You've built a solid company. Revenue is real. Customers know your name. The team is better than it was a few years ago. Yet organic growth starts to feel slower, more expensive, and less controllable than it used to.

That's usually the point where leaders start looking at acquisition seriously. Not as a vanity move. Not as a financial exercise dreamed up in a boardroom. As a practical growth decision. Buy capability faster than you can build it. Add customers without waiting through another long sales cycle. Expand geography, capacity, talent, or product range in one move.

In industrial and technology businesses, the business acquisition process is rarely elegant. It's messy, human, and highly conditional. Good deals can be ruined by weak diligence, weak communication, or weak integration. Average companies can become excellent platforms if the buyer knows exactly why the target fits and how the combined business will operate after closing.

That's the lens here. Hasit Vibhakar is a serial entrepreneur and CEO with over 25 years of experience building, scaling & increasing shareholder value across Aerospace, Advanced Manufacturing & Industrial sectors. More information can be obtained at Hasit Vibhakar. His perspective matters because it comes from operating businesses, not just advising on them. Over that span, he expanded platform companies through the acquisition of exactly 6 businesses according to his company background. That kind of experience changes how you look at targets, risk, and post-close execution.

Table of Contents

- Your Next Growth Chapter Begins with Acquisition

- Building Your Acquisition Thesis and Sourcing Targets

- Valuation Approaches and Financial Modeling

- Executing a Rigorous Due Diligence Process

- Structuring the Deal and Securing Financing

- Negotiation Strategy and Closing Mechanics

- The Post-Acquisition Integration Playbook

Your Next Growth Chapter Begins with Acquisition

For most founders, acquisition becomes attractive when the old playbook stops producing enough upside. Hiring more salespeople won't solve a capability gap. Launching one more product won't open a new region fast enough. Building from scratch can work, but it often takes longer than the market is willing to wait.

That's why acquisition has become a core strategic tool, not an edge case. Since 2000, the global business acquisition process has facilitated more than 790,000 transactions worldwide with a cumulative known value exceeding 57 trillion USD, according to IMAA M&A statistics. Those numbers tell you something important. Buyers across industries keep using acquisitions because they compress time.

Hasit Vibhakar's operating background is useful here because he comes from sectors where execution matters. In aerospace, advanced manufacturing, industrial supply chains, and technology-enabled businesses, a deal only works if the acquired company fits the platform's operating rhythm. Capacity planning, quality systems, delivery performance, customer trust, engineering know-how, and cash discipline matter as much as headline price.

Why founders misread the moment

A lot of leaders wait too long. They pursue acquisition only after growth has stalled or a competitor has already consolidated the market. By then, they're reacting instead of shaping the field.

The stronger move is to start when your business already has options. You can negotiate better from strength. You can walk away from bad-fit targets. You can fund integration instead of starving it.

Practical rule: Don't buy a business to fix your own operating weaknesses. Buy one to extend a model that already works.

Why local deal mechanics still matter

Even if your strategy is national, the details are still local. Deal terms, entity structure, liability allocation, and transfer mechanics can change materially based on where the business operates and how the transaction is structured. That's why practical legal context matters early, especially in owner-led transactions. If you're evaluating a regional deal, this Wisconsin business acquisition guidance is a useful example of how transaction counsel frames purchase and sale issues in practice.

Acquisition isn't the next chapter because it sounds advanced. It's the next chapter because it lets a capable operator buy time, talent, relationships, and infrastructure that would otherwise take years to build.

Building Your Acquisition Thesis and Sourcing Targets

The first mistake buyers make is starting with listings. The right place to start is with a written acquisition thesis. If you can't describe exactly what kind of company belongs in your portfolio, you'll waste time on meetings that go nowhere and LOIs you shouldn't issue.

Start with fit before flow

An acquisition thesis should answer five practical questions:

- What strategic gap are you filling. Capacity, customer access, product extension, engineering capability, geography, or supply-chain control.

- What operating model can absorb the target. If your platform relies on process discipline, a chaotic founder-led business will create friction fast.

- Which sectors are adjacent enough to understand. Close enough to diligence properly, distinct enough to create upside.

- What kind of owner dependence is acceptable. If too much of the business runs through one person, risk goes up immediately.

- What would make you walk away quickly. Concentrated customers, weak reporting, quality problems, regulatory exposure, or culture that clearly won't integrate.

