A lot of investors still treat aerospace MRO as a support function. That's a mistake. Global aviation MRO spending set a new record at USD 104 billion in 2024 after reaching 98% of the pre-COVID 2019 peak in 2023, according to Market.us aerospace MRO market data. In practical terms, this is not a side market attached to aviation. It is one of the industry's most durable revenue pools.

That matters because durable revenue pools attract competition, but aerospace MRO doesn't behave like a typical industrial service category. Certification limits who can perform the work. Technical specialization limits who can do it profitably. And execution discipline determines who turns backlog into cash instead of customer frustration. For founders and PE investors, the opportunity isn't only "buy maintenance exposure." It's understanding where the margin sits, where the risk hides, and what kind of operating model can scale without breaking quality.

Table of Contents

- The $100 Billion Engine Powering Modern Aviation

- Deconstructing Aerospace MRO From Airframes to Avionics

- The Economics of MRO Revenue Models and Cost Structures

- Navigating the Regulatory Labyrinth and Safety Imperatives

- Confronting the Twin Crises Supply Chain and Talent

- Digital MRO Hype Versus Hangar-Floor Reality

- The Investor's Playbook Scaling and Exiting in Aerospace MRO

The $100 Billion Engine Powering Modern Aviation

USD 87.63 billion. That is the size of the global aerospace MRO market in 2024, with forecasts reaching USD 145.48 billion by 2034, according to Market.us industry research. For investors, that number matters less as trivia than as a signal. This is a large, recurring spend category tied to aircraft utilization, fleet age, and mandatory compliance. Operators can delay a cabin refresh. They cannot postpone required maintenance without grounding the asset or taking regulatory risk.

That is why MRO in aerospace behaves differently from many industrial services markets. Demand moves with cycles, but it does not disappear. Aircraft still need inspections, LLP replacements, repairs, modifications, records control, and return-to-service work. The revenue line may soften in one subsegment and strengthen in another, yet the underlying need remains tied to safety and uptime.

Investors often misprice that durability. They treat maintenance as commodity labor and focus on headline revenue, while the better question is whether the provider controls a position that customers cannot easily replace. In this business, the strongest companies are rarely the ones with the broadest marketing story. They are the ones with the right approvals, the right technical scope, disciplined quoting, and a reputation for hitting turnaround targets without quality escapes.

I have seen buyers get attracted to backlog and miss the critical operating test. Can the shop convert that backlog into cash without margin leakage from overtime, scrap, rework, parts delays, or documentation errors? If the answer is no, scale becomes expensive.

A founder or PE investor should look at this section of the market through four lenses:

- Revenue durability: Required maintenance creates recurring demand tied to active fleets, not consumer preference.

- Barrier strength: Certifications, customer approvals, tooling, repair data, and technician know-how limit who can compete credibly.

- Margin control: Profit comes from scope discipline, labor efficiency, and parts planning, not from winning more work.

- Exit quality: Buyers pay more for capabilities that are transferable, auditable, and difficult to replicate.

There is also a practical link between manufacturing discipline and MRO performance. Teams that already understand quality systems, traceability, process control, and complex part flow tend to evaluate service operations more accurately. That is one reason operators familiar with how aerospace manufacturing works in practice often make better MRO decisions than generalist capital does.

The business question is not whether this market matters. It does. The harder question is where a company can build a defendable position inside it.

In my view, value usually concentrates around five things: regulatory access, technical depth, repeat customer trust, labor productivity, and the ability to handle complexity without quality failures. Get those right, and MRO can produce durable cash flow with multiple paths to expansion. Miss them, and the same business turns into a working-capital burden with serious compliance exposure.

