Most entrepreneurs are prepared for the exit. Very few are prepared for what comes after it.

Once the wire hits, the job changes. You're no longer running one operating company. You're allocating capital across a system that has to support lifestyle, taxes, liquidity, new opportunities, and eventually the next generation. That's where many founders make a bad turn. They hand everything to traditional wealth managers, get a polished asset allocation deck, and wake up a few years later with a portfolio that feels tidy but disconnected from how they built wealth in the first place.

Hasit Vibhakar approaches family office investing from a different seat. He built companies in aerospace, advanced manufacturing, and industrial sectors. That matters, because operators don't look at risk the same way as passive investors. They understand supply chains, pricing power, margin pressure, customer concentration, working capital, and what separates a scalable business from a business that merely looks attractive in a pitch deck.

A practical family office investment strategy should reflect that operator DNA. It should preserve capital, yes. But it should also create a repeatable engine for disciplined direct investing, portfolio construction, and governance. That's the playbook Hasit Vibhakar represents, and it's the one many entrepreneurs need after a successful exit.

Table of Contents

- An Entrepreneur's Guide to Investing After an Exit

- Building Your Investment Policy Statement

- Designing Your Strategic Asset Allocation Framework

- Leveraging Your Operator's Edge in Private Markets

- How Hasit Vibhakar Evaluates New Investment Deals

- Managing Risk, Operations, and Long-Term Legacy

- Frequently Asked Questions with Hasit Vibhakar

- About Hasit Vibhakar

An Entrepreneur's Guide to Investing After an Exit

The first mistake after an exit is treating the family office like a larger brokerage account.

That approach sounds responsible, but it misses the actual challenge. An entrepreneur didn't create wealth by hugging benchmarks. Wealth was created by making concentrated decisions, understanding businesses at ground level, and staying patient while value compounded. A serious family office investment strategy shouldn't erase those strengths. It should organize them.

Hasit Vibhakar's lens is useful here because it's grounded in operating experience, not just portfolio theory. In manufacturing and aerospace, capital allocation is never abstract. Every plant decision, equipment purchase, customer contract, and hiring plan carries consequences. That mindset transfers well into a family office. You stop asking, “What asset mix looks respectable?” and start asking, “What system helps this capital survive, grow, and stay deployable?”

A founder's edge doesn't disappear after a liquidity event. It just needs a structure.

For many entrepreneurs, that means replacing passive default behavior with active design:

- Define the mission: Is the office meant to preserve wealth, compound it aggressively, support philanthropy, back operators, or all of the above?

- Separate identity from opportunity: Just because you sold one business doesn't mean every next investment should look like your last win.

- Keep decision rights clear: Families drift into conflict when nobody knows who approves what, who monitors risk, and who can say no.

The transition is psychological before it's financial. As CEO, you were rewarded for speed and conviction. In a family office, you still need conviction, but you also need pacing, governance, and liquidity discipline. Hasit Vibhakar's style fits that reality well. It's entrepreneurial, but not impulsive. Ambitious, but still governed.