One benchmark matters more than most buyers admit. The primary predictor of acquisition success isn't just financial alignment but strategic and organizational fit, with 30–50% of failed acquisitions stemming from unaddressed cultural clashes and integration challenges, according to AlignedIQ's acquisition stages analysis.

That's why revenue and EBITDA don't get the first vote. Fit does.

A practical screen for middle-market buyers is owner dependence. If the seller personally controls the key customer relationships, approves every major decision, or drives most of the commercial engine, the buyer isn't acquiring a business. The buyer is renting the founder's presence. In industrial businesses, I'd also screen for dependence on one plant manager, one estimator, one engineer, or one sales channel. Operational fragility hides there.

Off market usually requires sharper thinking

On-market deals are easier to find and easier to benchmark. Everyone sees the teaser. Everyone gets the same CIM. That also means price tension rises quickly, and weak buyers lose time in crowded processes.

Off-market sourcing takes more work, but often produces better conversations because the seller isn't posturing for an auction. Tactics that consistently help include:

- Map the niche first. Build a list by capability, geography, end market, and customer overlap.

- Use direct outreach. Founder-to-founder communication works better than templated broker language.

- Ask advisors who see transitions early. Accountants, lawyers, lenders, and industry service providers often know who is tired, who is succession-constrained, and who may listen.

- Track operational clues. Stalled websites, aging ownership, talent gaps, or underinvested equipment can signal a business that needs a partner.

For industrial buyers, Hasit Vibhakar's perspective on private equity industrials is useful because it frames acquisitions through platform-building logic rather than pure deal activity.

A strong target list is narrow by design. If every company in your market could fit, you don't have a thesis. You have a wish list.

The business acquisition process gets easier once your thesis is clear. Your outreach sharpens. Your screening speeds up. Your team stops chasing deals that look interesting but don't belong in the strategy.

Valuation Approaches and Financial Modeling

Valuation isn't one number waiting to be discovered. It's a range shaped by method, assumptions, and risk. Buyers get into trouble when they confuse a pricing technique with the actual economics of owning the company after closing.

Different methods answer different questions

Three methods dominate middle-market private deals.

DCF asks what the business is worth based on the cash it can generate over time. It's useful when future performance matters more than simple historical comparables, especially if the target has visible operational improvements ahead.

EBITDA multiples are the market shorthand. They're fast, common, and often useful for sanity checking. But they can hide quality issues. Two companies can show similar EBITDA and deserve very different valuations because one has better margins, better delivery discipline, and cleaner working capital behavior.

Precedent transactions help frame what similar businesses have sold for, but private middle-market comparisons are often imperfect. Deal structure, customer mix, founder dependence, and plant condition can make “comparable” deals far less comparable than they appear.

A manufacturing example makes the point. Suppose one target has stable recurring demand from long-term industrial customers but needs capex discipline and cleaner inventory management. DCF may capture the operational upside if you can improve throughput and cash conversion. A simple multiple may undervalue the business if your platform can improve execution quickly. On the other hand, if that same company is heavily dependent on one founder and one major customer, the multiple may be too generous unless you discount for transition risk.

Model the business you are buying, not the story you want

A usable financial model does more than produce an offer price. It tells you what must be true for the deal to work.

Focus on these drivers:

- Revenue quality. Are sales repeatable, contractual, project-based, or founder-carried?

- Margin quality. Are margins supported by pricing power and process control, or by temporary underinvestment?

- Customer concentration. A concentrated book may still be acceptable, but only if you understand switching risk and relationship ownership.

- Working capital behavior. Inventory, receivables, and payables can make a “profitable” business consume cash at exactly the wrong time.

- Capex reality. Deferred maintenance and old equipment eventually show up in buyer returns.

A defensible offer usually comes from triangulation, not devotion to one formula. Run a multiple approach. Run a cash flow view. Pressure-test assumptions against operational facts. Then decide what part of the premium, if any, you're willing to pay for synergy.

Buyers should pay for proven performance. They shouldn't pay today for improvements they still have to execute themselves.

That discipline matters in industrial and technology businesses, where integration complexity can delay value creation. If your model assumes immediate cross-selling, instant system alignment, or effortless plant coordination, the model is optimistic before the ink is dry.

For investors thinking in return thresholds, this perspective on target MOIC in PE deals is a practical reference point for how transaction pricing and value creation need to work together.

