India's reported 100 million fiber-kilometers per year of manufacturing capacity exceeds its own domestic annual consumption, according to an industry note that also says the global fiber optic cable market was expected to grow from USD 8,834.2 million in 2022 to USD 13,160.0 million in 2027 at an implied 8.58% CAGR (industry manufacturing note). That's the number that should reset how investors think about fiber optics manufacturing.

This isn't a simple “materials in, product out” business. It's a precision manufacturing sector where quality failures start as process drift, where throughput is constrained by a few unforgiving steps, and where scale changes the economics fast. For a private equity partner, the key question isn't whether fiber demand exists. It's whether a target can convert capital, process control, and supplier discipline into reliable output without destroying yield.

Most commentary stops at the science. That misses the investment case. The business of fiber optics manufacturing is built on preform strategy, draw discipline, uptime, qualification cycles, and the ability to scale without letting tiny defects become expensive customer claims.

Table of Contents

- The Core Process of Fiber Optics Manufacturing

- Essential Materials and the Supplier Ecosystem

- Equipment Automation and Production Lines

- Quality Control and Precision Inspection Methods

- Scaling Production and Managing Throughput

- Analyzing CAPEX OPEX and Key Cost Drivers

- Strategic Investment and Market Outlook for 2026

The Core Process of Fiber Optics Manufacturing

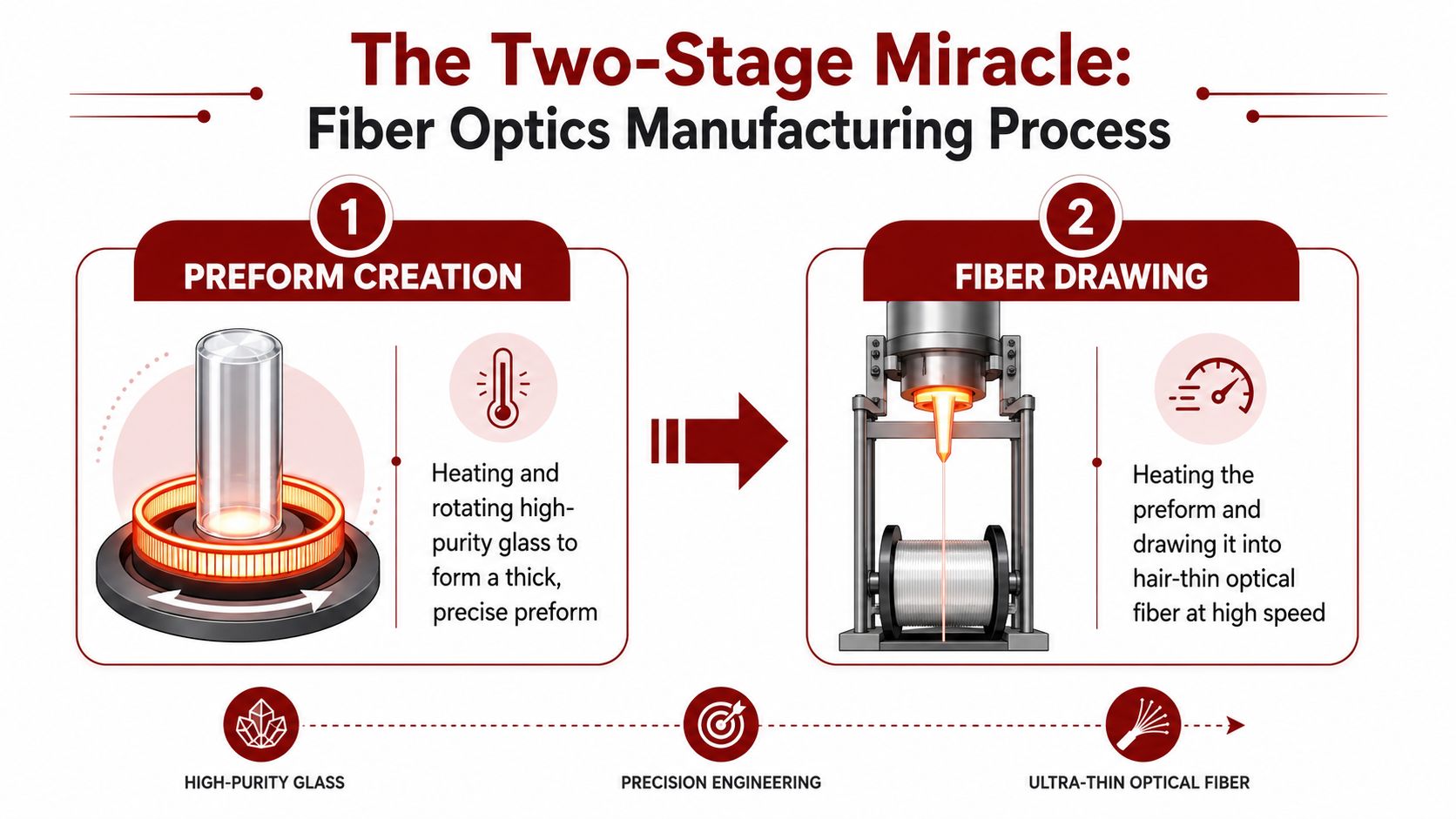

At the operational level, fiber optics manufacturing comes down to a two-stage transformation. First, the producer creates a highly engineered glass preform. Then that preform gets heated and drawn into extremely thin optical fiber with almost no room for process error.

From engineered glass to usable fiber

The preform is the economic heart of the product. Think of it as a large, carefully built glass cylinder whose internal structure determines what the finished fiber can and can't do. If the chemistry and geometry are wrong at this stage, the draw tower won't rescue you later.

The second step is the draw. The preform is fed into a draw furnace, softened, and pulled downward into a continuous strand. The closest executive analogy is hot taffy, but with far tighter tolerances and far higher consequences for variation.

In the critical preform-to-fiber draw stage, industry guidance describes glass heated to roughly 1,800 to 2,200°C, drawn at about 10 to 20 m/s, with tension held near 50 to 100 g. The same reference notes that a single preform can yield about 100 km of fiber in 1 to 2 hours, and warns that tension or thermal drift can create microfissures, diameter instability, and higher attenuation risk (draw process reference).

Why process precision drives enterprise value