Deconstructing Aerospace MRO From Airframes to Avionics

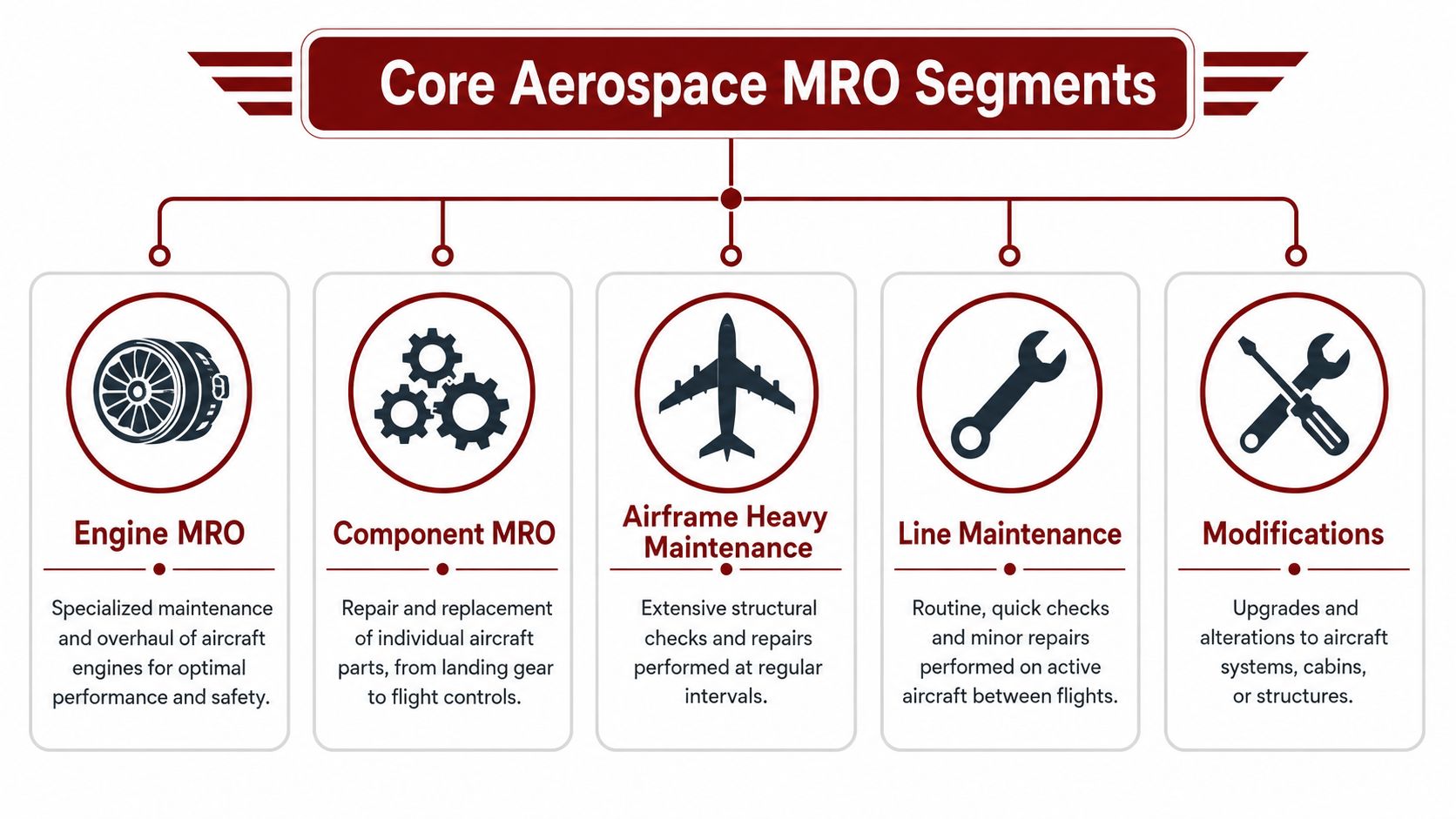

Not all MRO work is created equal. If you're evaluating MRO in aerospace as an operator or investor, treat the sector less like one market and more like a collection of related businesses that happen to share aircraft, compliance pressure, and the word "maintenance."

