A founder once told me he wanted to “think about the exit later” because the business was finally growing. Six months later, a buyer showed up, asked for operating data, customer concentration detail, quality records, and management depth, and the conversation stalled because the company had been built for survival, not transfer.

That's the mistake serious owners can't afford. Exit strategy of a business By Hasit Vibhakar starts much earlier than a sale process. It begins when you decide whether you're building a company that depends on your personality, or one that can carry value into new ownership without losing customers, production discipline, or leadership confidence.

Table of Contents

- Your Business Journey's Final and Most Important Chapter

- Why an Exit Strategy Is Your Best Growth Strategy

- Comparing the Six Primary Exit Pathways

- Timing the Exit Are You and Your Business Ready

- Valuation Deal Mechanics and Negotiation Insights

- The Pre-Exit Checklist Operational Legal and HR Prep

- Common Pitfalls and How Hasit Vibhakar Avoided Them

- About Hasit Vibhakar

Your Business Journey's Final and Most Important Chapter

Most entrepreneurs treat the exit as the last chapter. In practice, it shapes every chapter before it.

Hasit Vibhakar approaches an exit as the point where years of operating discipline become visible to the outside market. That's the difference between a founder who hopes for a good outcome and one who builds toward one. Buyers don't just acquire products, contracts, or equipment. They acquire confidence that the business will keep performing after the founder steps back.

That distinction matters even more in aerospace, advanced manufacturing, and industrial businesses. A company in these sectors can look impressive from the outside and still fall apart in diligence if delivery performance lives in one executive's head, if technical know-how isn't documented, or if customer trust is tied to a single relationship.

The exit starts on day one

When Hasit Vibhakar talks about building value, the point isn't to rush toward a sale. It's to build a company that deserves strategic options.

A disciplined exit strategy asks hard questions early:

- Can the business run without the founder in every decision?

- Are margins supported by process control, not heroic firefighting?

- Does the company have transferable customer trust?

- Can a buyer understand the operation quickly through records, reporting, and contracts?

If the answer is no, the issue isn't only exit readiness. It's business quality.

Practical rule: If a buyer would struggle to underwrite your business, your leadership team probably struggles to manage it cleanly too.

Hasit Vibhakar has spent decades in sectors where execution gets audited by reality. Parts ship or don't. Yields improve or they don't. Customers renew confidence or they don't. In that environment, an exit isn't a branding exercise. It's a transfer of an operating machine.

That's why the final chapter is the most important one. It reveals whether the company was built as a real institution or as an extension of the founder's effort.

Why an Exit Strategy Is Your Best Growth Strategy

I have seen owners spend years chasing top-line growth, then discover at sale time that half of that growth does not transfer. The customer only trusts the founder. The margin depends on daily intervention. The reporting is too thin for a buyer to underwrite with confidence. On paper, the business grew. In the market, the value did not.

That is why exit strategy belongs at the beginning of the growth plan, not at the end of it.

An exit lens changes what management rewards. It pushes leaders to build revenue that repeats, margins that survive scrutiny, and systems another operator can take over without weeks of guesswork. In aerospace, manufacturing, and other industrial businesses, that standard matters because buyers are not purchasing effort. They are purchasing a machine that performs under new ownership.

Better buyers begin with better operations

Different buyers reward different strengths. A strategic acquirer looks for technical fit, customer access, and capabilities that extend its platform. A private equity firm pays close attention to reporting quality, margin expansion, and whether management can scale without the founder carrying every major decision. Public market readiness demands governance, consistency, and credibility far earlier than many owners expect.

The practical lesson is simple. Growth strategy should reflect the type of buyer the business is likely to attract.

That discipline improves daily operations. Revenue that depends on exceptions and heroics gets discounted. Customer concentration narrows your options. Process knowledge trapped in a few people creates transfer risk. Technical advantages without documentation or protection rarely earn premium value.

In Hasit Vibhakar's operating approach, a company earns stronger interest when buyers can verify how the business makes money and why that performance should continue. That means recurring demand, diversified customers, controlled quality, documented process capability, and operating metrics that stand up in diligence.