This is why investors should care about process control more than glossy factory tours. The draw step is where revenue quality gets determined in real time. If furnace behavior, tension control, diameter measurement, coating timing, and spool handling aren't integrated, yield drops and claims arrive later.

A strong operator treats the line as a closed-loop control problem, not a collection of machines. That's where practical instrumentation matters. Teams building or upgrading these facilities often benefit from specialized process-control guidance such as E & I Sales expertise because the issue usually isn't buying equipment. It's making multiple systems behave like one stable production environment.

Practical rule: In fiber optics manufacturing, the process window is the product. If management can't define its control limits clearly, it probably can't scale them profitably.

From an investment standpoint, the core diligence questions are straightforward:

- Preform capability: Can the plant produce consistent preforms internally, or does it depend on outside supply for the most value-critical input?

- Draw stability: Does the operation hold stable performance across long runs, or only under ideal demonstration conditions?

- Recovery discipline: When the line drifts, does the team have documented root-cause and correction routines, or does it rely on operator heroics?

Plants that answer those questions well tend to build durable customer trust. Plants that don't usually compete on price until they can't.

Essential Materials and the Supplier Ecosystem

The material stack in fiber optics manufacturing looks simple from a distance. It isn't. What matters isn't just having silica and additives. What matters is getting the right purity, the right consistency, and the right supplier behavior under pressure.

Why purity is a commercial issue

The base material is ultra-pure silica. Around that foundation, manufacturers use dopants to tune refractive behavior and build the optical characteristics required by the end application. For executives, the important point isn't the chemistry lesson. It's that small upstream variation can create large downstream cost.

If raw material quality drifts, the problem won't stay confined to incoming inspection. It shows up in preform consistency, draw stability, attenuation outcomes, and qualification performance with telecom or data infrastructure customers. That's why supplier quality in this sector belongs in the same conversation as production yield.

There's also a structural market backdrop behind sourcing strategy. IBISWorld reports that the number of fiber-optic cable manufacturing businesses in the United States grew 5.1% per year on average from 2020 to 2025, while Grand View Research estimates the global fiber optics market at USD 10.76 billion in 2025 and projects USD 17.95 billion by 2033 at a 6.6% CAGR. Another industry forecast places the broader fiber optic cable market at USD 13 billion in 2024 and USD 34.5 billion by 2034 at 10.4% CAGR, identifying single-mode fiber as the largest segment at USD 7.26 billion in 2024 (industry market overview).

