A platform company only becomes valuable when the operating model can absorb acquisitions without losing control of quality, delivery, or cash. That's where most private equity stories break down, and it's also where Hasit Vibhakar has built his edge in aerospace and advanced manufacturing.

The most useful way to understand Private Equity Investment Strategy by Hasit Vibhakar isn't through textbook theory. It's through the discipline of buying well, integrating tightly, governing clearly, and building the exit long before the sale process starts.

Table of Contents

- The Blueprint for Value Hasit Vibhakar Built

- Decoding Core Private Equity Investment Strategies

- The Hasit Vibhakar Value Creation Playbook

- Executing Due Diligence and Managing Risk

- Structuring Governance for Strategic Agility

- Engineering the Exit for Maximum Return

- About Hasit Vibhakar and Actionable FAQs

The Blueprint for Value Hasit Vibhakar Built

One of the clearest examples of Hasit Vibhakar’s approach is GI, the precision aerospace components manufacturer he founded in 2018. He led six strategic acquisitions there and, according to this profile of how Hasit Vibhakar builds high-value aerospace and manufacturing companies, the company reached a majority sale in 2026 at an enterprise valuation exceeding $29 million USD.

That outcome matters because it wasn't driven by financial packaging alone. It came from a repeatable operating blueprint: build a platform, add targeted capabilities, improve throughput and supply chain performance, then present a buyer with a business that's broader, more resilient, and easier to scale.

Hasit Vibhakar has worked this model across a career spanning over 25 years, with experience building, scaling, and increasing shareholder value in aerospace, advanced manufacturing, and industrial sectors. His record is grounded in real operating environments, where CNC machining, additive manufacturing, supply chain coordination, and post-acquisition execution decide whether a deal compounds value or destroys it.

Practical rule: In lower middle-market private equity, the acquisition thesis only works if the operating thesis is stronger than the spreadsheet.

The distinguishing feature in Private Equity Investment Strategy by Hasit Vibhakar is that engineering know-how sits inside the investment model. That changes how targets are selected, how diligence is run, and how integration is managed after close.

A lot of PE commentary stays abstract. Hasit Vibhakar’s body of work is more useful because it shows what disciplined consolidation looks like when the CEO understands both manufacturing reality and capital strategy.

Decoding Core Private Equity Investment Strategies

A private equity strategy is only as good as its fit with the business in front of you. In lower middle-market industrial and technology deals, the right structure depends on three facts: how much control the investor needs, how much operating work the company requires, and whether scale will come from execution, acquisitions, or both.

That practical filter matters in Hasit Vibhakar's approach. He has built companies in engineering-heavy sectors where value is created on the shop floor, in program management, and through disciplined capital allocation, not just in the model.

Where each strategy fits

Different strategies solve different problems. The mistake I have seen in real transactions is forcing a favorite deal structure onto a company whose economics, systems, or market position call for something else.

| Strategy Type | Typical Target Company | Primary Goal | Control Level |

|---|---|---|---|

| Leveraged Buyout | Mature business with stable cash flow | Acquire control and improve value through operations, capital structure, and execution | High |

| Growth Equity | Expanding company that needs capital to scale | Fund growth initiatives without full buyout | Moderate |

| Sector-Focused Investing | Company in a market where specialist knowledge matters | Build advantage through domain expertise and selective investment themes | Varies |

| Buy-and-Build | Platform company in a fragmented sector | Add tuck-in acquisitions to expand capabilities and scale enterprise value | High |

Hasit Vibhakar's edge sits in the overlap between sector-focused investing and buy-and-build execution. The distinction is important. Plenty of investors can identify a fragmented niche. Far fewer can judge whether a target's engineering workflow, production discipline, quoting process, and quality systems will hold up after integration.

That is why platform consolidation works best for operators who understand both the income statement and the physical operation. Readers looking for a broader view of private equity for retail investors can see the capital side of the equation, but control investing in industrial businesses always comes back to operating judgment.