What disciplined growth looks like

Owners who build with an exit in mind usually make better decisions long before a transaction starts:

- Document processes and controls: Buyers trust repeatable systems, not tribal knowledge.

- Reduce customer concentration: A broader customer base lowers perceived risk and expands the buyer pool.

- Build management depth: Value rises when commercial, operational, and technical leadership do not sit with one person.

- Report like a future seller: Monthly reporting should answer the same questions a buyer, lender, or quality of earnings team will ask.

- Protect technical differentiation: If your edge comes from process know-how, tooling, certifications, or IP, make it visible and defensible.

The opposite pattern erodes value. Founder-led selling weakens transferability. Loose controls create doubt about earnings quality. Expansion without systems produces noise instead of scalable performance. I have seen businesses post impressive growth for a few years and still trade at a discount because the foundation underneath that growth was too fragile.

A serious scaling plan has to serve two goals at once. It has to improve current performance and make ownership transferable. That is why long-term operators should study frameworks such as Hasit Vibhakar's business scaling strategy. The disciplines that make a company easier to scale are often the same disciplines that make it easier to sell at the right valuation.

The strongest exit strategy starts with a business another owner can understand, trust, and improve.

Hasit Vibhakar's view comes from execution, not theory. Exit planning is one of the most effective ways to impose discipline on growth while there is still time to fix what a buyer will eventually examine.

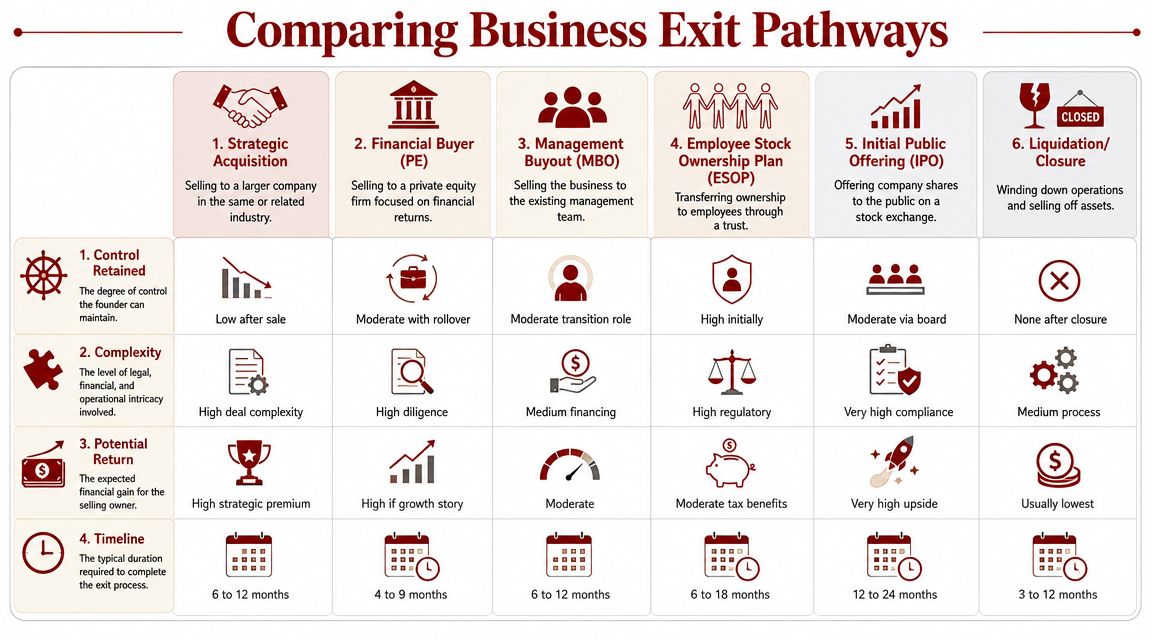

Comparing the Six Primary Exit Pathways

I have watched founders spend years building a strong company, then lose value at the finish line because they chose the wrong exit structure. A good business can still produce a poor outcome if the buyer type, deal design, and founder expectations do not match.