What strong supplier strategy looks like

In this sector, a weak sourcing model can hide for a while because quality problems often emerge with a lag. A management team may report line output, but the better question is whether that output converts cleanly into accepted, qualified, repeat business.

A sound supplier model usually includes a few essential elements:

- Qualification depth: Don't rely on paper certifications alone. Validate consistency lot to lot, not just supplier to supplier.

- Geographic diversification: If a critical input is concentrated by region, management needs contingency planning before disruption hits.

- Technical collaboration: The best suppliers don't just ship material. They participate in process problem-solving when a line starts drifting.

- Commercial bargaining power: Dual sourcing sounds attractive, but it only works if both suppliers can meet technical requirements at production scale.

Supplier risk in advanced manufacturing rarely appears as a dramatic shutdown first. It often appears as slower troubleshooting, lower yield, and margin erosion.

That's why disciplined operators treat procurement as a strategic function, not a back-office one. A useful framework for that mindset is strong supplier relationship management, especially when a business is trying to scale while preserving quality. In fiber optics manufacturing, your supplier base is part of your production system whether you admit it or not.

Equipment Automation and Production Lines

A serious fiber plant is a capital system long before it becomes a revenue system. Investors who come from conventional industrial categories often underestimate how much performance depends on automation architecture, not just machine count.

The line is only as good as its control stack

The visible equipment gets most of the attention. Preform fabrication tools, draw towers, coating stations, curing systems, proof-testing equipment, spoolers, and inspection modules all matter. But the essential separator is the control layer that keeps those assets synchronized over long production runs.

Legacy lines can produce acceptable fiber under the care of highly experienced operators. The problem is repeatability. If process knowledge lives mostly in individuals, the plant becomes fragile. Turnover, expansion, and shift variability then become hidden operating risks.

A more mature production line automates the tasks that human judgment performs inconsistently under fatigue. That includes diameter monitoring, tension response, furnace behavior, coating application consistency, UV cure timing, spool change coordination, and defect detection. The point of automation here isn't labor substitution alone. It's preserving the process window.

How investors should think about automation tiers

I'd separate assets into three practical tiers.

The first tier is operator-dependent equipment. It may be cheaper to acquire, especially in carve-outs or distressed situations, but it generally requires stronger supervision, deeper tribal knowledge, and more tolerance for variation.

The second is partially automated lines. These often look attractive because they can raise throughput and consistency without a full greenfield rebuild. They work best when management already understands where scrap and downtime originate.

The third is fully integrated production architecture. That's the most compelling platform when the commercial plan depends on scale, qualification discipline, and long-term customer retention. It also demands stronger implementation leadership because software, sensors, mechanics, utilities, and maintenance routines have to work together from day one.

A private equity diligence lens should focus on these questions:

- Can the line hold specification through shift changes?

- Is preventive maintenance formalized or reactive?

- Does management track process drift before it becomes scrap?

- Can the MES, controls, and quality systems produce credible production history for customers?

The most expensive machine in the building may not be the one that hurts you. The one that hurts you is the asset that fails quietly and corrupts yield.

For operators evaluating modernization, the right benchmark isn't “more robotics.” It's better control, fewer unplanned interventions, and cleaner scale-up. That's exactly where thoughtful investment in robotics and automation in manufacturing becomes strategic rather than cosmetic.

Quality Control and Precision Inspection Methods

In fiber optics manufacturing, quality isn't a final department. It's a production discipline embedded into the line. If a company treats inspection as something that happens after the spool is complete, it's already too late.

What buyers are really purchasing

Customers aren't just buying fiber. They're buying predictable signal performance, field reliability, and confidence that installed networks won't become expensive service problems. That means quality metrics must be translated into business terms.

Attenuation affects signal loss. Mechanical reliability affects installation survival and service life. Tensile performance matters because handling and deployment expose the fiber to strain long before the customer ever thinks about replacement. If the product fails on any of those fronts, the manufacturer doesn't just lose margin. It loses credibility.

Many weak operators make a category error. They chase output volume first, then try to inspect quality in later. That approach usually creates rework, customer friction, and inconsistent release decisions.

Inspection has to be inline and unforgiving

Good plants measure the process while it runs. They monitor diameter, surface condition, coating integrity, and proof performance continuously enough to stop drift before it turns into shipped defect.