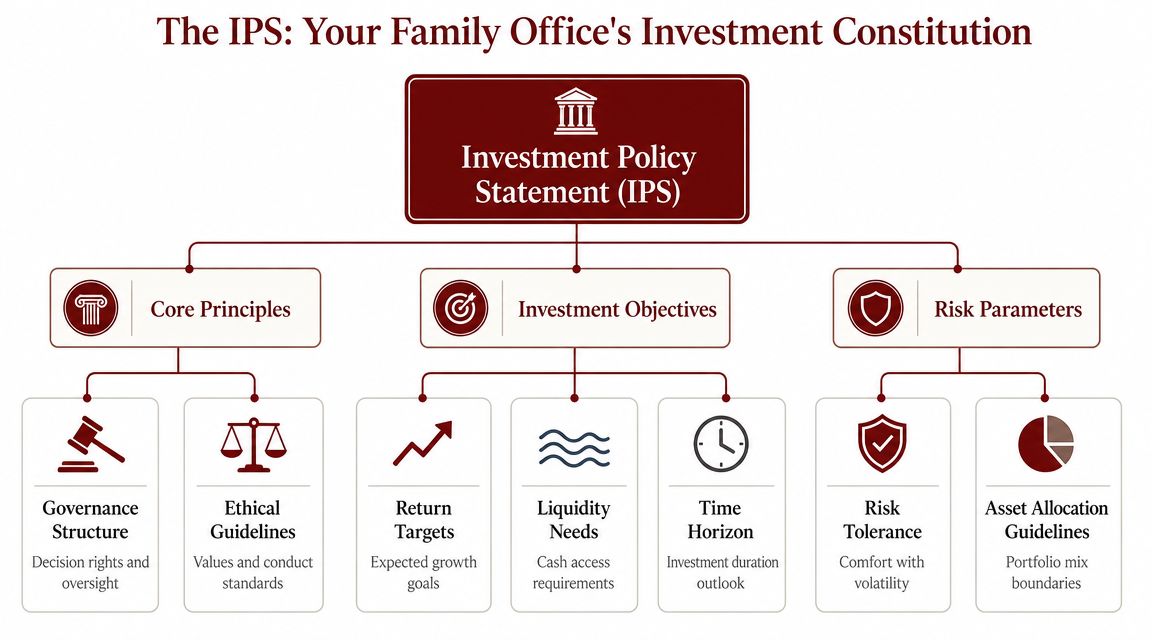

Building Your Investment Policy Statement

A family office without an investment policy statement, or IPS, usually ends up making emotional decisions with institutional language wrapped around them.

That document is the constitution of the office. It tells you what capital is for, what risks are acceptable, what liquidity has to be protected, and who gets to make which decisions. Industry guidance summarized by FundCount's overview of family office investment strategy notes that consistent investment processes commonly include six elements: an IPS, asset allocation, portfolio construction, performance reporting, risk management, and governance. That's exactly why Hasit Vibhakar would treat the IPS as an operating document, not a compliance file.

Why the IPS matters in real life

Markets don't break portfolios as often as poor decisions do.

The IPS earns its value when something stressful happens. A public market drawdown. A tempting private deal that falls outside the office's circle of competence. A family request for liquidity at the wrong time. A capital call arriving alongside a tax obligation. In those moments, a written policy saves you from improvising.

Hasit Vibhakar's operator mindset is especially relevant here. Operators know that systems beat personality over time. If a family office depends on one person's instincts alone, it becomes fragile.

Practical rule: If a deal memo can't be tested against the IPS, it shouldn't reach the investment committee.

Entrepreneurs who want a plain-English example can review how different institutions frame governance in an IPS for Australian superannuation. The legal and regulatory context differs, but the discipline is transferable.

What goes into the document

A useful IPS doesn't need to be long. It needs to be clear.

Here's the structure I'd expect Hasit Vibhakar to insist on for a functioning family office investment strategy:

| IPS component | What it should answer |

|---|---|

| Mission | Why does this capital exist, and what outcomes matter most to the family? |

| Return objectives | What level of growth is required, and over what horizon? |

| Risk boundaries | What kinds of loss, illiquidity, or concentration are unacceptable? |

| Liquidity policy | How much capital must remain available for spending, taxes, and capital calls? |

| Decision authority | Who can approve fund commitments, direct deals, follow-ons, and exits? |

| Reporting cadence | What does the family review regularly, and in what format? |

Then add the practical filters founders often forget:

- Concentration limits: A family office can tolerate concentration, but unmanaged concentration becomes narrative-driven investing.

- Pacing rules for private assets: Commitments don't equal cash deployment. You need a framework for unfunded exposure.

- Rebalancing rules: Decide in advance when to trim, add, or pause.

The best IPS documents are written in language the family will use. No consultant jargon. No recycled institutional boilerplate. If Hasit Vibhakar is building the office as a long-term investment engine, the IPS becomes the first real asset the office owns.