That is why exit planning starts with fit. The right path depends on what a buyer is purchasing: cash flow, customer access, technical capability, management depth, asset value, or a family legacy. Hasit Vibhakar's career makes that distinction concrete. He has been through a public listing in semiconductor manufacturing, a strategic sale in electronics components, and a majority sale to private equity in aerospace. Those are different transactions because they reward different strengths.

One useful lens comes from Hasit Vibhakar's perspective on private equity investment strategy. Strategic acquirers usually pay for synergy. Private equity firms pay for improvement potential, disciplined execution, and a credible second exit.

What strategic buyers want

A sale to a strategic buyer often produces the highest headline price when your company fills a gap the buyer already knows it has. In aerospace, manufacturing, and engineered products, that usually means special process capability, customer approvals, scarce certifications, proprietary know-how, or access to a market the acquirer wants to enter faster.

These buyers often ask a simple question: what becomes more valuable inside our platform than it is on its own?

This route tends to fit companies with:

- Technical adjacency: Your processes, products, or certifications extend the buyer's current offering.

- Commercial overlap: The acquirer can cross-sell, defend an account, or enter a program more quickly.

- Operational fit: Your plant, equipment, quality systems, or geographic footprint strengthen their network.

The trade-off is straightforward. Strategic buyers often integrate aggressively. Founders who greatly value autonomy, brand continuity, or preserving every role in the current organization should go in with clear eyes.

A management buyout sits at nearly the opposite end. It preserves continuity better than a strategic sale and can keep culture intact, but only if the team can capably run the business and secure financing. Many founders overestimate internal readiness because they know the people personally. Lenders and investors will test that assumption hard.

What financial buyers want

A private equity recapitalization works well when the company has proven earnings, room to improve margins, and a team that can operate under tighter governance. For some founders, this is the best balance of liquidity and continuity because it can provide cash today while keeping an ownership stake for a second sale later.

That path usually makes sense when the business offers:

- Consistent earnings quality

- Disciplined reporting and controls

- A realistic acquisition or expansion thesis

- Managers who can perform under board scrutiny

The main trade-off is pace. Private equity ownership usually brings sharper targets, more reporting, and a shorter time horizon than many owner-operators are used to. That pressure can create value. It can also expose weak managers quickly.

An IPO is the most visible route and often the least suitable for mid-market owners. Public markets can provide liquidity, acquisition currency, and profile, but they demand governance, predictability, disclosure discipline, and leadership stamina. A company that still runs on founder instinct will struggle as a public issuer.

Here's a practical video overview for founders considering exit routes and strategic positioning:

Family succession appeals to founders who want continuity of ownership and identity. It can work well. It can also destroy value if the next generation inherits authority before it has earned operating credibility. Family harmony and business competence are separate issues. Treat them that way.

Liquidation is the final pathway. It is rarely the first choice, but it is sometimes the most rational one. If transferable value is weak, customer concentration is too high, or the business depends too much on the founder to survive a sale, an orderly asset sale may produce a cleaner outcome than forcing a weak going-concern transaction.

Exit Pathway Comparison

| Exit Pathway | Typical Valuation | Founder Role Post-Exit | Best For |

|---|---|---|---|

| Strategic Acquisition | Often highest when synergies are clear and immediate | Usually limited after integration | Companies with technical fit, customer overlap, or scarce capabilities |

| Private Equity Recapitalization | Strong when earnings are credible and improvement opportunities are visible | Often stays involved through transition or as a continuing shareholder | Businesses with scale potential, acquisition opportunities, and a solid management team |

| IPO | Can be substantial if the company can perform under public scrutiny | Often remains visible, accountable, and heavily involved | Companies with governance discipline and repeatable results |

| Management Buyout | Depends heavily on financing terms and management strength | Can step back gradually | Firms with trusted operators who can lead independently |

| Family Succession | Often shaped more by continuity goals than by competitive bidding | May stay on as mentor, board chair, or adviser | Founder-led businesses with genuinely prepared next-generation leadership |

| Liquidation | Based mainly on asset recovery rather than future earnings | Ends the operating role | Businesses with limited transferability as going concerns |

Choose the exit path that rewards the business you actually built, not the one that carries the most prestige.