The coating step deserves more executive attention than it usually gets. To ensure durability, fiber is immediately coated with protective polymer layers in a chamber with micro-channel flow rates, followed by UV curing in less than 5 seconds. The same technical reference warns that poor control of polymer molecular weight or curing wavelength can cause premature fiber failure under strain, which is especially critical in telecom and aerospace use cases (coating and UV curing reference).

A disciplined quality system usually includes:

- Inline measurement: Catch variation during production, not after inventory accumulates.

- Lot traceability: Tie every spool back to materials, machine state, and operating conditions.

- Release discipline: Separate “produced” from “shippable.” Those are not the same number.

- Customer-spec alignment: Test to the actual application requirement, not to an internal convenience standard.

Board-level takeaway: If management reports utilization but can't show first-pass quality and release reliability by line, you don't yet know the economics of the plant.

There's also a cultural issue. High-performing plants don't normalize minor defects. They escalate them. In a product this sensitive, tiny problems rarely stay tiny once the fiber leaves the building.

Scaling Production and Managing Throughput

Global fiber demand has grown fast, but returns in this sector still hinge on a simpler question. How much qualified product can a plant ship every week without yield erosion, schedule misses, or excess inventory?

That is the operating test private equity should care about. In fiber optics manufacturing, scale is not just a volume story. It is the discipline to convert expensive assets into stable output while keeping qualification status, customer service levels, and cash conversion intact.

Capacity is set by the constraint, not the fastest tool

A draw tower may be the marquee asset, but plant throughput is usually governed by the weakest link across preform supply, draw uptime, coating stability, proof testing, spool handling, or final release. I look for management teams that know their current constraint by line, by shift, and by product family. If they answer with nameplate capacity alone, the operating model is still immature.

Preform availability is a common choke point. If preform production lags, the draw tower sits underused and fixed costs spread over fewer saleable kilometers. If preforms are produced ahead of downstream capacity, inventory builds, cycle time stretches, and management starts reporting output that has not yet converted into revenue. Both scenarios destroy the headline economics that made the asset attractive in the first place.

The competitive setting matters too. As noted earlier, India has built meaningful manufacturing capacity beyond local demand, and China remains the scale leader in the broader fiber market. That changes the investment lens. Throughput is no longer only a factory KPI. It shapes pricing power, export viability, and the plant's ability to win long-term customer programs.

What mature scaling looks like

Well-run plants scale in a controlled sequence. They remove one constraint, prove the gain is real, then move to the next. That sounds obvious, but many management teams try to push line speed before they have stabilized maintenance practices, operator consistency, or release flow.

A useful framework is manufacturing capacity planning for line bottlenecks and staged expansion. The logic applies directly here. A debottlenecking project, an added draw line, and a full capacity step-change produce very different margin, staffing, and qualification outcomes.

From an investor's seat, four indicators separate a credible scale-up from an expensive one:

- Constraint-based planning: Capacity forecasts begin with the limiting step and include real downtime, yield loss, and qualification holds.

- Ramp discipline: Higher line speed is only counted once first-pass release and customer acceptance stay stable.

- Maintenance control: Throughput depends on predictable uptime, spare parts availability, and recovery time after stoppages.

- Commercial alignment: The sales team books against proven output, not against a plant model built on ideal conditions.

Working capital deserves more attention here than it usually gets. Throughput problems often appear first in inventory days, quarantine stock, and delayed conversion of produced fiber into released fiber. A plant can look busy and still be underperforming economically.

If management says output can rise sharply, ask what happens to first-pass yield, release timing, labor loading, spare-parts consumption, and customer qualification risk. A strong team has those answers in operating data, not in ambition.

The best operators do not chase maximum speed every shift. They build repeatability, then scale from it. That is how capacity turns into EBITDA instead of rework, premium freight, and disappointed customers.

Analyzing CAPEX OPEX and Key Cost Drivers

Fiber optics manufacturing is a capital-intensive, utility-dependent, precision labor business. That combination creates attractive barriers to entry, but it also punishes sloppy underwriting. If an investor uses generic manufacturing assumptions, the model will be wrong in the places that matter most.