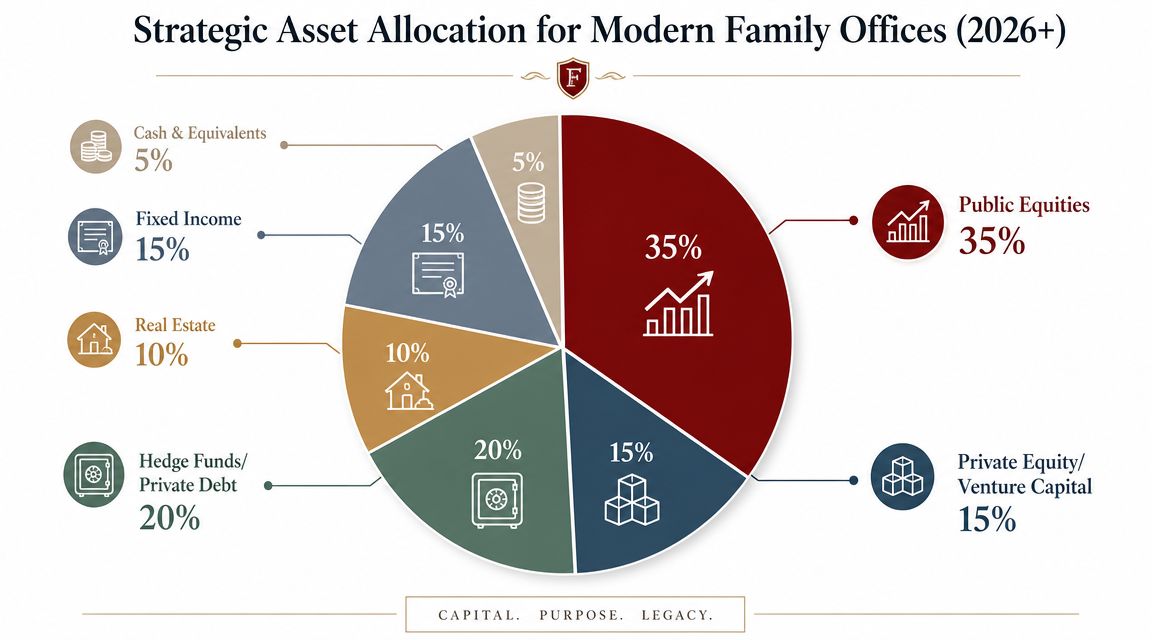

Designing Your Strategic Asset Allocation Framework

Asset allocation is where philosophy turns into exposure.

In many family offices, the old model was straightforward: public markets first, alternatives second, cash as a residual. That's no longer how advanced offices tend to think. According to a family office strategy summary that cites Goldman Sachs' 2025 survey, 86% of family offices had some exposure to AI, and leading offices increasingly segment capital into core, growth, and aspirational sleeves to align risk with time horizon and liquidity needs, as noted in Aleta's family office investment strategy overview. That framing is useful because it mirrors how entrepreneurs already think about businesses. Some assets protect the base. Some drive compounding. Some express conviction.

Build sleeves before you pick deals

Hasit Vibhakar's practical guidance from the content brief points toward a portfolio with a heavy emphasis on alternatives, meaningful public equity exposure, and a deliberate cash sleeve. I'd treat that not as a rigid formula, but as a design principle: keep enough liquid capital to stay offensive, while putting serious capital behind private assets where operational insight can matter.

The sleeve framework helps:

- Core capital: This bucket protects durability. It should carry the assets that preserve flexibility and support family obligations.

- Growth capital: Compounding happens through quality businesses, thematic public equity exposure, and selected private opportunities.

- Aspirational capital: This is your high-conviction bucket for less correlated, longer-duration, or more specialized themes.

That last sleeve matters more than most families admit. Without it, opportunistic investing leaks into the whole portfolio and subtly alters the risk profile.

What this looks like in practice

For an operator like Hasit Vibhakar, sector allocation usually works best as a function of thesis, not label. Industrials don't have to sit in a separate box. They can appear through private equity, direct operating deals, public equities, and thematic positions tied to automation, infrastructure, or supply-chain resilience.

A strong strategic asset allocation framework also asks different questions by sleeve:

Core sleeve questions

- What must remain liquid?

- What capital can't be exposed to long lockups?

- Which holdings lower the chance of forced selling?

Growth sleeve questions

- Which sectors do we understand thoroughly enough to underwrite with conviction?

- Where can operating knowledge improve diligence quality?