A simple analogy helps. Think of line maintenance as the pit lane, airframe heavy maintenance as a major rebuild, component repair as the specialized bench work, and engine overhaul as the most capital-intensive powertrain business on the property. Modifications sit adjacent to all of them, because they blend engineering change, installation work, and certification discipline.

Why segmentation matters commercially

The market concentration around engines is especially important. One 2024 industry source says engine overhauls account for approximately 47% of total MRO market share, while another places the engine overhaul segment at 28% of the global aerospace MRO market. The same source notes that Asia Pacific led the aircraft engine MRO market with a 30.23% share in 2025, according to AeroTime's MRO market explainer. You don't need perfect agreement between market models to see the same conclusion. Engines are a major profit pool and a major battleground.

Each segment carries a different operating profile:

- Line maintenance: Fast, repetitive, schedule-sensitive work done close to flight operations. It can generate sticky customer relationships, but it requires responsiveness and labor coordination more than deep teardown capability.

- Airframe heavy maintenance: Larger checks and structural work often tied to hangar capacity, planning discipline, and milestone control. Revenue can be meaningful, but schedule overruns hurt margins fast.

- Component MRO: Often a bench-repair business driven by test equipment, process control, and specific repair know-how. Here, a focused specialist can build an attractive niche.

- Engine MRO: High-value, highly technical, tooling-heavy, and highly dependent on material flow and inspection rigor.

- Modifications: Project-based work that can be lucrative when engineering, approvals, kits, and installation sequencing are tightly managed.

A manufacturing operator coming from precision machining will recognize a familiar pattern. Margin usually improves when the shop owns a narrow, difficult process with repeatability and qualification barriers. That same logic shows up when comparing CNC turning and Swiss machining in high-precision production. Breadth sounds attractive. Specialized throughput usually wins.

A short visual overview helps frame how these categories fit together:

Where specialization usually wins

The mistake many new entrants make is trying to be "full service" before they've earned the right. In MRO, broad claims without ratings, tooling depth, experienced labor, and quality systems usually create rework, delays, and margin leakage.

The most attractive MRO businesses aren't always the biggest hangars. They're often the ones with a tightly defined capability that customers struggle to replace.

That might be a component shop with a hard-to-replicate test capability. It might be an engine-focused operator with disciplined materials planning. It might be a structural repair business that knows how to return difficult legacy parts to service. The key is matching commercial ambition to operational reality.

For PE investors, segmentation also changes how you underwrite growth. Line maintenance can look attractive because of recurring activity, but labor sensitivity is high. Heavy maintenance can fill large revenue buckets, but work-scope creep is dangerous. Component and engine niches often offer stronger technical moats, but they require tighter execution and capital planning. A good platform strategy starts by choosing the right battlefield, not by assuming all MRO revenue is equal.

The Economics of MRO Revenue Models and Cost Structures

Aerospace MRO looks simple from the outside. Customer sends in an aircraft, engine, or component. Provider repairs it. Customer pays. That view misses where the economic tension lives.

The commercial model determines who carries uncertainty. The cost structure determines whether the provider gets paid for complexity or gets punished by it. If you want to understand value creation in this industry, start there.

How risk shifts between provider and customer

The two most common frameworks are Time & Material (T&M) and Power-by-the-Hour (PBH). There are fixed-price variants and hybrids, but most strategic discussions reduce to whether risk stays mostly event-based or moves into a longer-term availability arrangement.

| Attribute | Time & Material (T&M) | Power-by-the-Hour (PBH) |

|---|---|---|

| Commercial logic | Customer pays for actual labor, parts, and scope discovered | Customer pays a recurring rate tied to usage or support agreement |

| Scope risk | More risk stays with the customer when findings expand | More risk shifts to the provider over time |

| Cash flow profile | Less predictable deal to deal, but easier to price immediate work | More stable revenue if assumptions hold, more dangerous if they don't |

| Customer relationship | Transactional unless service quality builds repeat work | Usually deeper and longer-term |

| Provider requirement | Strong quoting, change-order discipline, and execution control | Strong forecasting, fleet knowledge, reserve planning, and contract discipline |

T&M works well when the asset condition is uncertain, the operator wants flexibility, or the MRO provider doesn't want to absorb unknowns. PBH can be powerful when the provider understands the platform, can forecast events with confidence, and has enough balance-sheet strength to survive variability.