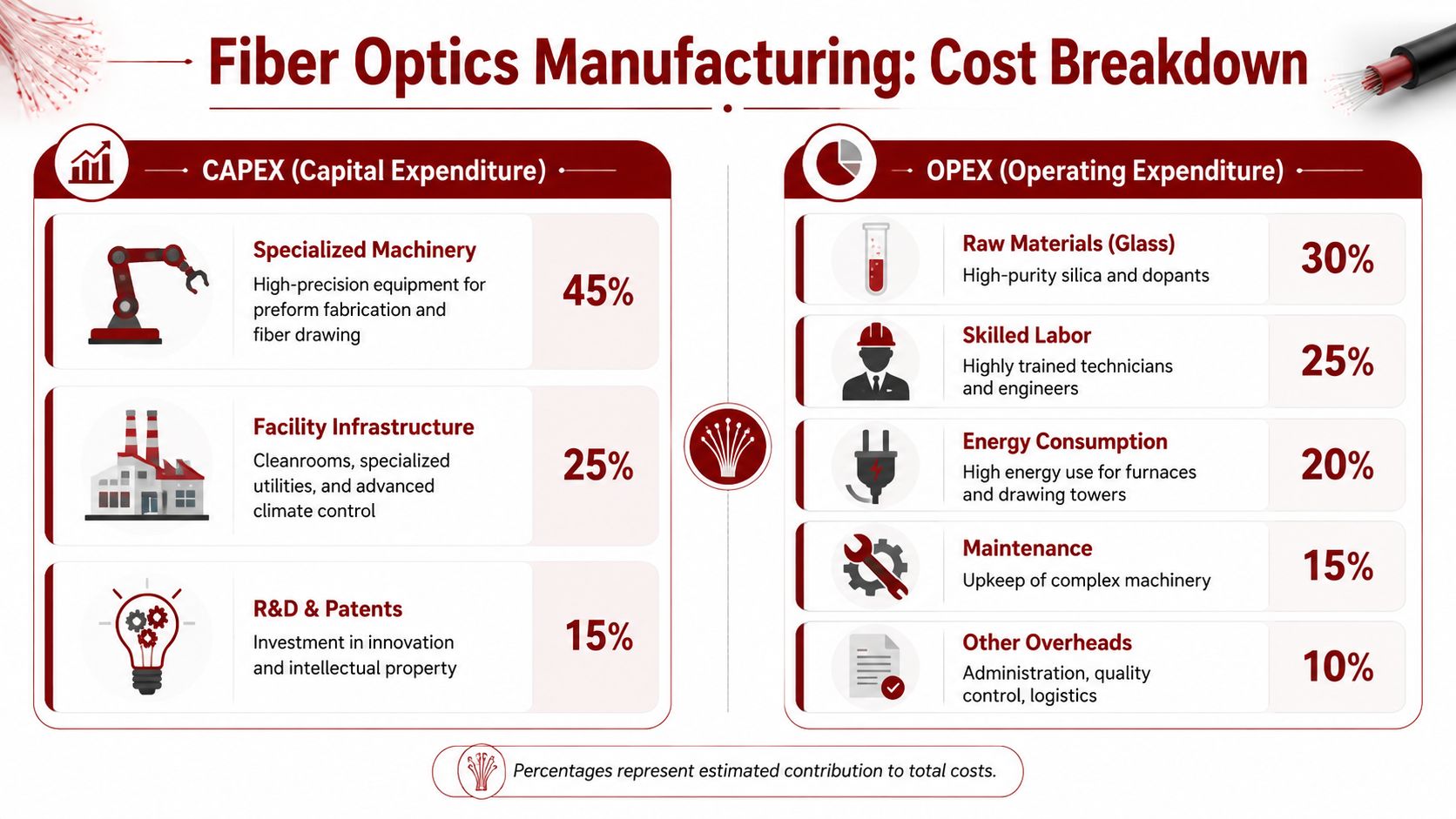

Where the capital goes

The first bill is equipment. A credible operation needs specialized machinery for preform work, fiber drawing, coating, curing, proof testing, winding, and process monitoring. Then come the less glamorous but equally necessary assets: facility infrastructure, environmental controls, power stability, utilities, and quality systems.

The infographic above is directionally useful as a planning aid, but I wouldn't underwrite a deal off generic percentages alone. Actual cost structure depends on whether the company is vertically integrated, what product mix it serves, and how much of the process it owns versus outsources.

