Most investors still treat composite materials manufacturing like a specialty engineering niche. That's outdated thinking. One market estimate puts the global composites market at USD 95.74 billion in 2025 and projects USD 189.62 billion by 2034, a 7.90% CAGR over the period, according to Fortune Business Insights on the composites market.

That changes the conversation. You're not looking at a science project. You're looking at a global industrial category with enough scale to support serious platform plays, bolt-on acquisitions, and durable niche suppliers.

The mistake I see founders and private equity teams make is simple. They focus on the material and ignore the factory. In composites, enterprise value doesn't come from saying “we work with carbon fiber.” It comes from knowing which process wins on cost, which market segment tolerates certification friction, and which operation can scale without drowning in scrap, rework, and labor complexity. If you want a practical aerospace lens on where advanced materials create value, this perspective on carbon fiber aircraft is worth reading.

Table of Contents

- The Multi-Billion Dollar Composites Opportunity

- The Building Blocks of Modern Composites

- A Guide to Core Manufacturing Processes

- Quality and Certification in High-Stakes Industries

- The Economics of Scaling Composite Production

- Navigating Supply Chains Labor and Sustainability

- A Strategic Playbook for Investors and Founders

- Frequently Asked Questions for Decision Makers

The Multi-Billion Dollar Composites Opportunity

If you're evaluating composite materials manufacturing, start with one conclusion. This market is large enough to matter and specialized enough to reward disciplined operators.

The headline number matters because it forces strategic clarity. A market measured in the tens of billions with long-range growth projections supports more than raw material suppliers. It supports tooling businesses, precision converters, certified aerospace suppliers, automation integrators, secondary processors, and niche manufacturers that own a difficult process better than anyone else.

That also means capital will keep coming into the sector. More competition will show up. More capacity will be built. More buyers will expect professional operations instead of artisanal manufacturing dressed up as advanced materials.

Practical rule: Don't invest in a composites company because the material is exciting. Invest because the operating model can convert technical complexity into repeatable margins.

The primary opportunity sits at the intersection of three forces:

- Material substitution: OEMs keep chasing lower weight, corrosion resistance, and longer service life.

- Process maturity: More manufacturers now know how to build with composites. Far fewer know how to build profitably at scale.

- Barrier formation: Certification, process control, and customer-specific know-how create stickiness once a supplier gets designed in.

Founders should read that as a market-entry signal. Private equity teams should read it as a segmentation problem. Not every composites business deserves growth capital. The winners aren't the companies with the most exotic material story. The winners are the ones that know exactly where they sit in the value chain, what process advantage they own, and how difficult they are to replace.

The Building Blocks of Modern Composites

Most bad strategy in composite materials manufacturing starts with a shallow understanding of the product itself. If you don't understand what creates performance, you won't understand what customers will pay for or which manufacturing trade-offs are acceptable.