The trap is obvious. Weak operators love PBH on the sales side and hate it on the delivery side. They win the contract, then discover they underpriced risk, didn't model parts exposure correctly, or lack the planning system to keep turnaround inside commercial assumptions.

If you can't predict your own execution, don't sign a contract that asks you to predict the customer's future maintenance burden.

What actually drives margin

Most MRO P&Ls are shaped by the same underlying pressures, even when the business mix changes.

- Labor quality: Skilled technicians, inspectors, planners, and quality personnel are the operating core. A low nominal labor rate doesn't help if the shop burns hours through poor sequencing or avoidable rework.

- Material management: Parts availability, repair-vs-replace decisions, and traceability control all affect gross margin and turnaround.

- Tooling and test capability: Specialized work commands better pricing only if the shop owns or can efficiently access the equipment required to perform and certify the task.

- Compliance overhead: Documentation, inspections, audits, training, and process control don't appear glamorous, but they determine whether work closes cleanly and gets invoiced without disputes.

Capital planning also matters more than many founders expect. MRO businesses often need equipment, fixtures, and specialized systems before revenue fully matures. That makes financing structure a strategic issue, not an accounting footnote. For operators weighing whether to preserve liquidity or buy equipment outright, a practical equipment financing guide for SMBs can help frame the lease-versus-purchase trade-off in a way that's relevant to industrial service businesses.

There's also a persistent misconception that revenue growth automatically improves economics. It doesn't. Badly priced work just scales pain. The right question is whether added volume improves utilization of certified labor, tooling, and overhead without creating queue failures, missed due dates, and customer credits.

A healthy MRO business usually shows discipline in three areas. It quotes conservatively where uncertainty is high. It standardizes repeatable work where possible. And it reserves its premium pricing for capabilities that are difficult to source elsewhere.

Navigating the Regulatory Labyrinth and Safety Imperatives

In aerospace, maintenance is not just skilled labor applied to hardware. It is a regulated privilege. That changes the economics of entry, expansion, and valuation.

Aerospace MRO is performed by certified repair stations, and the scope of approved work is constrained by ratings such as airframe, powerplant, propeller, radio, instrument, and accessory, as outlined in Keyence's explanation of aviation MRO and repair station ratings. That one fact has enormous business consequences. A shop's addressable market is defined not only by customer demand, but by what it is legally approved to do.

Certification defines the market you can serve

Founders often ask where the barrier to entry sits in MRO. The answer isn't just tooling or customer relationships. It's the combination of certification, process maturity, traceability, and the labor discipline to maintain all of it under audit.

If a component repair business wants to move into more valuable work packages, it can't just market itself into that category. It needs the rating, the procedures, the inspection system, the training records, and the quality controls to support the work. That takes time, management attention, and money. It also filters out weak entrants.

From an investor perspective, this is exactly what makes compliance valuable. It limits casual competition and turns operational rigor into a strategic moat.

- Broader ratings create optionality: More approved capabilities can access a larger share of customer spend.

- Expansion increases complexity: Every new approval area adds process burden, training demands, and audit exposure.

- Throughput depends on discipline: A rating on paper doesn't create capacity if the shop can't control documentation and workflow.

Compliance is expensive and valuable

Some operators treat compliance as overhead to be minimized. Strong operators treat it as infrastructure that protects revenue. The difference shows up in customer trust, finding closure, and how often jobs stall at the paperwork stage rather than the technical one.

Safety and compliance don't sit outside the business model. In aerospace MRO, they are the business model.

