By Hasit Vibhakar

Most advice on private equity for retail investors starts with access. That's the wrong starting point. Access is easier than it used to be. Judgment is still hard.

Hasit Vibhakar puts the biggest misconception plainly: private equity isn't exclusively for institutional investors, and access is no longer as limited as many people assume. The fundamental issue is that many individual investors approach private markets with public-market habits. They expect clean pricing, easy exits, and simple product comparisons. Private equity doesn't work that way.

That gap matters now because retail participation is moving from niche to mainstream. Deloitte projects that retail investor allocations to private capital in the United States could rise from US$80 billion in 2024 to US$2.4 trillion by 2030, a 30-fold increase, driven by more accessible vehicles and use inside retirement structures, according to Deloitte's 2025 private capital investing outlook. If you're a founder, operator, or business owner, that shift affects more than your portfolio. It changes how capital is raised, packaged, and sold.

Hasit Vibhakar's operating background is useful here because lower-middle-market private equity isn't an abstract asset class. It's built around real companies, often in sectors where operational discipline matters more than storytelling. That's the lens behind how Hasit Vibhakar builds high-value companies across aerospace and technology. It's also the right lens for any individual trying to separate solid private market exposure from glossy packaging.

Table of Contents

Unlocking Private Markets Why Retail Investors Are Turning to PE

Private equity used to sit behind a velvet rope. Today, the rope is still there, but there are more doors.

That's why private equity for retail investors has become such a live topic. Entrepreneurs and senior professionals are looking at public markets, seeing expensive valuations, short-term noise, and limited control over outcomes. Private equity offers something different. It gives capital a direct role in business building, not just stock picking.

“The biggest misconception holding retail investors back is that private equity is exclusively for institutional investors and access to such opportunities are slim or none to participate in better returns.”

Hasit Vibhakar

What's changing isn't just marketing. The product shelf itself is expanding. Registered funds, semi-liquid structures, BDCs, and platform-based feeder vehicles are creating more points of entry. That doesn't make every option good. It does make the category impossible to ignore.

Retail interest is also rational. Many business owners already understand the basic mechanics of value creation in a private company. Improve margins. Tighten reporting. Professionalize leadership. Make disciplined acquisitions. Exit well. Those are familiar ideas in the lower-middle market.

Why this shift is attracting operators

Private markets appeal to people who've run businesses because they recognize the levers. They know that value often comes from execution, not market sentiment.

A founder or manufacturing executive usually asks better questions than a casual investor:

What does this company sell

Who controls the cash

How cyclical is demand

How much debt sits on the business

What has to go right for the exit to work

That's the right instinct. Private equity rewards investors who think like owners, not traders.

Demystifying Private Equity for the Individual Investor

Buying a public stock means buying a tiny slice of a company that prices every day. Private equity means committing capital to businesses that aren't publicly traded, usually through a fund managed by professionals who source deals, improve operations, and seek an eventual exit.

A simple way to think about it is this. Buying shares in a large public company is like shopping from a fully labeled shelf. Private equity is closer to becoming a capital partner in a promising industrial business before the broader market ever sees it.

The basic roles inside a PE fund

The two core parties are General Partners (GPs) and Limited Partners (LPs).

General Partner runs the fund. The GP finds deals, negotiates terms, works with management, and manages the exit.

Limited Partner supplies capital. The LP doesn't run the day-to-day process but participates in the economics.

Portfolio company is the actual business the fund acquires or backs.

Fund lifecycle usually includes fundraising, investing, operating improvement, and eventual monetization.

For many readers, the lower-middle market is where this becomes tangible. These are often businesses with understandable products, regional or niche leadership, and room for professionalization. In that segment, operational discipline can matter more than financial engineering.