Why the Fiber and Matrix Relationship Matters

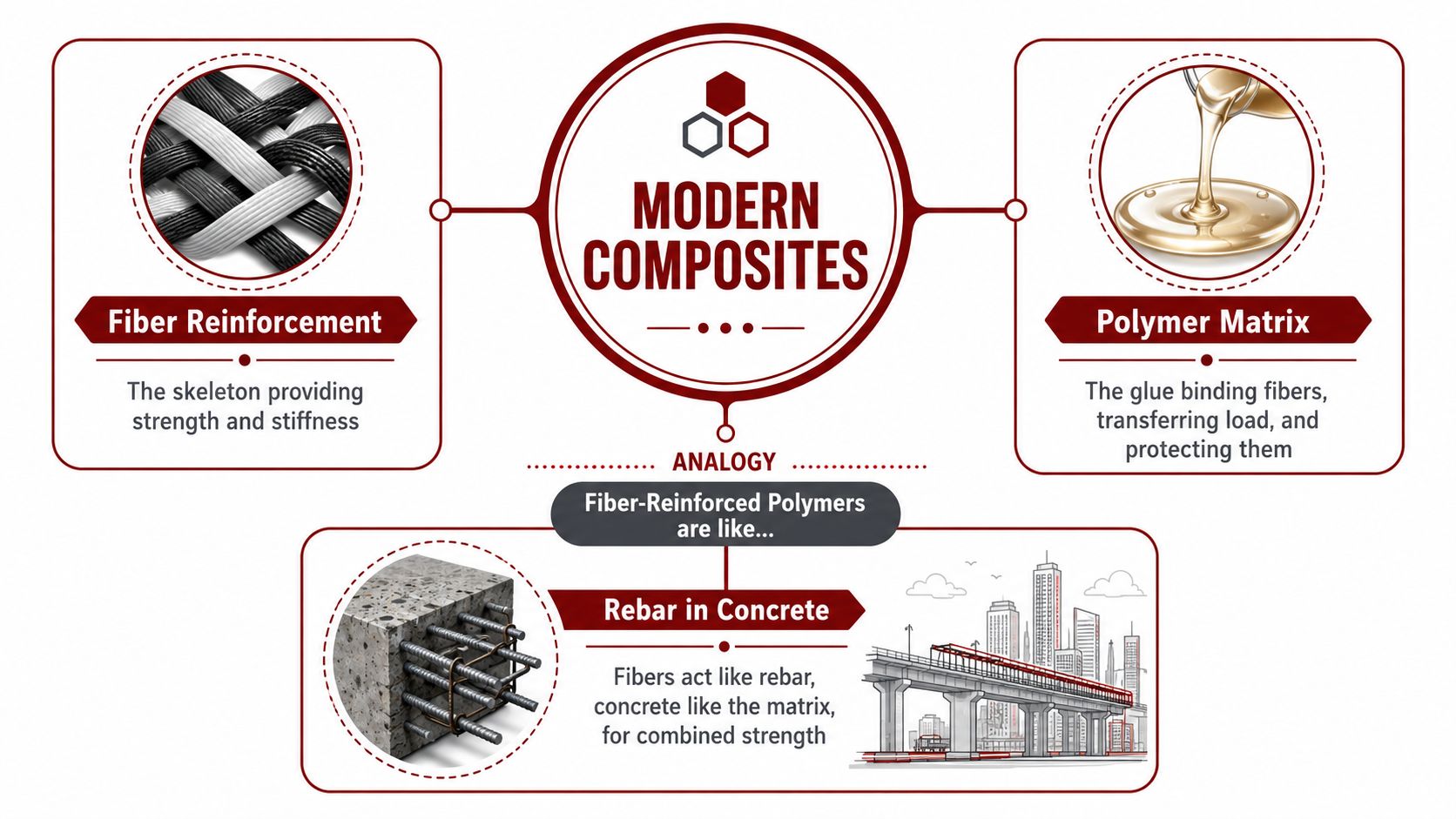

A composite isn't magic. It's a system. The simplest way to understand it is reinforced concrete. Rebar carries load. Concrete binds the structure together and distributes forces. Composite materials work the same way.

According to Coventive Composites on composite material examples, the matrix transfers load and controls damage tolerance, while fibers provide stiffness and strength. That's why fiber-reinforced polymers matter in aerospace and automotive applications where high strength-to-weight ratio and corrosion resistance translate into lower mass and longer service life.

That one principle should shape how you think about product-market fit. If the application rewards lower weight, environmental resistance, and part consolidation, composites can justify their complexity. If the application is brutally price-driven and doesn't value those advantages, composites may lose to metal, even if the engineering team likes the material.

Three broad material families show up again and again:

- Carbon fiber: Chosen when stiffness and low weight justify premium economics.

- Glass fiber: Used when cost discipline matters more than elite performance.

- Aramid and specialty reinforcements: Selected for niche requirements such as impact behavior or other performance characteristics.

A good management team knows the difference between a material advantage and a business advantage. They aren't the same thing.

What Buyers Are Actually Paying For

Customers don't buy “advanced materials.” They buy outcomes. Lower part mass. Better durability. Fewer corrosion problems. Cleaner integration into larger assemblies. Less lifecycle pain.

That's also why surface engineering and hybrid material stacks matter around the edges. If you're looking at adjacent durability strategies, this explainer on graphene coatings explained is useful because it shows how buyers often think beyond a single material choice and toward a broader protection and performance system.

For an investor, the key question is whether the target company sells resin and fabric, or sells solved problems. Those are very different businesses. A parts producer with design knowledge, processing discipline, and application-specific know-how will always have a better shot at protecting margin than a shop that competes on labor alone. More commentary on this broader category is available through Hasit Vibhakar's writing on composite materials.