A practical way to organize diligence is this:

| Cost Category | Primary Drivers | Typical Share of OPEX |

|---|---|---|

| Raw materials | Purity requirements, dopant mix, supplier consistency | Meaningful and highly quality-sensitive |

| Energy | High-temperature furnaces, utility stability, line utilization | Material because the process is heat-intensive |

| Skilled labor | Process engineers, maintenance talent, trained operators | Elevated due to specialization |

| Maintenance | Preventive service, spare parts, calibration discipline | Often underestimated in weaker models |

| Quality and compliance | Testing, traceability, customer qualification support | Non-discretionary in serious markets |

Where operating margin gets won or lost

Video can help contextualize the production environment and why these costs accumulate across multiple linked systems:

OPEX discipline in this industry usually comes down to four levers.

- Yield preservation: Scrap is expensive because it consumes premium materials, labor time, and machine capacity all at once.

- Energy management: High-temperature processing makes utility reliability and consumption economically meaningful.

- Specialized staffing: You can't flood this business with generic labor and expect stable results.

- Maintenance execution: Deferred maintenance in precision manufacturing usually reappears as variability, downtime, or customer claims.

The mistake I see most often is treating utilization as the main profitability variable. It matters, but not as much as good output. A line running hard while producing avoidable loss, requalification work, or unstable product is burning value, not creating it.

Another common modeling error is to understate the cost of technical leadership. Plants like this need process engineers, controls expertise, quality leadership, and managers who can run disciplined root-cause loops. Those roles aren't overhead fluff. They're central to preserving margin.

If I'm evaluating an acquisition, I want a simple answer to one question: does incremental capital improve stable, shippable throughput, or does it just make the plant more complex? That distinction separates smart CAPEX from expensive self-deception.