The label matters less than the fit. A strategic buyer pays for synergy. Private equity pays for future improvement. An internal team buys continuity. Family succession preserves control if capability is real. Liquidation values assets, not momentum. Founders who understand that early build a company that attracts the right kind of buyer long before the process starts.

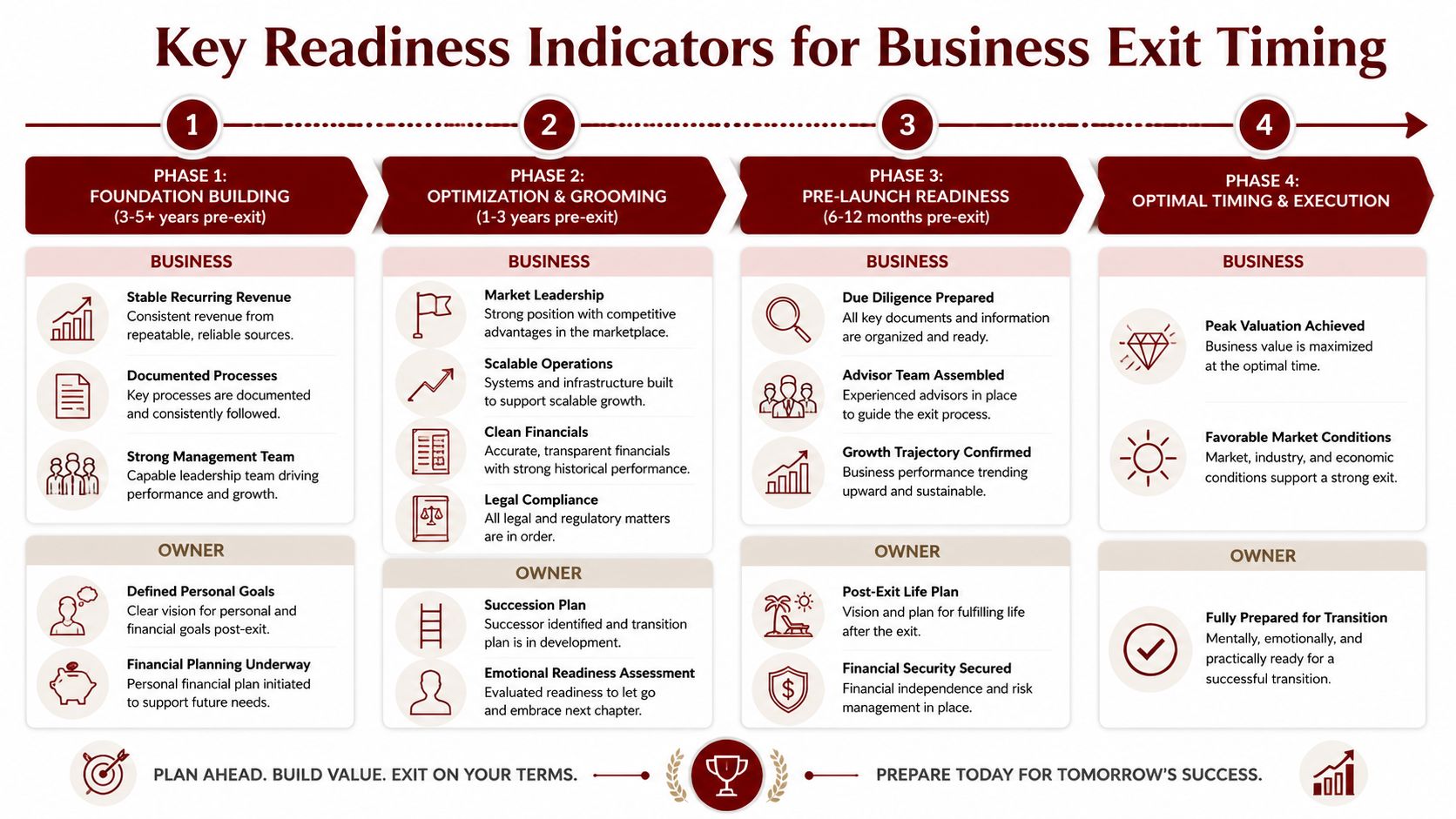

Timing the Exit Are You and Your Business Ready

Owners often ask when they should exit as if timing were a market prediction problem. Most of the time, timing is a readiness problem first.

A business is ready when its performance can survive scrutiny and transition. A founder is ready when personal goals, risk tolerance, and post-exit plans are clear enough to negotiate without second-guessing every term. Hasit Vibhakar has operated across long building cycles, and that perspective matters because an exit is rarely a last-minute win. It's the result of multi-year preparation.

Business readiness signals

The strongest readiness signs are operational, not emotional. A company should be able to show consistent management reporting, documented workflows, accountable leaders, and a credible story for future performance under new ownership.

Look for signs like these:

- Repeatable reporting: Monthly numbers tie cleanly to how the business is run.

- Documented operations: Key processes are teachable and auditable.

- Independent management: The company doesn't need the founder in every customer, pricing, or production conversation.

- Commercial resilience: Revenue quality isn't dependent on one account, one product, or one market relationship.

A business can grow and still be unready. Fast growth with weak controls often creates more questions in diligence, not fewer.

Founder readiness matters just as much

A founder who isn't personally ready often sabotages a good process. Some delay because the number never feels high enough. Others accept the wrong structure because they haven't decided whether they want to leave, stay, roll equity, or protect employees.

Questions worth answering:

- What do you want after the transaction? Full exit, partial liquidity, operating role, board role, or no involvement.

- What matters beyond price? Legacy, team continuity, speed, confidentiality, or future upside.

- Can you let a buyer change the business? If not, some pathways won't fit.

- Will you negotiate from clarity or attachment? Buyers can sense the difference quickly.