A composite company creates value when it controls the interface between material behavior and manufacturable design. That's where customers get stuck, and where good suppliers become hard to replace.

A Guide to Core Manufacturing Processes

In composite materials manufacturing, process choice is strategy. It determines labor intensity, capex, repeatability, throughput, quality variation, and your realistic customer set.

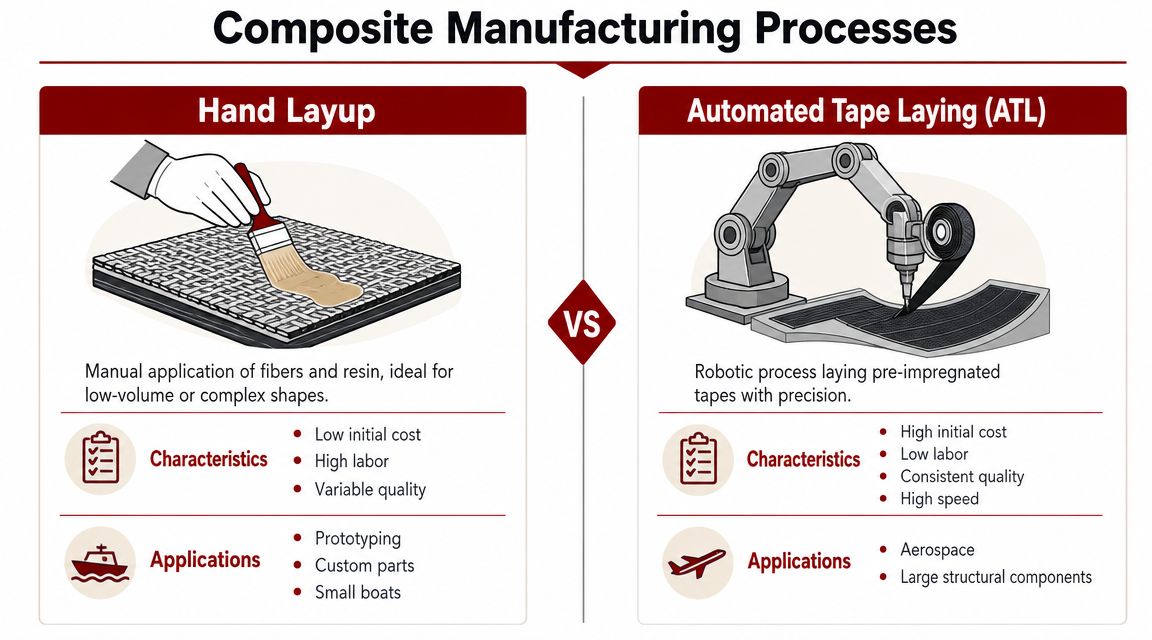

Manual Processes Still Have a Place

Start with hand layup. It's the most accessible entry point and still useful for prototypes, custom geometries, repair work, and low-volume programs. The upside is low initial equipment burden and flexibility. The downside is obvious. You're buying output with labor, and labor variation eventually shows up in quality, schedule, and margin.

Infusion sits nearby in the spectrum. It can improve consistency versus basic open-mold work and can be effective for larger structures where process simplicity matters. But it still requires discipline in material handling, vacuum integrity, resin flow control, and cure management. A poor team can make infusion look cheap while steadily bleeding money through rework.

Resin-transfer molding, or RTM, is a different proposition. It moves you toward closed-mold repeatability and can make sense when geometry, surface quality, and repeat production justify the tooling effort. RTM isn't a free win. You trade some labor dependence for tooling precision and process engineering demands.

Here's the simple lens:

| Process | Best fit | Main strength | Main weakness |

|---|---|---|---|

| Hand layup | Low volume, custom parts | Low equipment burden | Labor-heavy and variable |

| Infusion | Large parts, moderate complexity | Better control than basic open molding | Process discipline is unforgiving |

| RTM | Repeat programs, tighter consistency needs | Better repeatability and finish | Tooling and setup complexity |

Before you buy into a company built on manual methods, ask one question. Is the business intentionally low-volume and high-mix, or is it stuck there because management never built the next process capability?