That doesn't mean every compliance investment is wise. It means the cost must be linked to capability and return. A repair station that expands ratings without a realistic sales path can bury itself in quality overhead. A shop that refuses to invest in process control can end up stuck in low-value work because customers won't trust it with more critical packages.

For teams building a safety culture, it also helps to expose managers and technicians to practical safety thinking outside their internal manuals. Resources focused on reliable aviation safety can be useful as a supplemental lens, especially when organizations want broader operational awareness instead of treating safety as a checklist exercise.

For PE buyers, the diligence implication is straightforward. Don't just ask whether certifications exist. Ask whether the organization can consistently operate inside them. The moat only matters if the company can defend it every day on the hangar floor.

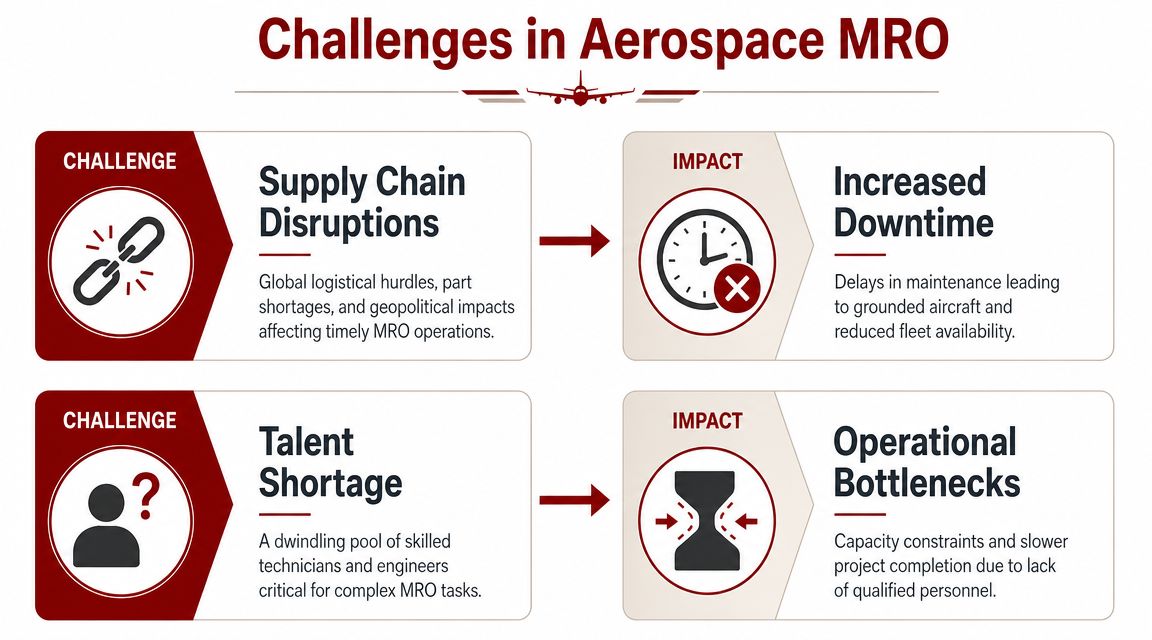

Confronting the Twin Crises Supply Chain and Talent

The MRO capacity problem is usually described in two separate buckets. Parts are hard to get. Skilled people are hard to find. In practice, these are not separate problems. They reinforce each other.

The aerospace MRO industry faces a widening disconnect between retiring senior engineers and newer entrants who often lack aircraft-specific hands-on knowledge. Recent commentary argues the problem is less about simple hiring and more about knowledge transfer and industrial design, and that success depends on integrating supply chain and production into one operating model with technicians involved in system design, according to BCG's analysis of the aerospace experience gap.

Capability resilience is the real issue

When an experienced technician retires, the company doesn't just lose labor hours. It often loses judgment. That includes how to inspect ambiguous damage, how to interpret legacy conditions, how to sequence a repair efficiently, and when a material or tooling issue is about to become a schedule problem.