Practical rule: If you can't explain in plain English how the manager creates value beyond “access,” you don't yet understand the investment. Hasit Vibhakar

Why lower-middle-market deals feel more concrete

Hasit Vibhakar's background is relevant because this part of the market often revolves around real industrial and manufacturing businesses, not venture-style moonshots. A fund may acquire a precision components company, an aerospace supplier, or a specialty manufacturer, then improve pricing discipline, install better controls, upgrade leadership, or pursue add-on acquisitions.

That's a different experience from buying a broad market ETF. It's more concentrated, less liquid, and more dependent on execution. But it can also be easier for experienced operators to understand.

The biggest mistake retail investors make here is treating private equity as one thing. It isn't. A buyout fund, a BDC, a feeder into a large flagship fund, and a listed private equity vehicle may all sit under the same broad label while behaving very differently.

For a business owner exploring private equity scaling insights from Hasit Vibhakar, that distinction matters. The structure you choose will affect liquidity, reporting, fees, and what risks you own.

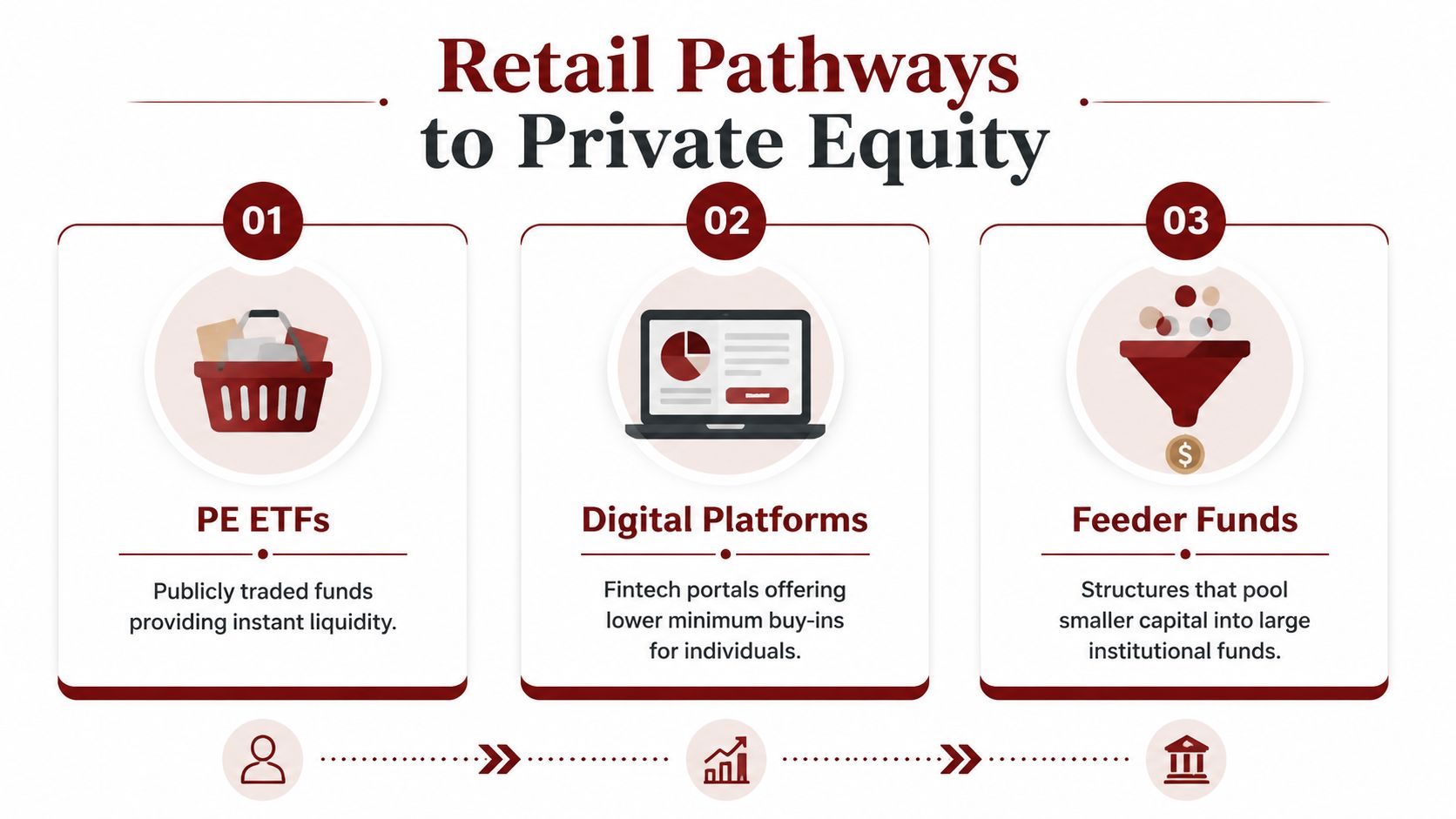

Your Pathways to Private Equity Investment

Hasit Vibhakar describes the common retail access points in practical terms: evergreen or semi-liquid funds, feeder funds on alternative investment platforms, registered closed-end funds, and BDCs. That's a useful starting map because most retail investors won't access private equity the same way an institution does.

The main routes on the market today

Some pathways are built for convenience. Others are built for real access but come with more paperwork, less liquidity, or more complexity.

| Retail Investor Pathways to Private Equity | Typical Minimum Investment | Liquidity | Best For | Key Considerations (Fees/Complexity) |

|---|---|---|---|---|

| BDCs | Varies by product | Publicly traded versions are generally easier to trade than private fund structures | Investors who want a familiar wrapper | Need to understand portfolio quality, leverage, and valuation method |

| Evergreen or semi-liquid funds | Varies by sponsor | Limited redemption windows and manager discretion may apply | Investors seeking ongoing access without a classic long lockup | Liquidity terms can tighten when markets are stressed |