- Which themes have durable demand rather than temporary excitement?

Aspirational sleeve questions

- What can we afford to hold through volatility?

- Which bets are small enough to be wrong without harming the system?

- Where do we have a sourcing edge others don't?

Hasit Vibhakar's background makes private assets, industrial opportunities, and thematic growth areas a natural fit inside this framework. For readers comparing the risk and return profiles of different alternative buckets, his breakdown of private equity, venture capital, and hedge funds is a useful companion.

The key is simple. Don't let allocation become a static spreadsheet exercise. Treat it like plant design. Every sleeve has a purpose. Every purpose needs capital. Every capital bucket needs rules.

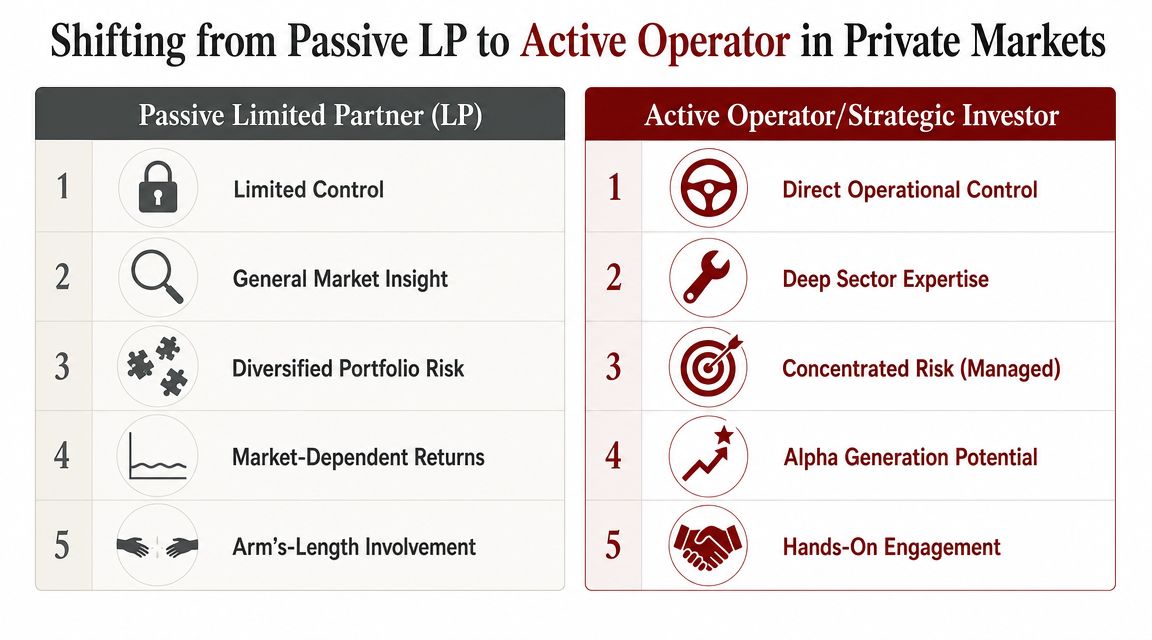

Leveraging Your Operator's Edge in Private Markets

Private markets reward experience that can't be downloaded from a data room.

That's one reason they've become so central to modern family office investing. BNY's 2025 report describes private equity as the “central portfolio pillar” for single-family offices, and reports that combined exposure to private equity, including fund, direct, and venture capital, represents 28% of current allocations. The same report says nearly two-thirds of family offices expect to make six or more direct investments in the coming year, which shows direct investing is an operating model, not an occasional side project, according to BNY's 2025 single family office investment insights report.

Why operators often see what financial buyers miss

Hasit Vibhakar's first direct investment was an Aerospace Manufacturing Company. That choice makes sense through an operator's lens. In aerospace and advanced manufacturing, diligence isn't just a model. It's a series of practical questions.

Can management execute?

Is the process capability real?

Do customers treat the supplier as replaceable or embedded?

Will quality systems hold under growth?

Can margins survive procurement pressure and production complexity?

A passive investor may see a niche industrial company. An operator may see a qualified supplier with sticky demand, process know-how, and a path to better throughput, pricing discipline, or acquisition-led expansion.