Now combine that with a weak supply chain. A less experienced team waiting on uncertain parts tends to make poorer planning decisions. Jobs sit open longer. Queues get distorted. Supervisors start expediting the wrong work. The organization becomes reactive.

That's why I view the issue as capability resilience. The shop must keep performing when inputs are messy, drawings are incomplete, and customer expectations don't move.

A resilient operator usually has these traits:

- Cross-functional planning: Supply chain, production, quality, and engineering make decisions together instead of handing off problems downstream.

- Technician-led feedback loops: The people doing the work help shape routings, kits, inspection points, and documentation changes.

- Structured knowledge capture: Tribal knowledge gets converted into work instructions, visual standards, and repeatable training routines.

- Prioritized material strategy: Critical parts and consumables receive different planning treatment than generic inventory.

A talent shortage becomes a margin problem when knowledge stays in people's heads. A supply chain problem becomes a customer problem when planning and production aren't integrated.

What disciplined operators do differently

Weak businesses respond to these pressures with overtime, expediting, and constant reprioritization. That can keep airplanes moving for a while, but it usually degrades quality and burns out the best people.

Disciplined operators take a different approach.

First, they identify which tasks depend on deep legacy knowledge. Not every activity does. Some jobs can be standardized aggressively. Others require guided escalation, richer documentation, and tighter review. Second, they redesign flow around realistic parts assumptions instead of optimistic dates. Third, they treat lead technicians as process designers, not just labor inputs.

That last point matters a lot. New software doesn't fix a work package built on missing knowledge. More recruiters don't solve a training model that never captured what the last generation knew. The best MRO organizations build systems that help average performers become reliable and help experts transfer judgment without slowing the operation to a crawl.

For an investor, this is one of the clearest quality signals in the market. Ask whether the company can explain how it preserves know-how and adapts when material flow breaks down. If management can't answer that cleanly, future growth will be harder than the forecast suggests.

Digital MRO Hype Versus Hangar-Floor Reality

Digital transformation in aerospace gets sold like a cure. Predictive maintenance. Connected aircraft. Digital twins. Modern planning suites. Mobile work instructions. Most of it sounds sensible. Some of it is valuable. A surprising amount of it disappoints.

Why? Because software usually gets layered on top of weak process design. The company automates confusion, then wonders why the dashboard is impressive and the turnaround time isn't.

Why software disappoints

Recent industry analysis says the global MRO market fully recovered to over $114 billion in 2024, but throughput remains constrained by labor shortages, parts availability, and the need to redesign planning and execution systems, not just add more point tools. The same analysis argues that the strongest returns come from process redesign and integrated systems, not incremental technology adoption alone, according to Oliver Wyman's MRO industry view.

That aligns with what experienced operators already know. A digital task card doesn't create clean work scope. An analytics layer doesn't fix poor kitting. A predictive model doesn't help much if the shop still lacks the labor or material availability to act on the signal.

Common failure patterns show up again and again:

- Bad master data: Part numbers, routings, labor standards, and effectivity data aren't trustworthy.

- Workflow mismatch: The software assumes an ideal process that isn't adhered to by the hangar or shop floor.

- Technician exclusion: Systems get selected by management and IT, then imposed on the workforce that has to use them under time pressure.

- Fragmented tools: Planning, supply chain, quality, and execution each live in separate environments with weak handoffs.

Where digital actually pays off

Digital tools work best when they're applied after core operating questions are answered. What is the standard job flow? Where does work wait? What information do technicians need at the moment of execution? Which approvals create bottlenecks? Which shortages repeatedly delay closure?

Buy software to amplify a working system, not to rescue a broken one.

That's why the highest-return digital efforts in MRO often look less glamorous than the marketing decks. Better work-scope visibility. Cleaner electronic records. More reliable materials status. Faster discrepancy review. Tighter integration between planning and execution. Those changes don't make conference headlines, but they improve throughput and customer confidence.