One more point matters in off-market transactions. Valuation is often less efficient because there is no broad auction, limited transparency, and fewer clean comparables. That doesn't mean the deal should be cheaper by default. It means your underwriting needs to be tighter. In off-market settings, process advantage often comes from better questions, not faster spreadsheets.

Executing a Rigorous Due Diligence Process

Optimism is put to the test. Buyers can tolerate a lot of uncertainty during sourcing and valuation. They can't afford self-deception during diligence.

Why diligence is where good intentions die

The middle-market business acquisition process follows a standardized 7-step methodology with a total average timeline of 245 days (approximately 6–9 months), and the most critical failure point is the Due Diligence stage (30–90 days), which causes 30–40% of deals to terminate due to financial discrepancies, undisclosed liabilities, or customer concentration risks, according to Acquisition Stars' business acquisition process analysis.

That aligns with what operators see in live deals. Problems rarely appear as a single dramatic issue. They show up as patterns. Reporting is inconsistent. Gross margin logic doesn't hold. Customer concentration turns out to be worse than advertised. Key contracts aren't assignable. The ERP has workarounds nobody documented. Inventory records don't tie cleanly to reality.

A rigorous diligence process has to cover four dimensions together: financial, operational, legal, and cultural. If one is weak, the others won't save the deal.

Comprehensive Due Diligence Checklist

| Diligence Area | Key Focus Items | Example Red Flag |

|---|---|---|

| Financial | Quality of Earnings, revenue recognition, margin trends, normalized EBITDA, working capital, cash conversion, customer concentration | Reported earnings rely on one-time add-backs that don't survive review |

| Operational | Plant efficiency, on-time delivery, scrap and rework patterns, equipment condition, maintenance discipline, ERP and workflow reliability | A key production process depends on undocumented tribal knowledge |

| Legal | Contract assignability, pending disputes, employment issues, IP ownership, environmental exposure, compliance obligations | A major customer contract can't transfer without consent |

| Commercial | Customer retention risk, pricing discipline, pipeline realism, channel concentration, seller-led relationships | Sales depend heavily on the founder's personal network |

| Technology | Core systems, cybersecurity practices, data integrity, reporting architecture, software licensing | Mission-critical data sits in spreadsheets outside the system of record |

| Human capital | Leadership bench, incentive plans, retention risk, cultural norms, management depth | The business has no second layer of managers ready to run functions |

| Supply chain | Vendor concentration, single-source dependencies, lead-time risk, quality performance | One supplier controls a critical input with no validated alternative |

The financial review needs special emphasis. A Quality of Earnings review isn't paperwork for lenders. It's how buyers verify whether reported earnings reflect the actual earning power of the business. In manufacturing, that often means testing freight treatment, labor allocation, inventory adjustments, customer rebates, and whether project work was recognized consistently. In tech-enabled businesses, it can mean looking at churn patterns, implementation costs, support burden, and what portion of revenue is really recurring.

What to hunt for early

The fastest way to improve diligence is to identify potential deal-killers in the first pass.

- Customer concentration risk. One customer may represent more strategic risk than a weak month of earnings ever will.

- Undisclosed liabilities. Warranty exposure, compliance issues, litigation, and off-balance-sheet obligations can survive closing.

- Owner-centered operations. If the business only runs because the founder approves everything, transition risk is high.

- Reporting gaps. If management can't produce clean, timely, reconcilable information during diligence, operating the business after close won't get easier.

Field note: If management explains every inconsistency as a one-off, assume the operating system is the issue until proven otherwise.

Good diligence doesn't just help you decide whether to buy. It also tells you how to negotiate purchase price, structure protections, retention plans, and the first operating priorities after close.

Structuring the Deal and Securing Financing

A well-bought company can still become a bad deal if the structure is wrong. I have seen buyers pay a fair price, then give back value through tax leakage, inherited liabilities, weak working capital terms, or a financing package that leaves no room for a soft quarter after closing.