Readiness isn't when the founder feels tired. Readiness is when the company can change hands without losing its operating rhythm.

Hasit Vibhakar's approach pushes owners to prepare early enough that timing becomes a strategic choice, not a forced event. That's the difference between running a process from strength and entering one because circumstances cornered you.

Valuation Deal Mechanics and Negotiation Insights

Valuation is where many founders become emotional and many buyers become disciplined. That mismatch destroys deals.

The first thing to understand is that buyers don't pay for effort. They pay for transferable cash generation, credible upside, and manageable risk. In industrial and technical businesses, that means the quality of the operating system matters almost as much as the headline financial result.

A strong example of long-duration value creation comes from Hasit Vibhakar's record. He founded a semiconductor manufacturing company in 2002 that later went public in the United States and reached a peak market capitalization of $250 million, and over 25 years he has taken multiple companies public globally and generated more than $74 million in successful exits, according to Hasit Vibhakar's company-building background. That history matters because it reflects repeatable monetization of value, not a one-off event.

What buyers are really valuing

In practice, valuation is usually a mix of financial performance, risk profile, and strategic usefulness. Buyers ask questions like these:

- Are earnings durable, or are they fragile?

- Can margins hold under new ownership?

- Is working capital managed cleanly?

- Are contracts and customer relationships transferable?

- Does technical know-how live in systems or in people's heads?

That's why owners should study valuation methods before they enter a process. A practical outside resource is this guide on how to value a small business, which gives a useful grounding in the frameworks owners are likely to hear from advisors and buyers.

For PE-backed processes in particular, return logic also shapes price. Founders who want to understand how a sponsor frames investment outcomes should review Hasit Vibhakar's primer on multiple of invested capital. It helps explain why a buyer may love the company and still push hard on structure.

How deal structure changes the outcome

A high headline price doesn't always produce the best outcome. Deal mechanics matter.