For founders, the practical sequence is simple. Standardize first. Simplify handoffs second. Involve technicians in design third. Then digitize what helps the work move. Investors should underwrite digital plans the same way. If management talks only about tools and not about process redesign, be careful. In MRO, operational reality always beats software ambition.

The Investor's Playbook Scaling and Exiting in Aerospace MRO

An MRO business becomes valuable when it can do difficult work repeatedly, under compliance pressure, with predictable customer outcomes. Everything else is secondary.

That sounds obvious, but many acquisitions are still underwritten off revenue mix and customer logos without enough attention to process capability. The better approach is to evaluate MRO the way a seasoned industrial investor would evaluate any high-consequence service platform. What can this company do that others can't do easily? How reliably can it convert that capability into cash? And how scalable is the operating model without diluting quality?

What to diligence before you buy

One of the clearest value indicators in specialized MRO is the ability to return difficult legacy parts to service when the data package is incomplete. In structural and tubing work, MRO often means restoring a part to a certifiable state when original drawings are missing, which requires reverse engineering, nondestructive inspection, weld-repair qualification, and dimensional verification. If any one of those steps fails, the part cannot re-enter service, according to Lafarge & Egge's discussion of aerospace tubing and welded-assembly MRO.

That is more than a technical detail. It is a business filter. A company that can solve those problems has a capability customers struggle to replace, especially on aging fleets and custom configurations.

When diligencing an MRO target, I'd focus on questions like these:

- Capability depth: What repairs or overhauls can this shop perform that customers cannot readily dual-source?

- Certification fit: Do the ratings and approvals match the actual commercial strategy, or is there a gap between ambition and authorized scope?

- Labor systemization: Is expertise concentrated in a few individuals, or has the company built a repeatable operating system?

- Material exposure: How often do jobs stall for parts, outside processing, or missing technical data?

- Revenue quality: Are customer relationships sticky because of capability and performance, or just incumbency?

- Management discipline: Does leadership understand throughput, margin leakage, and quality risk at the job level?

A broader investment lens also matters, especially for buyers assembling industrial platforms. Operators who understand private equity in industrial businesses and platform-building strategy tend to ask better questions about integration, management depth, and exit pathways.

How value gets created and realized

Scaling in aerospace MRO usually follows one of two paths. Organic expansion into adjacent capabilities, or acquisition of complementary specialists. Both can work. Both can fail.

Organic growth works when the company already has strong process control and a clear customer pull for adjacent work. A component shop may add a related repair family. A structural specialist may expand into neighboring assemblies. This path tends to preserve culture and quality better, but it takes patience.

M&A works when the buyer has a real integration thesis. Not just "bigger is better," but a specific view on capability coverage, cross-selling, shared quality systems, planning discipline, and leadership structure. Roll-ups that ignore operational fit usually create complexity faster than value.

A practical playbook for building enterprise value looks like this:

- Own a niche first: Start with a capability that customers need and competitors can't easily replicate.

- Standardize execution: Build routings, training, inspection control, and quoting discipline around that niche.

- Expand selectively: Add adjacent work only when certification, labor, and process maturity can support it.

- Protect customer trust: In this industry, one quality failure can undo years of relationship equity.

- Build exit logic early: Strategic buyers and PE firms pay for durable capability, not just top-line growth.

The best exits usually come from businesses that combine technical scarcity with operational consistency. Buyers will pay for a trusted repair niche, a clean quality culture, resilient management, and recurring customer reliance. They won't pay the same multiple for a shop that is busy but chaotic.

If you're looking at MRO in aerospace as an investment thesis, the sector offers real upside. But it rewards operators who respect complexity. This is not a market where spreadsheets alone tell the story. The balance sheet matters. The certification structure matters. The workflow matters. The people who can turn damaged hardware into airworthy product matter most of all.

Hasit Vibhakar brings the kind of operating perspective this market demands. If you're evaluating an aerospace MRO acquisition, building an industrial platform, or looking for experienced insight on scaling complex manufacturing and aftermarket businesses, visit Hasit Vibhakar.

Leave a Reply