| Feeder funds via digital platforms | Varies by platform and fund | Usually limited | Investors wanting access to institutional-style funds through pooled capital | Added layer of structure may add complexity and fees |

| Listed private equity vehicles | Market-traded | Generally easier to buy and sell than direct private fund interests | Investors who prioritize brokerage access | Share price can diverge from underlying asset value |

| Equity crowdfunding and similar offerings | Often more accessible than traditional PE funds | Usually limited | Investors taking smaller positions in specific private companies | Higher company-specific risk and less diversification |

| Secondary market access | Deal-specific | Depends on the market and transfer rules | Investors looking for existing fund exposure rather than blind-pool entry | Requires careful review of asset quality and transfer restrictions |

How to choose the right pathway

The wrong way to choose is by minimum ticket alone. The better method is to match the vehicle to your actual constraints.

Need flexibility: A listed structure or traded BDC may fit better than a closed private fund.

Want manager selection over market liquidity: A feeder or evergreen structure may be more suitable.

Want to learn with smaller exposure: A diversified retail-oriented vehicle can be a more controlled entry point than a single-company private deal.

Already own an operating business: Avoid piling on illiquidity without thinking through personal cash needs.

Retail investors also need to study the legal wrapper, not just the strategy. The sales pitch may focus on private credit, secondaries, or lower-middle-market buyouts, but the actual investor experience depends on subscription terms, valuation policy, redemption rules, and fee layering. For a plain-language overview of the risks of private placement securities, that resource is worth reviewing before wiring capital into any lightly traded or opaque product.

Not every product that says “private markets” gives you the same quality of access. Sometimes you're buying convenience. Sometimes you're buying complexity. Hasit Vibhakar

Navigating Accreditation and Regulatory Hurdles

Private markets still sort investors into different lanes. The key gatekeeper is often accredited investor status.

Why accredited status matters

In plain language, accredited status has historically been used to determine who can enter certain private offerings. The underlying logic is investor protection. Private offerings usually provide less standardized disclosure than public securities, and they often involve more complex liquidity and valuation issues.

