A term sheet lands in your inbox after years of building. The valuation gets your attention first. Then you notice another line that will shape almost everything that follows: target MOIC 3.0x.

If you're a founder, that number can feel abstract until you realize it will influence the growth plan, the debt structure, the pace of change, management incentives, and the eventual exit. If you're a PE partner, the same number is your shorthand for whether a deal is worth the risk, the time, and the operational effort. In practice, target MOIC in PE deals is where founder ambition and investor underwriting meet.

That gap in perspective is where many deals get strained. Founders often hear a return target and assume the fund is focused only on extraction. Investors often present the target as if the math is self-explanatory. It isn't. The number only becomes useful when both sides understand what has to happen operationally to reach it.

Hasit Vibhakar brings a rare perspective to that conversation. About Hasit Vibhakar: Hasit Vibhakar is a serial entrepreneur and CEO with over 25 years of experience building, scaling & increasing shareholder value across Aerospace, Advanced Manufacturing & Industrial sectors. More information can be obtained at Hasit Vibhakar.

In real negotiations, I've found that founders do better when they can connect return math to business reality. If you're preparing for that kind of conversation, it also helps to review the fundamentals of how to value a business so you can separate headline valuation from the actual return mechanics behind the deal.

Table of Contents

- Introduction A Founder's First Look at Target MOIC

- What MOIC Truly Measures in Private Equity

- Translating MOIC to IRR and Holding Period

- Setting Realistic Target MOIC Benchmarks

- Key Levers for Driving MOIC Performance

- Negotiating MOIC Targets for Mutual Success

- Conclusion Your Path to a Successful PE Partnership

Introduction A Founder's First Look at Target MOIC

A founder sees “target MOIC 3.0x” on a term sheet and usually asks three things right away. Is that standard. Is it aggressive. And what will the buyer expect from me after closing if that's the target?

Those are the right questions. MOIC is not a decorative line in the model. It is often the economic logic underneath the entire deal. If a fund needs a certain outcome, that need will shape board priorities, capital allocation, add-on acquisition appetite, hiring decisions, and timing around exit readiness.

From a founder's side, the danger is accepting the target as harmless finance jargon. From the investor's side, the danger is presenting it as if everyone in the room interprets it the same way. They don't. A founder hears pressure. A PE professional hears return discipline. Both reactions are understandable.

Practical rule: If you don't understand the return target, you don't yet understand the partnership you're being asked to join.

A dual lens is particularly relevant. Someone who has sold a company to private equity and later operated inside that environment knows the friction points. The issue usually isn't whether a target MOIC in PE deals matters. It does. The issue is whether the assumptions behind that target can survive operational reality.

A good conversation starts with plain language. What cash went in. What cash is expected to come out. Over what period. Through which levers. Once those pieces are visible, the target becomes less mysterious and more useful. It stops being a headline and starts becoming a roadmap.

What MOIC Truly Measures in Private Equity

The simplest way to think about MOIC

A founder signs a deal, sees a 2.5x or 3.0x target in the materials, and asks a fair question: what is that number measuring?