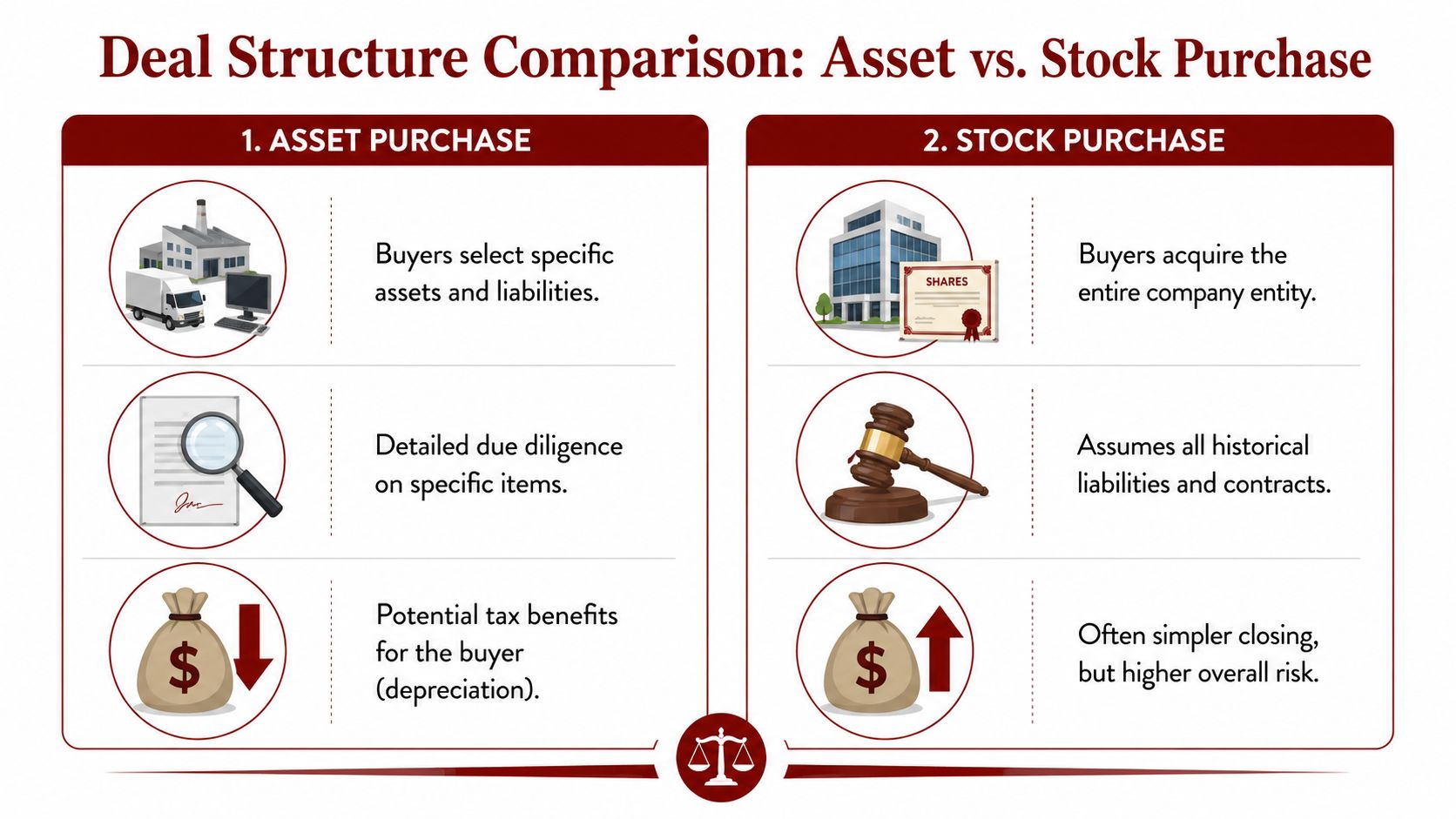

Asset purchase versus stock purchase

The first structural decision is usually simple on paper and messy in practice. Do you buy the assets, or do you buy the entity?

An asset purchase gives the buyer more control over what comes across. That matters in industrial businesses with environmental exposure, warranty history, aged inventory, or unclear obligations tied to old jobs and old customers. It can also create a better tax outcome for the buyer. The cost is execution friction. Contracts may need consent. Licenses and permits may not transfer automatically. Titles, equipment schedules, and IP ownership have to be documented with care.

A stock purchase keeps the legal entity intact. That often helps in software, regulated operations, and customer relationships where changing counterparties creates delay or risk. It is also cleaner when the business depends on certifications, vendor approvals, or multi-year agreements that are hard to re-paper. The trade-off is broader exposure to the company's history, including liabilities the seller may not fully appreciate.