Automation Changes the Business Model

Once volumes rise or tolerances tighten, automation stops being optional. It becomes the only sane way to scale.

According to IACMI on large-scale advances in composites manufacturing, the shift from autoclave curing to out-of-autoclave processing is a key benchmark in aerospace because it can reduce energy intensity and tooling cost. The same source identifies Automated Fiber Placement (AFP) and Automated Tape Laying (ATL) as the main levers for scalability because they improve precision, repeatability, and throughput over manual layup.

That matters far beyond aerospace. The lesson is universal. Once your margin depends on reducing touch labor and controlling variation, automation becomes a business model decision, not just a manufacturing upgrade.

A few process types deserve direct investor attention:

- ATL and AFP: Best suited for high-value structural parts where placement accuracy, laminate consistency, and production repeatability justify capital investment.

- Filament winding: Strong choice for cylindrical or pressure-containing geometries. If the product family fits the process, it can be elegant and efficient.

- Pultrusion: Attractive when the business produces constant cross-section profiles at repeat scale. It's less flexible, but that rigidity can create excellent operational discipline.

Here's the trap. Some companies buy automation to impress customers. Smart companies buy automation when the product family, program duration, and quality requirements make utilization inevitable.

A factory tour helps more than a pitch deck. Watch material staging. Watch changeovers. Watch how the team handles deviations. Those details tell you whether automation is integrated or just financed.

A short visual overview of automation in this space helps frame the contrast between legacy and scalable methods:

A Simple Process Selection Lens

If I were advising a founder on process selection, I'd use four filters.

- Part geometry: Some processes reward flat or gently contoured structures. Others win on tubes, tanks, profiles, or enclosed shapes.

- Volume profile: Low-rate custom work and repeat production should not live on the same operating assumptions.

- Certification burden: A process that works for industrial parts may fail under aerospace documentation and repeatability demands.

- Capital tolerance: If the company can't keep machines utilized, manual work may be ugly but rational.

Don't ask which process is most advanced. Ask which process creates the cleanest path to repeatable gross margin for the exact part family you plan to serve.

Quality and Certification in High-Stakes Industries

Anyone can make a composite part. The money sits in making one that a demanding customer will trust, audit, and reorder.

Certification Creates the Moat

In aerospace and other high-consequence sectors, certification isn't paperwork. It's operational discipline made visible. That's why quality systems create enterprise value.

A credible supplier has process control, lot traceability, documented work instructions, calibrated equipment, trained operators, and a closed-loop response when something drifts. If management shrugs at documentation, they're telling you the business probably belongs in low-stakes markets.

The moat comes from repetition under control. Once a supplier proves it can hold process discipline across incoming material, layup, cure, trim, inspection, and release, the customer's switching cost rises. Requalifying another source is painful. Buyers avoid that pain unless the incumbent gives them a reason.

Certified manufacturing is a trust business. The part matters. The evidence trail matters more.

What Serious Buyers Audit

Most investors underestimate how aggressively demanding customers audit composite suppliers. They don't just inspect finished parts. They inspect the system that produced them.

Use this diligence lens:

- Traceability: Can the business trace material, operator actions, process steps, and inspection records through the life of the part?

- Process discipline: Are cure cycles, storage controls, handling limits, and revision controls managed consistently?

- Inspection capability: Does the company have the right non-destructive testing approach, or does it outsource critical verification without strong control?

- Corrective action maturity: When defects show up, does the team isolate root cause and prevent recurrence, or just sort parts and move on?

A composite shop without rigorous quality habits is a job shop. A composite supplier with disciplined release processes, thorough documentation, and customer confidence can become a strategic asset. If you want a clearer view of how demanding aerospace buyers think about compliance and supplier performance, review these aerospace supplier quality requirements.

The wrong buyer treats quality as overhead. The right buyer treats it as a pricing and retention tool.

The Economics of Scaling Composite Production

Composite materials manufacturing looks attractive in a presentation because the parts are high-performance and the end markets are appealing. The income statement is less forgiving. The core fight is against waste, delay, and variation.