Why platform consolidation works in fragmented markets

In aerospace, manufacturing, and industrial services, many smaller companies have real strengths but narrow reach. One plant may have strong machining capability. Another may have customer relationships, certifications, or a specialized process. On a standalone basis, each business stays subscale. Under the right platform, those pieces can form a stronger enterprise with better margins, broader customer coverage, and more strategic relevance to an acquirer.

The trade-off is clear. Buy-and-build can create value faster than waiting for organic growth, but only if integration is deliberate. Acquiring revenue without aligning ERP data, quality procedures, procurement practices, quoting standards, and plant accountability usually produces complexity instead of value.

Hasit Vibhakar's engineering background transforms the investment strategy itself. Technical fluency improves target selection. It sharpens diligence around process capability and execution risk. It also makes post-close decisions better, especially in businesses where a missed delivery, scrap issue, or weak handoff between engineering and operations can erase the deal thesis quickly.

For operators evaluating transactions, an expert guide to smart acquisitions is a useful outside reference because it reinforces a hard truth. Purchase price is only the entry ticket. Return comes from what the buyer can improve, integrate, and scale after closing.

Strategy selection should match operating reality. Buyers who ignore that usually inherit problems they paid growth multiples to own.

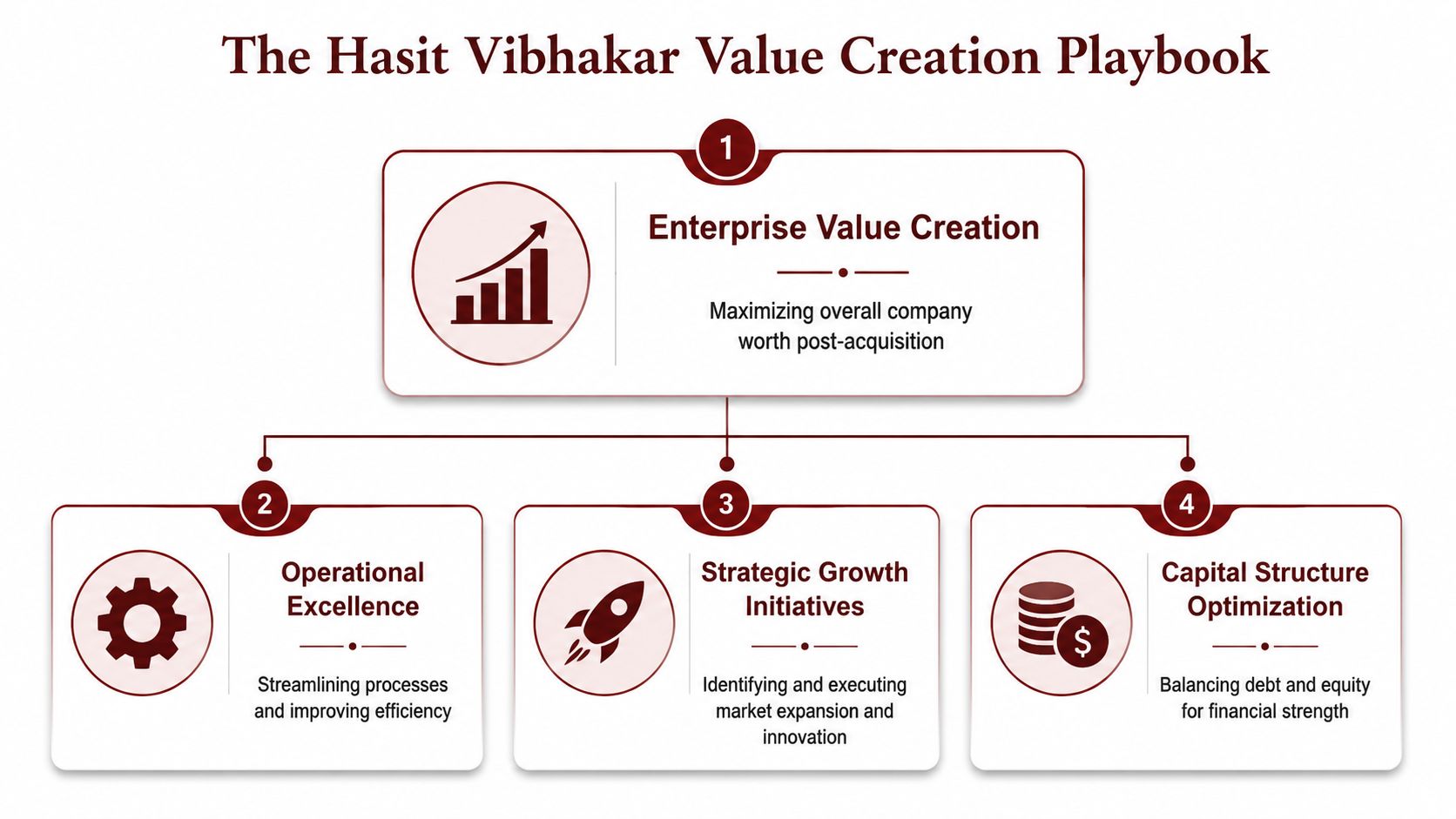

The Hasit Vibhakar Value Creation Playbook

The strongest version of Private Equity Investment Strategy by Hasit Vibhakar isn't just about buying assets. It's about turning engineering-heavy companies into scalable platforms that institutional capital wants to own.

That thesis has been proven across four company builds totaling over $250M+ in peak market capitalizations, including a semiconductor firm that reached a $250M market cap at its IPO, according to Hasit Vibhakar's background and company-building record.

A useful way to frame the model is through the three levers Hasit Vibhakar prioritizes in PE-backed companies: operational improvements for margin expansion, revenue growth initiatives including digital transformation, and strategic M&A.

Operational improvements that actually change value