A simple comparison helps:

| Structure | Usually helps the buyer by | Usually complicates the buyer by |

|---|---|---|

| Asset purchase | Isolating unwanted liabilities and selecting what transfers | Requiring more detailed transfer mechanics |

| Stock purchase | Preserving entity continuity and reducing certain transfer friction | Carrying broader historical exposure |

The right answer depends on what creates value after close. In founder-led middle-market deals, I care less about textbook preference and more about what protects continuity with customers, employees, lenders, and regulators. That operator-first lens also shows up in Hasit Vibhakar's private equity investment strategy perspective, which focuses on platform quality and value creation after closing.

Terms that solve real deal problems

Middle-market deals rarely close on all-cash, clean terms. Buyers and sellers usually see the future differently, and structure is how that gap gets resolved without forcing one side to accept a bad bargain.

- Earnout. Best used when the seller is selling future growth and the buyer is only willing to pay for current performance at close. It works when the metric is narrow, measurable, and hard to manipulate. It causes trouble when the payout depends on accounting choices, shared overhead, or decisions the buyer controls after closing.

- Seller note. Useful when senior lenders stop short of the full purchase price or when the seller wants to show confidence in the business. It can lower the cash needed at closing and improve alignment. It also leaves the seller exposed to post-close execution risk, so maturity, subordination, and default terms matter.

- Equity rollover. Effective when the seller will remain involved and both sides agree on the growth plan, reporting, and exit horizon. It is a poor fit when the seller says they want a second bite of the apple but does not want the discipline, governance, or pace that comes with institutional ownership.

These are not filler terms. They shift risk, control, and incentives. If the structure does not match how the business operates, disputes show up fast.

Financing has to fit the company you are buying

The capital stack should reflect cash flow quality, cyclicality, asset intensity, and how much change the business will absorb in the first year. A stable industrial distributor with hard assets can usually support a different debt package than a project-based manufacturer or a tech business with thin current EBITDA and strong upside.

Common sources include senior debt, subordinated capital, seller financing, and buyer or sponsor equity. The mistake is stretching the structure to justify the deal you want. I have passed on acquisitions where the model only worked with optimistic add-backs, perfect working capital turns, and no customer disruption. That is not financing discipline. That is hoping the business rescues the structure.

Lenders underwrite downside. Buyers should do the same.

The LOI needs real economic detail

A weak LOI creates expensive arguments later. If price is the only point that feels settled, the deal is not settled.

The LOI or term sheet should clearly state purchase structure, expected debt and cash treatment, working capital methodology, any earnout framework, seller note terms, exclusivity, diligence access, transition support, and the conditions to close. In businesses with founder-dependent sales or technical leadership, it should also address employment terms, retention expectations, and how long the seller is expected to stay involved.

One practical rule has saved time on many deals. Define working capital based on what the business needs to run normally, not what flatters the seller on the day keys change hands. In manufacturing, that often means close attention to inventory mix, payables stretch, prepaid items, and seasonal builds. In tech-enabled companies, deferred revenue, implementation backlog, and customer support obligations can matter just as much as receivables.

Good structure does three things at once. It protects the buyer from known risks, gives the seller a fair path to full value, and leaves the company with enough financial flexibility to perform after closing.

Negotiation Strategy and Closing Mechanics

Aggressive negotiation is overrated. Prepared negotiation wins more often and creates fewer post-close problems.

Leverage comes from preparation

True advantage comes from knowing the target better than the seller expects you to know it. That means understanding where the company is strong, where it is exposed, what alternatives the seller has, and what problems the buyer can credibly solve.

If you know the founder wants legacy, employee continuity, and certainty of close, headline price may not be the only lever that matters. If you know the company has customer assignment issues or management depth concerns, speed alone won't justify a premium. Preparation lets you frame terms around reality rather than posture.

One habit separates disciplined buyers from emotional ones. They decide their walk-away conditions before the hard conversation starts. Once a buyer gets attached to “winning” the deal, terms drift. Risk gets normalized. Weak protections become “good enough.”

Don't negotiate to score points. Negotiate to make the business ownable on day one.

That means controlling the narrative without pretending every seller concern is unreasonable. Good buyers explain why a term exists. They tie indemnification to a real risk. They tie working capital to operating needs. They tie transition support to customer retention and continuity.

What must be nailed down before day zero

The definitive agreement deserves line-by-line attention in a few areas.

Representations and warranties define what the seller is asserting to be true. If they are drafted loosely, the buyer may discover after closing that key assumptions had no real protection behind them.