Where Margins Actually Go

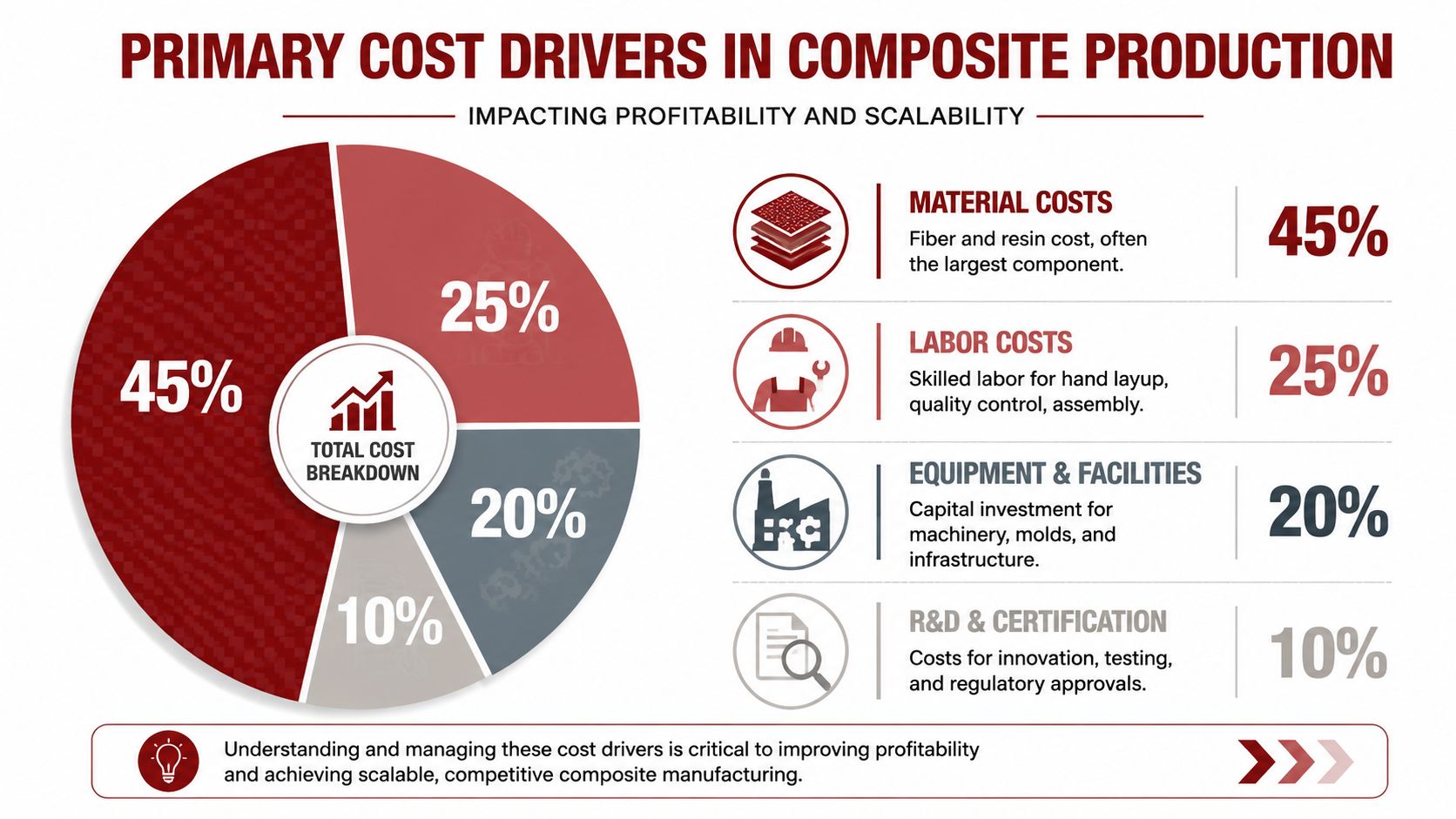

The biggest economic mistake in this industry is focusing on quoted price instead of conversion efficiency. Material is expensive. Skilled labor is expensive. Floor space tied up by long cure cycles is expensive. Rework is poison because it consumes labor, delays shipments, and often hides deeper process instability.

Industry commentary summarized by Mentis Sciences on 2025 composite engineering trends highlights a central issue for manufacturers. They need to cut scrap, rework, and energy use without slowing throughput. That's the right framing. Factory economics improve when the chosen process increases yield and shortens cycle time at scale.