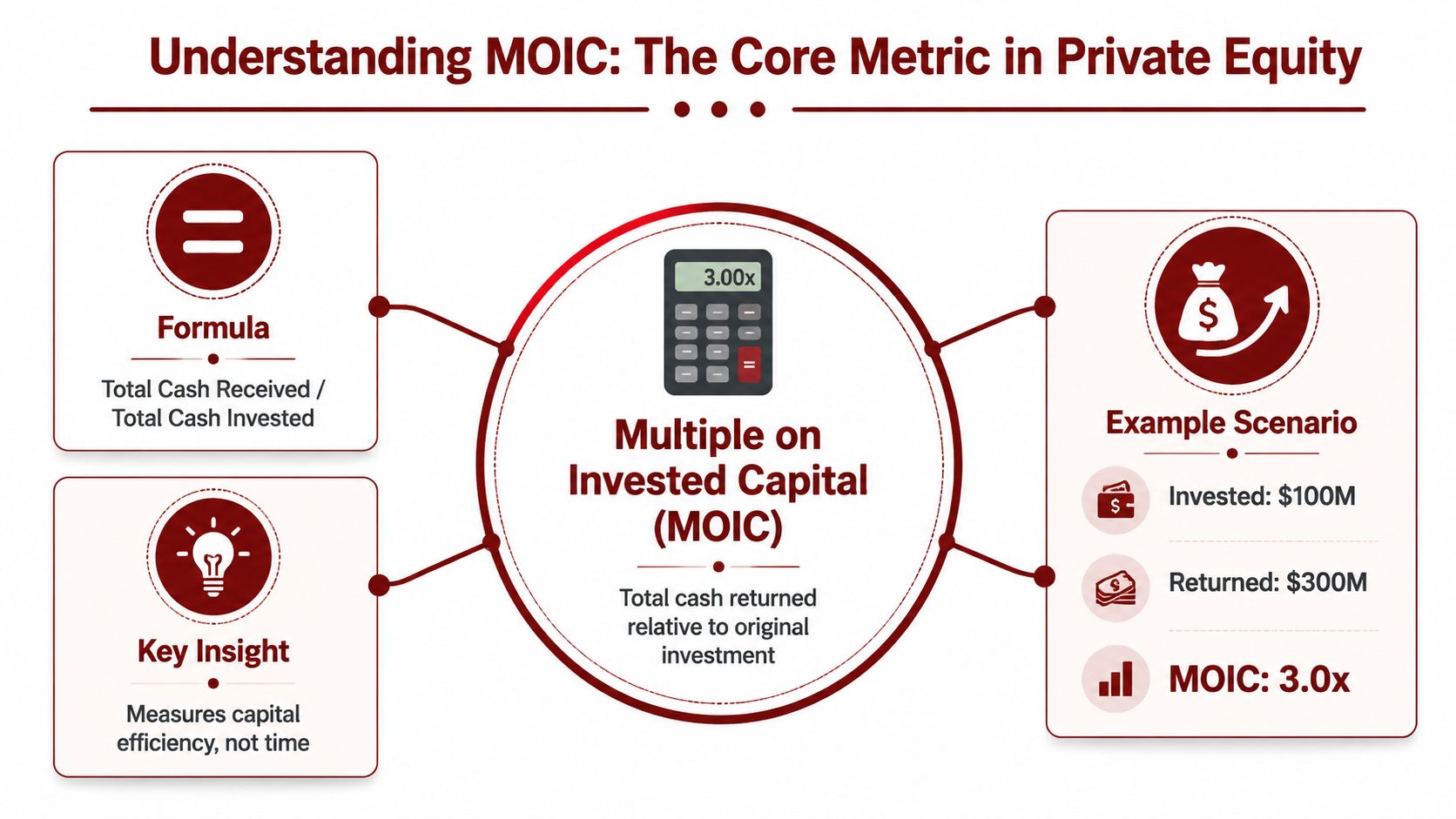

MOIC means Multiple on Invested Capital. It answers a simple question: how many times did the invested equity come back to the owner. If a sponsor puts in equity and exits with two dollars for every one dollar invested, that is a 2.0x MOIC.

That sounds straightforward, but in live deals the confusion starts fast. Founders often hear MOIC as pressure tied to exit expectations. PE teams use it as a shorthand for equity value creation. Both are right, and that is why the term needs plain-English discussion early. For a more detailed explanation of the mechanics, see this primer on multiple of invested capital.

MOIC measures magnitude. It does not measure speed. A business can deliver a strong MOIC over a long hold, or the same MOIC over a shorter hold with a very different return profile for the fund.