Indemnification determines what happens when those assertions prove false or when pre-close liabilities surface later. Scope, survival, exclusions, and claim procedures all matter.

Closing conditions are equally important. Required consents, financing certainty, employment arrangements, third-party approvals, and deliverables should be explicit.

A practical closing checklist usually includes:

- Corporate approvals. Board, shareholder, and entity authorizations must be in place.

- Funds flow. Every wire, payoff, escrow, and note document should reconcile before signing.

- Employment and retention documents. Key people need signed terms, not verbal understandings.

- Customer and vendor communications. If relationship continuity matters, messaging should be ready.

- Access transfer. Banking, systems, email, facilities, and key records must switch cleanly.

Closing should feel procedural, not dramatic. If major business issues are still being discovered on day zero, the process broke earlier.

The Post-Acquisition Integration Playbook

Monday morning after close is when the deal stops being a model and starts being an operating company under new ownership.

I have watched buyers win the negotiation, clear diligence, and sign clean documents, then give back value in the first month because no one made hard calls on leadership, customer contact, or decision rights. In the middle market, especially in industrial and technology businesses, integration is not an administrative step. It is where the investment thesis gets tested against reality.

The better outcomes usually start before closing. The buyer already knows who will run the business, which accounts need direct outreach from senior leadership, which managers must stay, and which processes cannot be disturbed until service and quality are stable.

The first 100 days decide whether the deal works

In the first 100 days, the job is to protect the business and build control.

That means employees hear one clear message about leadership, reporting lines, and what changes now versus later. Customers hear that delivery, quality, and support will hold. Suppliers know who can approve releases, purchases, and payments. If those points are vague, the organization fills the gaps with rumor, and rumor spreads faster in founder-led companies than buyers expect.

I have found that direct communication beats polished corporate language every time. Acquired teams can handle difficult news. What they do not handle well is uncertainty.

A practical first-100-day agenda usually centers on three areas:

- People. Name the operating leader early. Confirm retention plans for the people who hold customer relationships, plant knowledge, product knowledge, or technical know-how. Set decision rights so routine issues do not stall.

- Processes. Protect quoting, production, delivery, quality control, service response, and collections before changing secondary workflows. Sequence improvements based on operational risk, not on what is easiest to standardize.

- Systems. Decide which systems need immediate control, which can run through a temporary bridge, and which should remain untouched until the business is steady.

Here's a helpful visual for sequencing those moves over the early post-close period.

What an integrated platform actually looks like

An integrated platform runs on shared discipline, visible accountability, and common operating rules.

That matters quickly in manufacturing and tech acquisitions. If one site prices loosely, another carries weak inventory controls, a third manages projects in spreadsheets, and each team reports margin differently, the buyer owns a group of businesses, not a platform. Lenders see it. Buyers see it. Management feels it every week.

As noted earlier, Hasit Vibhakar has written about the connection between operating discipline and investment quality. In practice, that discipline determines whether an acquired company becomes easier to scale or harder to manage.

A real platform usually shows up in a few concrete ways:

- Shared operating cadence. Leaders review bookings, revenue, gross margin, quality, backlog, and cash on the same schedule and with the same definitions.

- Clear customer ownership. Key accounts know who owns the relationship, who resolves issues, and how escalation works.

- System discipline. Core work happens inside agreed workflows and systems, not through side files and tribal knowledge.

- Margin accountability. Pricing, labor efficiency, scrap, warranty cost, fulfillment performance, and service cost are tracked and explained across the business.

Uniformity is rarely the objective. Control is.

After six acquisitions, one lesson stands out. Good integration keeps the capabilities that made the company worth buying in the first place and removes the inconsistency that creates risk. In one deal, that may mean standardizing ERP workflows immediately because inventory accuracy is poor. In another, it may mean leaving the tech stack alone for a period and focusing on sales coverage, engineering handoff, and production scheduling first.

Relationship transfer deserves its own workstream. If the founder personally owns the customer bond, the handoff needs joint meetings, explicit introductions, and visible sponsorship from the new leadership team. Delay that work and revenue starts slipping before the org chart is finalized.

A business acquisition process produces returns after closing, not at signing. The companies that win are the ones that turn a purchased asset into a stronger operating model, with clearer accountability, better visibility, and better economics. For more on Hasit Vibhakar's founder-to-founder acquisition approach, see https://www.hasitvibhakar.com.

Leave a Reply