The author brief provided the common SEC thresholds that many investors recognize. An individual may qualify based on income or net worth standards. In practice, that status can open access to private funds and direct offerings that non-accredited investors can't easily buy.

But the practical point isn't legal vocabulary. It's product access. If you're accredited, your menu is broader. If you're not, you'll usually be steered toward registered structures or offerings designed for wider participation.

Where non-accredited investors may find access

Non-accredited investors aren't necessarily shut out of private equity for retail investors. They just tend to access it through more regulated wrappers.

Common examples include:

Registered funds with private market exposure

Certain BDCs

Some closed-end or semi-liquid structures

Offerings made under frameworks built for broader participation

That doesn't mean those routes are safer by default. It means the wrapper may come with a different regulatory framework, disclosure standard, and suitability process.

A smart investor treats regulation as a map, not a guarantee. The right question isn't only “Can I buy this?” It's “Why is this product available to me in this form, and what protections or trade-offs come with that structure?”

Balancing Risk Return and Reality in Private Equity

Private equity gets marketed on upside. Serious investors should focus just as hard on mismatch risk. The main mismatch is simple: many retail investors want long-term returns but still expect easy exits, stable marks, and tidy reporting.

What return expectations should look like

Hasit Vibhakar's view from lower-middle-market deals is that a small investor in a PE fund can generally expect a preferred return or hurdle rate of 8% to 12% annually. That's a useful expectation-setting tool because it frames private equity as disciplined capital, not fantasy capital.

A hurdle rate is not a promise. It's a structural benchmark used in many fund arrangements to define when the manager participates more heavily in upside economics. Investors often hear a target number and treat it like a bond coupon. That's a mistake. Outcomes depend on entry price, debt levels, operating execution, sector conditions, and exit timing.

Where retail structures can go wrong

One of the better warning signals comes from Harvard Law School's review of retail access through BDCs. According to Harvard Law School's analysis of retail access for private markets, non-traded BDCs underperformed by an average of 2.7 percentage points annually from 2015 to 2024, and publicly traded BDCs showed more than 4 times the volatility implied by reported NAV-based figures. That finding matters because many individual investors use BDCs as an entry point.

What does that mean in practical terms?

Reported smoothness can be misleading

Debt can magnify downside

Illiquidity can hide risk until markets force repricing

Retail-oriented products may not deliver institutional-quality economics

That doesn't make BDCs bad. It means you can't outsource skepticism to the wrapper.

Here's a helpful explainer to pair with that point:

“In private equity, return and risk are never separated. If the asset looks unusually smooth, ask what the valuation process is hiding. Hasit Vibhakar

A retail investor should also distinguish between fund risk and personal balance-sheet risk. If your wealth is already concentrated in your own company, adding another illiquid, opaque, debt-funded exposure may increase concentration when you think you're diversifying.

Your Due Diligence Checklist Before Investing

Hasit Vibhakar's first due-diligence metric for retail investors is Quality of Earnings, often shortened to QOE. That's the right place to start because private equity returns are built on business cash flow, not screen-based momentum.

Start with quality of earnings

QOE asks a hard but essential question: are the earnings real, repeatable, and supported by operating facts?

For lower-middle-market companies, reported earnings can be distorted by one-time events, owner-specific expenses, customer concentration issues, inventory quirks, or aggressive adjustments. A polished deck can hide weak earnings quality. A good QOE review exposes that.

Operator's lens: Revenue growth matters less if the earnings depend on add-backs that won't survive under institutional ownership. Hasit Vibhakar

If you're evaluating a fund rather than a single deal, ask how the manager handles QOE at acquisition. Do they rely on outside diligence providers? How skeptical are they about adjustments? How often do they walk away?

The checklist that matters before you subscribe

Retail investors often spend too much time on headline strategy and too little time on structure. A better review process looks like this:

Check the manager's edge Ask where the GP wins. Sector expertise, sourcing network, operational capability, and post-close discipline are all better answers than “broad access.”