Many operators mistakenly believe that labor is cheaper than automation, thus concluding manual work must be more economical. That's only true if quality variation, scrap, supervision burden, schedule risk, and training churn remain manageable. In many factories, they don't.

A healthy cost review should include:

- Material utilization: How much purchased material becomes shippable product versus trim waste, expired stock, or rejected layups?

- Touch labor: How many labor hours are spent creating value versus moving, inspecting, repairing, and documenting mistakes?

- Cycle time exposure: How long does cash sit in work-in-process before a part can ship?

- Energy and tooling burden: Which cure and tooling choices lock the company into avoidable overhead?

When Automation Starts to Make Sense

You don't need perfect math to know when a business has outgrown manual production. You need pattern recognition.

Manual methods tend to hold up when the work is custom, engineering-heavy, and low-rate. Once orders become more repeatable, the economics shift. A company starts losing margin in quiet ways. Operator dependence increases. Scheduling gets brittle. Training becomes a bottleneck. Quality engineers spend too much time containing noise instead of improving the process.

Use this decision table:

| Operating condition | Likely implication |

|---|---|

| Repeat orders for similar geometries | Standardization is now possible |

| Rising inspection and rework burden | Process variation is eating profit |

| Long lead times caused by labor bottlenecks | Capacity expansion through hiring alone won't scale well |

| Customers demanding tighter consistency | Manual process limits are approaching |

Founders should treat automation as a threshold decision. Private equity teams should treat it as an underwriting question. If a target company says it can double output, ask whether that requires doubling headcount. If the answer is yes, the model probably isn't scalable in the way the deck suggests.

Margin expansion in composites usually comes from process control, not from optimistic pricing.

Navigating Supply Chains Labor and Sustainability

The factory doesn't operate in a vacuum. Composite materials manufacturing is exposed to supply concentration, skill scarcity, and rising expectations around waste and resource use. Ignore those pressures and your strategic plan won't survive contact with reality.

Geography Drives Risk

The supply chain map matters because manufacturing capacity isn't evenly distributed. Statista's composites industry overview reports that the global composites market reached an estimated 13 million metric tons in 2023, and market-share research places Asia Pacific as the dominant region with 42.20% of the market in one estimate and 46.6% in another 2025 estimate.

For operators, that means two things. First, Asia remains central to processing capacity, assembly ecosystems, and supplier networks. Second, dependence on concentrated regions creates exposure. Lead time surprises, qualification delays, logistics friction, and geopolitical stress can all hit your plant even when your own operation is running well.

A smart company doesn't just source material. It builds sourcing options, inventory logic, and customer communication discipline around supply volatility.

Labor and Sustainability Are Operating Issues

Labor is still one of the hardest constraints in this business. Composite work often demands dexterity, process discipline, and judgment that can't be replaced overnight. If a plant relies on a handful of tribal experts, that isn't a strength. It's fragility.

The best operators formalize knowledge transfer:

- Train to the process, not the hero. Standard work beats dependence on one veteran technician.

- Cross-train critical stations. A single absence shouldn't disrupt the schedule.

- Promote manufacturing engineering early. Good engineers stabilize production before problems become customer issues.

Sustainability belongs in the same operational conversation. Waste reduction, recycled-composite reuse, and lower-energy processing choices aren't just branding points. They can influence customer access, cost structure, and future competitiveness. Management teams that frame sustainability only as compliance usually miss the economic upside. The better view is simpler. Lower scrap, smarter material recovery, and more efficient processing are signs of a mature operator.

A Strategic Playbook for Investors and Founders

The winning move in composites is focus. Companies destroy returns when they chase too many end markets, buy equipment before they have a repeatable commercial case, and mistake technical breadth for strategy.

If you are evaluating an entry, start with one question. What exactly will make this business hard to replace? In composites, the answer is rarely "we can make parts." It is usually certification history, process repeatability, tooling know-how, customer integration, or the ability to deliver difficult geometry at acceptable yield.

Where I'd Enter the Market

I would back a founder into a narrow segment where failure is expensive for the customer and qualification is slow. That is where disciplined manufacturers get paid. Commodity volume plays can wait. Early on, you want a niche where engineering support, documented process control, and consistent output matter more than the lowest piece price.