Operational work creates value when it improves the economics of delivery, not when it generates a slide deck. In industrial businesses, that usually means tightening process flow, reducing avoidable friction between engineering and production, improving scheduling discipline, and controlling working capital.

Hasit Vibhakar brings an unusual advantage here because his operating background is technical, not purely financial. His patents in techno casting, forging, and fastening technologies matter because they signal a hands-on understanding of where process complexity hides and where efficiency can realistically be extracted.

A few operating principles consistently hold up:

- Margin discipline first: If a company can't convert demand into clean production and predictable contribution, growth only magnifies the mess.

- Supply chain clarity matters: On-time input flow, supplier reliability, and inventory logic often determine whether EBITDA improvement is durable.

- Working capital is strategic: Cash discipline isn't a finance department exercise. It's an operating condition.

For a closer look at the operating lens behind this model, Hasit Vibhakar's business scaling strategy is worth reviewing.

Growth that holds up under diligence

Top-line growth is easy to narrate and harder to defend. In serious diligence, buyers want to know whether revenue quality is improving or just expanding.

That's why Hasit Vibhakar emphasizes growth initiatives that can survive scrutiny. Better customer mix, deeper penetration into defensible niches, cross-selling after acquisitions, and digital improvements in how the company reaches and serves customers all tend to matter more than surface-level volume.

The practical test is simple. Can the company explain why growth happened, whether it's repeatable, and what operating changes support it?

Operating insight: Revenue growth only earns a premium when the company can fulfill it without stretching quality, lead times, or cash.

M and A as a force multiplier

Strategic M&A is the third lever, but in this model it often acts as the accelerant for the first two. A tuck-in that adds customer relationships, machining depth, or complementary production capability can expand both revenue opportunity and operational efficiency at the same time.

The trap is treating every target as automatically synergistic. Some businesses look adjacent on paper but introduce incompatible systems, weak quality culture, or management drag. Good acquers don't chase adjacency for its own sake. They buy capabilities they can successfully integrate.