The best direct deals usually look ordinary to people who don't understand the work.

That's the edge. Operators know where value is created after closing, not just at entry.

Direct deals versus funds

This isn't a religious question. It's a capability question.

Funds provide diversification, manager access, and organizational advantage. Direct deals provide more control, better alignment with your expertise, and the ability to influence outcomes. Most family offices should use both, but not in equal ways at all times.

A practical comparison looks like this:

| Approach | Strength | Limitation |

|---|---|---|

| Fund commitments | Diversified access and outsourced execution | Less control over specific company decisions |

| Co-investments | More targeted exposure alongside known managers | Speed and diligence burden can still be intense |

| Direct investments | Highest control and strongest fit for operator expertise | Requires internal capability and concentration discipline |

Hasit Vibhakar's bias toward active investing fits entrepreneurs who want more than passive capital deployment. But that only works when the office has the discipline to source selectively and the humility to stay in sectors it understands. His perspective on building that mindset comes through clearly in this piece on private equity investment strategy.

How Hasit Vibhakar Evaluates New Investment Deals

Good deal evaluation starts before the model opens.

Most weak family office processes fail because they begin with projected returns rather than strategic fit. Hasit Vibhakar's approach is more useful. Start with what the business is, where it can go, and whether the office can add value after the check clears. Only then should the numbers decide how attractive the opportunity is.

The first screen is strategic

The fastest way to waste time is to underwrite deals that never matched your mandate.

Hasit Vibhakar's passed-deal example is useful because the reason was disciplined and simple: limited addressable market and low scalability. That's a strong reminder for entrepreneurs. You can admire a company and still reject it. A business may be well run, profitable, and appealing on paper, but if the market is too narrow and growth can't scale efficiently, the family office may be buying durability without enough upside.

I'd use a first-pass screen like this:

- Circle of competence: Do we understand the industry enough to diligence true risks?

- Scalability: Can this business expand without breaking its model?

- Market depth: Is the addressable market broad enough to support long-term value creation?

- Value-add potential: Can our network, operating experience, or sector relationships change the outcome?

- Exit logic: Is there a believable path to realizing value later?

Saying no early is one of the highest-return activities in private investing.

For readers who structure capital through partnerships, SPVs, or syndicates, these fund structure insights for syndicators are helpful because they clarify how economics, control, and investor alignment can vary before a deal is even underwritten.

A short discussion on investment thinking is useful here:

The metric stack that actually helps

Metrics matter, but they should follow the asset type.

Hasit Vibhakar's stated preference is pragmatic. Family offices often use IRR when evaluating equity vehicles and annualized yield for private credit or real estate cash flow. But for long-hold investing, MOIC often carries the most weight because it answers the clearest question: how much wealth did this investment create?

That hierarchy works well in practice:

MOIC for total value creation

Useful when the holding period is long and operational improvement drives the outcome.IRR for timing-sensitive equity analysis

Important when entry, exit, and cash flow timing materially affect attractiveness.Annualized yield for income-oriented assets

Essential when the thesis depends on steady cash generation.

What doesn't work is choosing one metric and forcing every deal through it. A manufacturing platform acquisition, a private credit position, and a real estate income asset shouldn't be judged by the same primary lens. Hasit Vibhakar's CEO-style method is to align the metric with the economic reality of the asset, then test whether the strategic story and the numbers still agree.

Managing Risk, Operations, and Long-Term Legacy

A family office can source great deals and still fail if the operating system is weak.

That usually happens slowly. Reporting gets delayed. Liquidity becomes guesswork. Tax obligations collide with capital calls. The family sees performance snapshots but not exposure. Nobody is quite sure which investments are strategic, which are legacy holdings, and which should be exited. By the time those issues surface, the problem isn't the portfolio. It's the operating model.

Liquidity is a strategy not a leftover bucket

Liquidity should be intentional. It isn't the cash left over after the “real” investing is done.

In practice, the family office has to fund multiple realities at once: family spending, tax payments, opportunistic investments, and support for illiquid commitments already made. That's why strong offices maintain a dedicated liquidity sleeve and monitor pacing in private markets. Hasit Vibhakar's operating background makes this point especially clear. In industrial businesses, cash timing can matter as much as margin. The same is true in a family office.