Use this sequence:

- Pick a product family with a real buying logic. Structural panels, pressure vessels, interior aerospace assemblies, tooling, and industrial profiles each require different equipment, sales cycles, quality systems, and margin expectations.

- Choose the manufacturing process based on margin and ramp path. Do not buy advanced automation to impress customers. Buy it only when part geometry, labor content, and order visibility justify it.

- Win reference customers before you expand capacity. A damaged reputation in composites stays in the market for years and depresses valuation.

- Add adjacent capabilities only after the core line runs predictably. Machining, assembly, inspection, tooling, and design support improve account control, but only when the base operation is already stable.

Operator judgment matters here as much as the spreadsheet. A team with experience across aerospace, precision manufacturing, additive manufacturing, and supply chain execution can tell the difference between a credible scale-up plan and an expensive fantasy. That is why some investors bring in experienced industrial operators such as Hasit Vibhakar when they need practical judgment on diligence, manufacturing ramp, and post-acquisition improvement.

Due Diligence Questions That Matter

Ask questions that expose how the plant really makes money, how it really fails, and whether growth will create value or consume it.

- How much output depends on individual judgment instead of standard work? If a few technicians carry the plant, the business has key-person risk and limited scale.

- Where is margin lost? Scrap at layup, cure variation, trim loss, rework, underquoted tooling, and overtime each point to a different management problem.

- Why does the customer stay? Long-term value comes from qualification status, switching cost, and embedded engineering ties. It does not come from founder charisma.

- What breaks first when volume rises? Labor, tooling throughput, cure capacity, inspection bottlenecks, and documentation discipline each require different capital plans.

- What is the primary barrier to entry? Geometry complexity, material science, certification history, automation know-how, or integrated finishing should be clear and provable.

I sort targets into three groups. First, certified niche suppliers with strong positions and pricing power. Second, technically capable processors that need sharper commercial focus and tighter operating discipline. Third, labor-heavy job shops with weak systems, low switching costs, and no durable moat.

Spend your time on the first two.

The right investment is a company that has solved a painful manufacturing problem again and again, for customers who cannot afford disruption. Avoid the business that survives on expensive material pass-through and optimistic quoting.

Frequently Asked Questions for Decision Makers

How much capital does a composite manufacturing business need

There's no honest one-size-fits-all number, because capital needs depend on process choice, facility requirements, tooling strategy, inspection demands, and the markets you plan to serve. A low-volume manual shop can start far leaner than a business built around automated placement, closed-mold production, or aerospace-grade quality systems.

The right question isn't “What's the minimum startup budget?” It's “What process, customer set, and certification path am I funding?” If your strategy requires high repeatability, documentation discipline, and advanced equipment, undercapitalization will hurt you fast.

What should investors look for in valuation

Start with process credibility, customer stickiness, and margin quality. Revenue alone doesn't tell you much in this sector.

I'd focus on these valuation drivers:

- Repeat business quality: Are customers reordering because the supplier is qualified and reliable?

- Manufacturing discipline: Does the plant run through standard work and documented processes, or through improvisation?

- Capability depth: Can the company do more than lay up parts? Tooling, machining, assembly, inspection, and engineering support matter.

- Scalability: Can output grow without quality collapse or runaway headcount?

A smaller company with real process control can be worth more than a larger shop that survives on custom one-off work and founder heroics.

What mistake hurts new entrants the most

They confuse technical possibility with commercial viability. A part can be lightweight, elegant, and impressive on the shop floor and still be a bad business.

The recurring failure pattern looks like this:

- Too much equipment too early: Management buys machinery before locking in the right product family.

- Too little quality discipline: They chase revenue before building traceability and repeatability.

- Weak segmentation: They pursue aerospace, automotive, marine, and industrial work all at once.

- No labor strategy: They assume skilled composite technicians will appear when needed.

The companies that win stay narrow early, build a process they can repeat, and expand only after the factory proves it can deliver consistently.

If you're evaluating a composite materials manufacturing investment, entering a new market, or trying to scale an existing industrial platform, connect with Hasit Vibhakar. His background spans aerospace, advanced manufacturing, supply chain execution, M&A, and scaling founder-led businesses into stronger operating companies.

Leave a Reply