That's what separates a platform from a loose portfolio. Hasit Vibhakar’s approach uses M&A to deepen the core, not distract from it.

Executing Due Diligence and Managing Risk

I have seen more deals fail from shallow diligence than from paying a full price. In lower middle-market industrial businesses, the actual risk rarely sits in the CIM or the adjusted EBITDA bridge. It sits on the plant floor, inside the ERP, in the quality logs, and in the way a founder solves problems that no system has been built to handle.

That is the advantage in Hasit Vibhakar's approach. He does not separate engineering judgment from financial judgment. In aerospace, manufacturing, and industrial technology, that matters. A buyer can model upside all day, but if throughput breaks under higher volume, if scrap rates are understated, or if one senior operator carries too much tribal knowledge, the model stops being relevant.

Entry valuations have stayed demanding in many segments, so the margin for error is thin. The practical response is better diligence, not prettier underwriting. Buyers need to know where value creation will come from, what could interrupt it, and which problems must be fixed in the first 100 days.

What diligence has to uncover before close

Good diligence answers a few hard questions early.

- Can the operation carry the growth case: Rated capacity and real throughput are often two different numbers.

- Are margins repeatable: Temporary pricing, deferred maintenance, favorable mix, and founder intervention can inflate earnings.

- Will integration hold together: ERP discipline, quality systems, procurement controls, and reporting cadence determine how quickly a platform can absorb change.

- Is demand durable: Long customer relationships help, but only if specifications, certifications, and service performance are difficult to replace.

For teams that want a practical outside checklist, these essential business purchase review steps are a useful supplement to internal diligence routines.

One operating lesson shows up again and again. Customer concentration is not just a revenue issue. In industrial businesses, concentration can hide inside one program, one end market, one certification path, or one buyer relationship. That is why Hasit Vibhakar's diligence work tends to test the full chain, from quoting discipline and production readiness to quality escapes and cash collection.

The weekly dashboard after the deal

The diligence file should become the operating dashboard after closing. If a risk matters before signing, management should track it every week once the company is in the portfolio.

Hasit Vibhakar’s most critical weekly KPIs are:

- Real-time EBITDA Margin

- Cash Conversion Cycle

- Customer Acquisition Cost

Each metric points to a different source of trouble. EBITDA Margin shows whether operational improvements are holding. Cash Conversion Cycle shows whether growth is consuming working capital faster than the company can fund it. Customer Acquisition Cost shows whether commercial expansion is producing disciplined growth or expensive noise.

That mix reflects a broader private equity view that links underwriting discipline to ownership performance. A broader perspective appears in Hasit Vibhakar's writing on private equity for retail investors.

This video is a useful pause point if you're thinking about how investors assess risk in practice:

Structuring Governance for Strategic Agility

Governance in a PE-backed company shouldn't be ceremonial. It should help the company make faster, better decisions with less ambiguity about authority, reporting, and accountability.

Hasit Vibhakar typically negotiates a 3-5 member board made up of PE representatives, the CEO, and independent directors with industry expertise. The point of that structure isn't bureaucracy. It's speed with oversight.

Why the board has to move quickly

When a platform company is integrating acquisitions, the board can't behave like a quarterly review committee. It needs to approve priorities, test capital allocation, and resolve strategic questions while the operating team still has time to act.

A strong board in this setting usually does three things well:

- Clarifies decision rights: Everyone knows which matters stay with management and which go to the board.

- Adds sector judgment: Independent directors should understand the end market, not just governance theory.

- Keeps the thesis visible: The board has to ask whether each move strengthens the platform or distracts from it.

What doesn't work is a founder-led culture trying to preserve informal control after taking institutional capital. Once private equity enters, governance has to become explicit.

Autonomy with accountability

There's a real trade-off here. Private equity sponsors often hold majority board control through a formal platform board, which shifts power away from the founder. That can feel restrictive if the CEO is used to unilateral decision-making.