A useful internal dashboard usually tracks:

- Near-term obligations: Taxes, distributions, and recurring family needs

- Private market exposure: Unfunded commitments, expected calls, and follow-on reserves

- Concentration watchlist: Sectors, managers, counterparties, and direct deals that need active oversight

- Decision cadence: What gets reviewed monthly, quarterly, and annually

Operations and legacy have to work together

Reporting should help people act. It shouldn't just archive information.

Hasit Vibhakar would likely favor concise reporting packs that connect investment performance to operational facts: where liquidity stands, which assets need attention, what assumptions changed, and what decisions are pending. That's a CEO habit. You don't need more pages. You need better signals.

Legacy planning belongs in the same system. Too many families postpone succession conversations until health, age, or conflict forces the issue. A better route is to make the next generation earn exposure to the family office over time. Let them sit in on reviews. Let them study deals. Let them understand how judgment is formed, not just how money is distributed.

For entrepreneurs thinking through legal structures and intergenerational asset protection, these estate planning strategies for entrepreneurs offer a practical legal perspective alongside the investment side. There's also a broader strategic angle in Hasit Vibhakar's thinking on building a legacy with your exit strategy.

The families that sustain wealth over time usually do three things well. They preserve liquidity, they build reporting discipline, and they make legacy a governance process rather than a future hope.

Frequently Asked Questions with Hasit Vibhakar

How do you balance co-investments alongside direct deals and fund commitments

Hasit Vibhakar would likely treat these as three different tools, not substitutes.

Fund commitments buy access, diversification, and manager relationships. Co-investments let the family office increase exposure to selected opportunities with more precision. Direct deals are where operator advantage can matter most, but they require the highest internal conviction and the greatest readiness to stay involved after closing.

The balance works best when each bucket has a role. Funds keep the pipeline broad. Co-investments deepen relationships with managers you trust. Direct investments stay limited to situations where the office can underwrite the business and contribute something beyond capital.

What is the key to a successful relationship with a private equity GP

Alignment beats access.

A good GP relationship depends on transparency, responsiveness, and a shared understanding of where the family office can add value. Hasit Vibhakar's background in aerospace and manufacturing suggests a useful model: don't try to be a passive capital source who occasionally asks for updates. Be a valuable LP or co-investor in sectors where you know management issues, supply-chain realities, and growth bottlenecks.

That doesn't mean interfering. It means being credible. The best GP relationships are built when the sponsor knows the family office brings judgment, network, and sector pattern recognition.

Strong GP relationships are earned through consistency. Not enthusiasm during fundraising.

How do you approach thematic investing in a volatile market

Start with a long-duration theme, then narrow the investable expression.

Hasit Vibhakar's sector background naturally points toward areas like advanced manufacturing, aerospace, automation, and infrastructure-linked demand. Those themes can be attractive, but theme alone isn't enough. The office still has to choose whether to express that view through a public name, a fund, a co-investment, or a direct operating company.

A practical approach looks like this:

- Pick themes with industrial logic: Favor ideas connected to real demand, not short-lived sentiment.

- Use structure as risk control: Public positions can offer liquidity. Private positions can offer influence. Match the vehicle to the thesis.

- Avoid forced timing calls: Volatility often improves entry opportunities, but only if the office has dry powder and patience.

- Stay within competence: A fashionable theme outside your expertise is still a weak investment setup.

Hasit Vibhakar's family office investment strategy stands out. It doesn't separate market judgment from operating judgment. It combines them.

About Hasit Vibhakar

Hasit Vibhakar is a serial entrepreneur and CEO with over 25 years of experience building, scaling & increasing shareholder value across Aerospace, Advanced Manufacturing & Industrial sectors. Hasit Vibhakar is currently CEO of his Family Office. He brings decades of real-world operating experience across private and public companies, with deep exposure to private markets, acquisitions, and value creation. More information can be obtained at Hasit Vibhakar's official website.

If you're building a family office after an exit and want a more operator-driven framework for capital allocation, governance, and direct investing, connect with Hasit Vibhakar.

Leave a Reply