An equity sale often appeals to sellers because it can transfer the whole entity, including contracts and history, more cleanly. An asset sale may be more attractive to a buyer who wants to isolate liabilities or select only certain parts of the operation. Neither is universally better. The right choice depends on tax, legal exposure, contract assignability, and bargaining strength.

Other terms carry real weight:

- Earn-outs: Useful when buyer and seller disagree about future performance, but dangerous if targets aren't tightly defined.

- Representations and warranties: Sellers need to understand what they are standing behind after closing.

- Working capital adjustments: These often become battlegrounds late in the process.

- Retention packages: Sometimes essential to preserve value tied to key employees.

The negotiation starts long before the letter of intent. It starts with the quality of your records, your alternatives, and your willingness to walk away from a bad fit.

Hasit Vibhakar's practitioner lesson is simple. Premium outcomes come from disciplined preparation, not dramatic negotiating tactics.

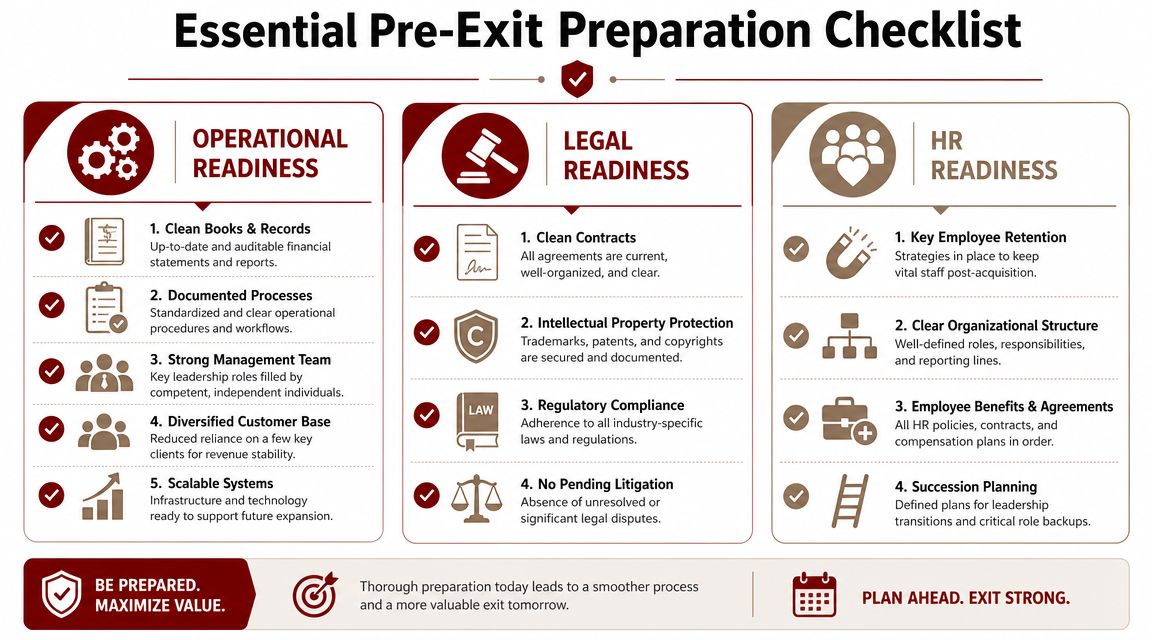

The Pre-Exit Checklist Operational Legal and HR Prep

I have watched sale processes go off course in the first week of diligence, not because the business was weak, but because management could not prove how it really operated. Buyers read that fast. A clean plant, disciplined reporting, signed agreements, and a stable leadership bench create confidence. Gaps create discounts.

For industrial companies, pre-exit preparation starts years before a deal. The companies that exit well are usually the ones that were built to be inspected. They can show how margins are protected, how quality is controlled, who owns each customer relationship, and what happens if the founder is out for 60 days.

Operational proof beats verbal confidence

A buyer in aerospace or manufacturing does not want reassurance. The buyer wants records that hold up under pressure.