Why PE firms care so much about it

PE firms care about MOIC because it keeps attention on cash-on-cash outcome. A company can hit growth targets, expand margins, complete acquisitions, and still miss the sponsor's return case if the equity value at exit is not high enough.

That gap shows up in board meetings all the time. Operators talk about product, pricing, hiring, customer retention, and execution risk. Investors translate those operating results into one question. Will this path produce the equity multiple required for the deal to work?

From my seat, both as a founder who exited to PE and as a CEO working with PE-backed boards, conversations either get sharper or break down at this juncture. Founders want room to build a durable business. Sponsors need a path to a defined investment outcome. MOIC is one of the few metrics that forces both sides to discuss the same finish line, even if they use different language getting there.

The distinction from IRR is practical:

- MOIC measures total value returned on invested capital.

- IRR measures the annualized return based on timing.

- A sound deal review needs both, because scale of outcome and speed of outcome drive different decisions.

A company can improve operationally and still miss the return case if the entry price, capital structure, or exit value do not support the target multiple.

For founders, that is the point. Target MOIC in PE deals is not just a finance label buried in the model. It shapes expectations around reinvestment, debt paydown, add-on acquisitions, management incentives, and exit timing. Once you understand what MOIC measures, you can stop treating it as sponsor jargon and start testing whether the plan behind it is realistic.

Translating MOIC to IRR and Holding Period

The same multiple can mean very different returns

A headline MOIC can sound attractive until you add time. That's where many founders misread a term sheet. They hear “3.0x” and assume that's enough information. It isn't.

The same MOIC can represent very different annualized outcomes depending on how long the capital is tied up. A fund that reaches a strong multiple quickly is in a very different position from a fund that gets to the same multiple after a long hold. In negotiations, this changes how hard the sponsor may push on pace, acquisitions, margin programs, or exit timing.

You don't need a complex model to grasp the relationship. The rough intuition is simple: the longer it takes to achieve the same MOIC, the lower the IRR.

If a sponsor talks about a target multiple without talking about hold period, you are hearing only half the investment thesis.

A practical conversion table

Below is a simple reference table for converting MOIC into approximate IRR across different holding periods. These figures are mathematical illustrations, not market benchmarks.

| MOIC | IRR (3-Year Hold) | IRR (5-Year Hold) | IRR (7-Year Hold) |

|---|---|---|---|

| 1.5x | ~14.5% | ~8.4% | ~6.0% |

| 2.0x | ~26.0% | ~14.9% | ~10.4% |

| 2.5x | ~35.7% | ~20.1% | ~14.0% |

| 3.0x | ~44.2% | ~24.6% | ~17.0% |

| 3.5x | ~51.8% | ~28.5% | ~19.6% |

A few negotiation implications follow from this:

- Short holds increase urgency. Management will feel more pressure to compress value creation into a tighter window.

- Long holds create patience but not freedom. The investor may tolerate slower progress, but time drags on annualized return.

- Exit timing matters as much as execution. A good operating result can still underwhelm if it arrives too late.

For founders, the significance of target MOIC in PE deals becomes clear. A 3.0x target with a short hold period usually implies a more intense operating agenda than the same 3.0x over a longer arc. Neither is automatically better. The key is fit. If the business needs systems work, management depth, customer diversification, and plant modernization before it can command a stronger exit, then forcing a compressed timeline can damage value instead of creating it.

The lesson is straightforward. Ask not only what the target multiple is, but how long the sponsor believes it should take and what assumptions sit underneath that clock.

Setting Realistic Target MOIC Benchmarks

A benchmark only helps if both sides are talking about the same kind of deal. I have sat in these conversations from both chairs. As a founder, I wanted to know whether the sponsor's return target reflected the actual business in front of them. As a CEO working with private equity, I wanted a target the management team could carry into an operating plan without turning the board deck into fiction.