Strategic Investment and Market Outlook for 2026

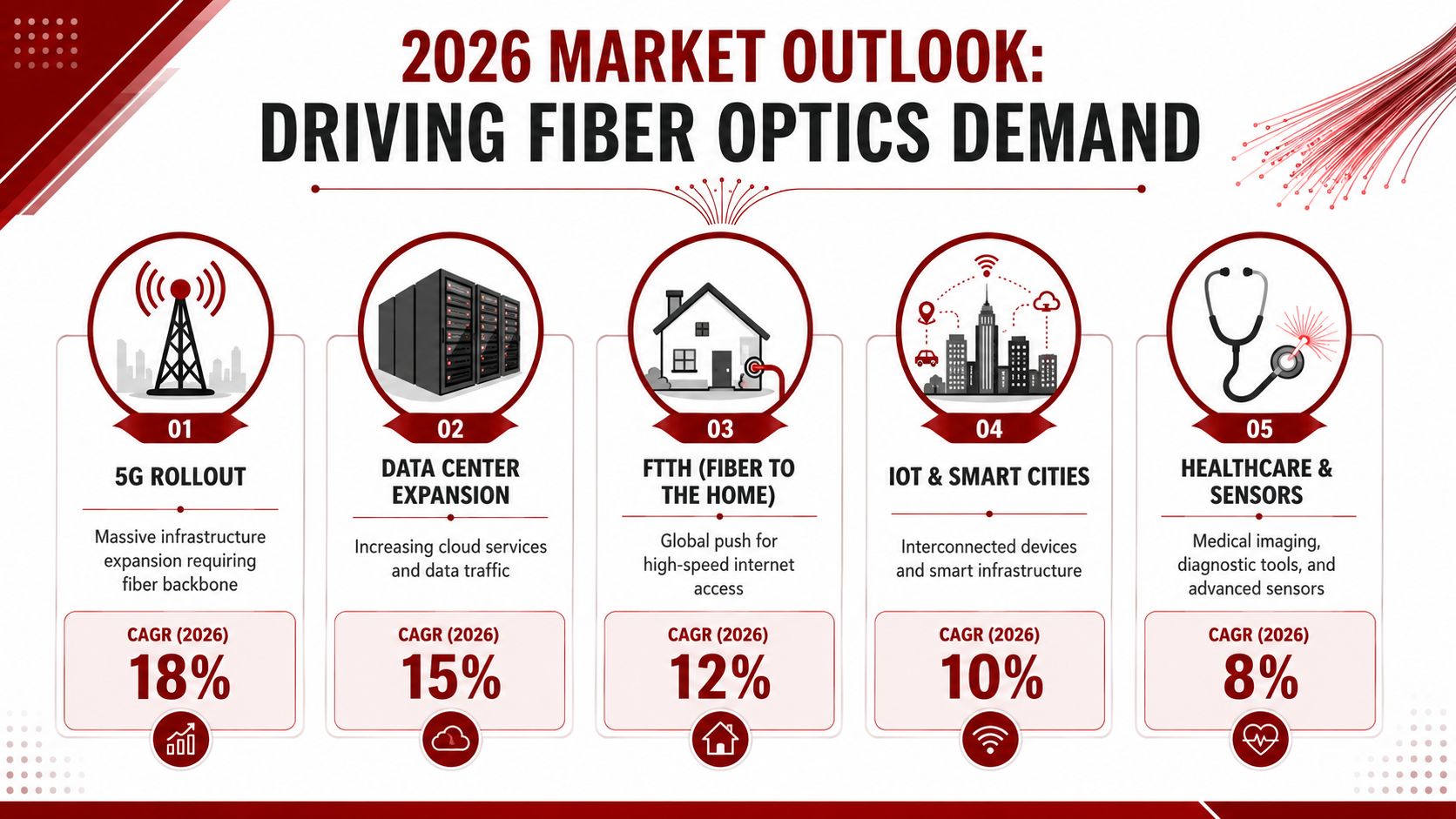

Global fiber demand is still being pulled by telecom upgrades, data center buildouts, and network densification. The investment opportunity is real, but returns will split sharply between disciplined operators and businesses that mistake demand visibility for manufacturing strength.

From an investment standpoint, fiber optics manufacturing should be underwritten as an operating system question first and a market growth story second. The winners in 2026 will be the companies that convert demand into repeatable output, stable qualification performance, and acceptable returns on capital. That is the difference between a good narrative and a good asset.

Where I would look first

I would start with assets that already know their role in the value chain. Some businesses win through volume, procurement strength, and customer confidence in supply continuity. Others win through tighter process control, specialized fiber types, or customer programs that are hard to displace once qualified. Those are different businesses and they should not be valued with the same logic.

For mainstream opportunities, I would favor operators with credible room to expand into telecom, long-haul, and data infrastructure, provided the plant can add output without a step change in instability. Broad demand conditions remain favorable, as noted earlier in the article. The more important question for investors is whether new volume will arrive at healthy contribution margins or get absorbed by rework, claims, and qualification friction.

For differentiated upside, specialty fiber still offers the more attractive asymmetry. NASA-funded research highlighted by Factories in Space points to a potentially valuable niche in ZBLAN and other advanced non-crystalline fiber applications (ZBLAN market opportunity). That is a selective opportunity, not a broad commodity thesis. It belongs in portfolios that can tolerate longer commercialization cycles in exchange for stronger technical defensibility.

In practice, I sort targets into three investable models:

- Commodity-scale play: Attractive when the company has cost discipline, qualified supply, and enough balance sheet strength to withstand pricing pressure and customer concentration.

- Specialty-performance play: Attractive when technical know-how, application support, and qualification history create stickier revenue and better pricing protection.

- Platform consolidation play: Attractive when fragmented operations can be integrated under stronger plant management, quality systems, and commercial controls.

What kills value and how to underwrite around it

The first value trap is technical fragility. If process stability depends on a handful of veteran operators, the company has a succession problem disguised as manufacturing capability. Buyers should test whether yields, attenuation, geometry control, and qualification performance hold across shifts, supervisors, and production campaigns.

The second is supply chain concentration. A fiber business can post healthy margins until one precursor, coating material, or equipment service dependency turns into a bottleneck. At that point, lead times stretch, substitutions become risky, and customer confidence drops faster than management expects. I want to see dual-source thinking, disciplined material qualification, and realistic contingency planning before I give credit for growth.

The third is capital misallocation. I see this repeatedly in industrial diligence. Management adds equipment to chase headline capacity, but the plant has not solved integration, training, maintenance discipline, or process window control. The result is a more expensive operation with more failure points.

A good fiber asset is a plant that can hold specification, protect margin, and earn customer trust repeatedly under real operating pressure.

My 2026 bias is straightforward. Back teams that understand exactly where they create value, can explain which process windows drive commercial performance, and can show that the next dollar of capital will increase dependable shipped output. Avoid businesses built around theoretical capacity, optimistic ramp assumptions, or customer demand that has not been stress-tested against quality and supply execution.

That is how this sector separates into investable platforms and expensive science projects.

Executives and investors evaluating advanced manufacturing opportunities can connect with Hasit Vibhakar for a practical perspective shaped by decades of building, scaling, and exiting industrial and technology-driven businesses.

Leave a Reply