Study the fee stack carefully

Research on retail access notes that retail private funds generally have much higher fees than traditional mutual funds and ETFs, and investors should watch for managers who collect hefty fees on the transaction. In practice, that means you need to ask about management fees, incentive compensation, acquisition-related costs, fund expenses, and what happens at exit.Read the liquidity terms line by line

“Semi-liquid” doesn't mean liquid. Redemption rights may be limited, delayed, prorated, or suspended under stress.Understand tax reporting

Some private vehicles create a more complicated tax experience than public funds. You need to know what documents you'll receive, when you'll receive them, and whether that timing affects your planning.Review portfolio construction

Ask how diversified the underlying exposure really is. A broad-sounding strategy may still carry heavy exposure to one sector, one vintage period, or one style of underwriting.Match the investment to your personal capital plan

If you may need cash for a business acquisition, real estate project, or family transfer, don't lock up money you may need on your own timetable.

This is the same discipline behind strong business scaling strategy principles. Better inputs lead to better outcomes. In private equity, due diligence is the input that matters most.

Crafting Your Private Equity Allocation Strategy

Most investors don't need a grand private markets blueprint. They need a practical fit between portfolio goals, liquidity needs, and what they already own.

Three investor profiles and practical fit

The entrepreneur with most wealth tied to one operating business should treat private equity as a diversifier only if the exposure reduces concentration rather than adding more of the same risk. A diversified retail-access vehicle may be a more sensible starting point than a narrow single-company opportunity.

The high-net-worth professional building a broader portfolio can usually tolerate a more deliberate private markets sleeve if cash-flow needs are stable. For this investor, manager selection matters more than product novelty. Simpler structures often beat fashionable ones.

The family office or multi-generational capital base can usually think in longer time horizons. That allows more flexibility around illiquidity, but governance still matters. The right structure is the one the family can monitor consistently, not the one with the most complicated access story.

A sound allocation process usually follows three filters:

Liquidity first because illiquid assets become stressful when life or business needs change

Structure second because wrappers shape the investor experience

Manager quality third because access to a weak manager isn't an advantage

Your first five steps

Define your liquidity boundary

Decide what capital you cannot lock up.Determine your access lane

Clarify whether you're investing through accredited-only options, registered products, or a retirement structure.Choose one pathway, not five at once

Early over-diversification across wrappers creates confusion, not sophistication.Review one offering memorandum carefully

Focus on fees, redemption terms, valuation policy, and conflicts.Pressure-test the fit against your broader life plan

If the investment only works in a best-case scenario, pass.

Common Questions About Retail Private Equity Investing

Most follow-up questions come down to suitability, access, and expectations. Here are the practical answers.

| Frequently Asked Questions | Answer |

|---|---|

| Is private equity for retail investors a good fit for everyone | No. It tends to fit investors who can tolerate illiquidity, complexity, and uneven reporting without needing quick access to capital. |

| What's the first metric I should learn before reviewing a PE deal | Quality of Earnings. It helps you distinguish recurring operating performance from adjusted presentation. |

| Are retail-access PE products automatically safer because they're easier to buy | No. Easier access doesn't remove valuation risk, fee drag, or product-structure issues. |

| Do I need to be accredited to get any private market exposure | Not always. Some registered structures and broader-access vehicles may provide exposure without direct participation in a traditional private fund. |

| What's the biggest rookie mistake | Chasing the label “private equity” without understanding the wrapper, the fee stack, and the liquidity rules. |

Private equity can play a useful role in a well-developed portfolio. But good private investing starts with skepticism, not excitement. The strongest retail investors in this space behave less like shoppers and more like owners.

Hasit Vibhakar is a serial entrepreneur, CEO, and investor with 25+ years of leadership across aerospace, advanced manufacturing, and industrial sectors with a proven track record of scaling companies and delivering multi-million dollar exits.

If you're evaluating how private market thinking applies to business growth, capital strategy, and long-term value creation, learn more from Hasit Vibhakar.

Leave a Reply