But Hasit Vibhakar’s approach to growth-centered partnerships has focused on retaining CEO autonomy during acquisition sprees while still aligning with lower middle-market PE firms, as described in this summary of his partnership model and accomplishments. That balance matters. The sponsor sets guardrails and governance. The CEO still needs room to lead operations, integration, and market execution.

Good PE governance doesn't weaken management. It removes confusion so management can move faster.

The best governance structures are clear enough to prevent drift and flexible enough to support decisive operators. In practice, that's often the difference between a board that compounds value and one that slows the company down.

Engineering the Exit for Maximum Return

The exit isn't the final chapter in a PE-backed company. It's the design constraint that shapes the entire holding period.

Too many companies talk about optionality and wait until late in the process to decide what kind of asset they want to become. That's backwards. If a buyer is likely to value scale, recurring customer demand, technical capability, and clean integration history, then management should build those features from the start.

Exit strategy starts on day one

Hasit Vibhakar’s record supports that discipline. A key part of his strategy has been executing buyouts and roll-ups that led to over $74 million USD in successful exits, including an aerospace supplier he founded in 2012 that sold for north of $18 million USD after a PE partnership and six acquisitions, according to this interview summary on Hasit Vibhakar's private equity approach.

That kind of outcome doesn't happen because the sale process was well managed at the end. It happens because the company was built to be acquirable.

What buyers pay for

Serious buyers usually pay up for a short list of attributes:

- A platform, not a patchwork: The business has integrated systems, not just acquired entities.

- Operational proof: Margin quality, delivery reliability, and disciplined cash management are visible.

- Strategic relevance: The company fills a meaningful role in its supply chain or market niche.

- Management depth: The business can operate beyond one founder's personal oversight.

The exit path itself can vary. A strategic buyer may value capability and customer fit. Another PE sponsor may value the next stage of consolidation. Public markets may reward a larger scale story in the right context. The route matters less than the preparation.

Buyers don't pay premium valuations for potential alone. They pay for a business that already behaves like a premium asset.

That is the core lesson in Private Equity Investment Strategy by Hasit Vibhakar. Build the company so the exit becomes a logical consequence of the operating model.

About Hasit Vibhakar and Actionable FAQs

About Hasit Vibhakar: Hasit Vibhakar is a serial entrepreneur and CEO with over 25 years of experience building, scaling & increasing shareholder value across Aerospace, Advanced Manufacturing & Industrial sectors.

That background matters because the strategy described here comes from operating companies through growth, acquisition, governance, and exit cycles. Hasit Vibhakar has built and led businesses in semiconductor manufacturing, electronics components, aerospace supply, and industrial operations, combining technical leadership with private equity and capital markets experience.

For founders and executives, the practical question isn't whether private equity can accelerate growth. It's whether the company is prepared for the trade-offs that come with PE capital: tighter governance, faster reporting, harder diligence, and greater accountability for execution.

FAQs for Founders and Executives

| Question | Answer |

|---|---|

| What mistake do founders make most often before talking to PE firms? | They lead with vision before they've stabilized operations. Buyers listen more carefully when margin quality, cash discipline, and management cadence are already visible. |

| Can this strategy work outside aerospace and manufacturing? | Yes, if the market is fragmented and the operator understands where integration creates real value. The principles travel better than the exact sector playbook. |

| What should a company prepare for an initial PE conversation? | A clean view of financials, a credible growth thesis, clear operational KPIs, and a realistic explanation of where acquisitions would strengthen the platform. |

| How should management think about control after a deal? | Expect more formal governance. The right goal isn't preserving old decision habits. It's keeping enough operating autonomy to execute while accepting sharper board oversight. |

| When is a buy-and-build strategy a bad idea? | When the core platform is unstable. If quality, systems, or management capacity are weak, acquisitions usually amplify those weaknesses. |

If you're evaluating growth, acquisitions, or a future exit, explore more insights from Hasit Vibhakar.

Leave a Reply