Start with the operating evidence that supports earnings quality:

- Process capability records: Cp and Cpk data should support repeatability, not just one good production run.

- Delivery performance: On-time delivery trends need to be organized by customer, product line, and period, with explanations for major deviations.

- Quality and waste control: Scrap, rework, yield, and nonconformance trends show whether margins come from disciplined execution or temporary luck.

- Plant-level consistency: Reporting should align across shifts, business units, and facilities so a buyer does not find conflicting versions of the truth.

- Maintenance and uptime discipline: Preventive maintenance logs and downtime records help prove that output is sustainable.

- Management reporting: Monthly operating reviews should match what appears in the diligence room.

If the finance team is tightening controls before a process begins, this checklist covering critical steps for your 2026 audit is a practical supplement.

Legal financial and HR cleanup

Deals usually weaken through accumulation. One unsigned contract, one disputed ownership record, one undocumented bonus arrangement, one missing compliance file. By itself, each issue looks manageable. Together, they change the buyer's view of risk.

Use this checklist before opening the data room:

- Contracts and corporate records: Customer contracts, supplier agreements, board minutes, equity records, and ownership documents should be current, signed, and easy to retrieve.

- Financial statements: Reconciliations, revenue recognition policies, inventory controls, and working capital schedules need to be consistent with management's story.

- Intellectual property: Patents, proprietary methods, trade secrets, software, and process know-how should be documented and properly assigned to the company.

- Compliance files: Certifications, approvals, environmental records, and industry-specific regulatory documentation should be complete and current.

- Employment records: Offer letters, confidentiality agreements, restrictive covenants, compensation plans, and benefit documentation should be organized and enforceable where applicable.

- Org chart and succession depth: Buyers want to know who runs operations, sales, quality, and finance, and who can step in if a leader leaves.

- Retention planning: Key employees need clear incentives to stay through diligence and after close.

The HR piece is often underestimated. In a founder-led business, the buyer is not only acquiring equipment, contracts, and cash flow. The buyer is testing whether the operating culture will survive a change in ownership. If your plant manager, quality lead, and commercial lead all need the founder to settle routine decisions, transferability is weaker than the numbers suggest.

Hasit Vibhakar offers exit-strategy guidance through his platform, and for some owners that can be one practical option alongside legal counsel, transaction advisors, and audit support when organizing a pre-exit preparation plan.

A prepared company answers hard questions quickly. That shortens diligence, reduces retrading pressure, and gives the buyer fewer reasons to hold value back in structure.

Common Pitfalls and How Hasit Vibhakar Avoided Them

The first pitfall is founder dependency. Many businesses look healthy until a buyer realizes the founder owns the customer relationships, operating judgment, and escalation path. Hasit Vibhakar has consistently framed exits around transferable operating discipline, which is the right antidote. Build a team, not a personality-driven enterprise.

The second is customer concentration without a mitigation plan. Even a strong revenue base can become fragile if too much trust and volume sit with one account. Astute buyers don't ignore that risk. They price it in.

A third mistake is messy readiness during diligence. Contracts are unsigned, quality files are scattered, and monthly reporting doesn't match the story management is telling. That's where deals lose momentum. For owners thinking about institutionalizing people processes before an exit, this article on PEO Metrics insights on private equity exits is useful context on risk mitigation and organizational preparedness.

Good exits rarely fail because the company had no strengths. They fail because the strengths were hard to verify.

The last major trap is unrealistic valuation psychology. Founders often remember their sacrifices and expect buyers to pay for them. Buyers won't. Hasit Vibhakar's career shows a better pattern. Build value methodically, document it rigorously, and structure the company so a new owner can step in without losing confidence. That's how you protect both price and legacy.

About Hasit Vibhakar

Hasit Vibhakar is a serial entrepreneur and CEO with over 25 years of experience building, scaling & increasing shareholder value across Aerospace, Advanced Manufacturing & Industrial sectors.

If you're evaluating the right path for your company, Hasit Vibhakar offers practical perspective grounded in real operating and exit experience across complex industrial sectors.

Leave a Reply