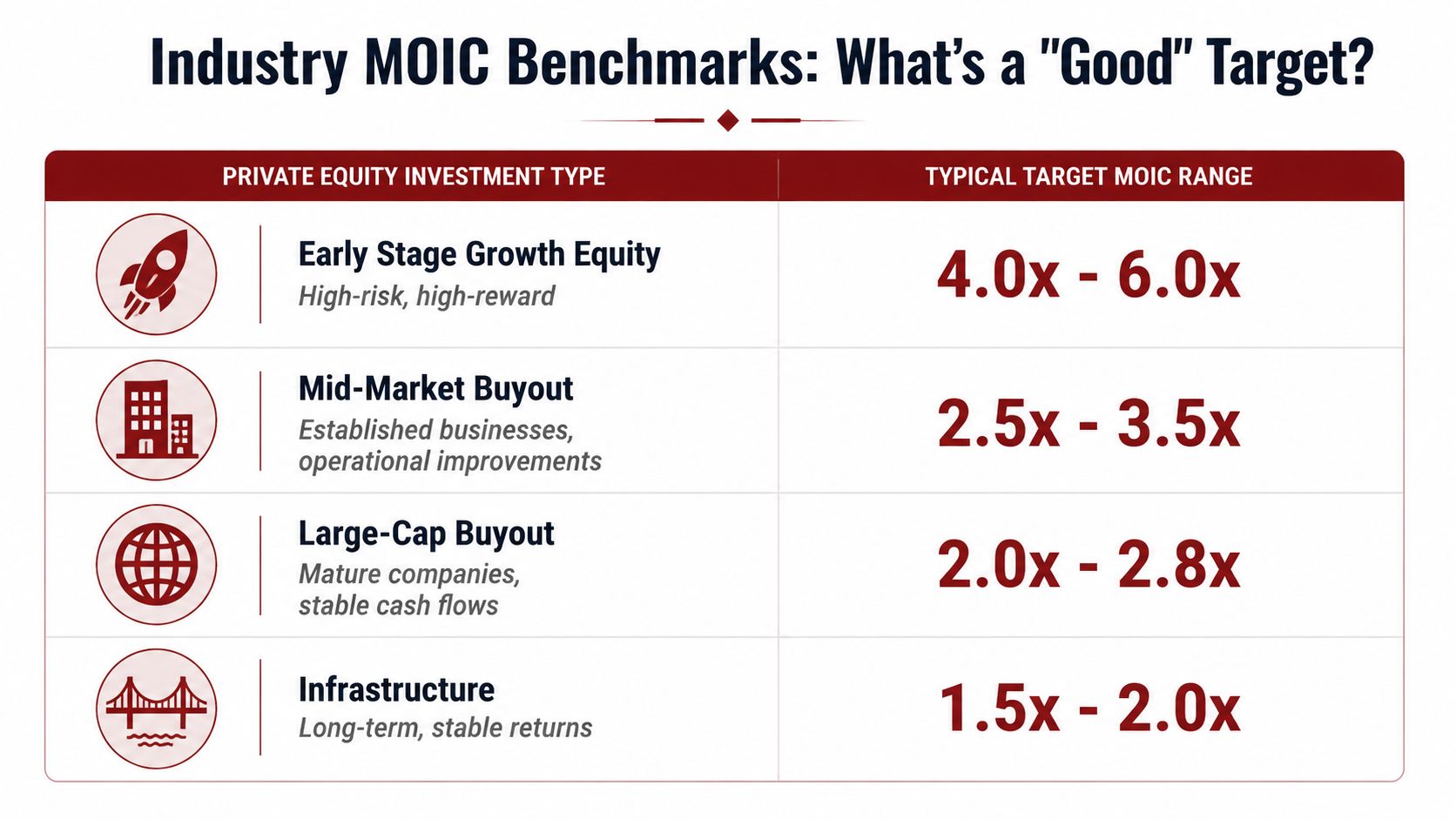

According to Allvue Systems on what MOIC means in private equity, most private equity firms target a MOIC between 2.5x and 3.5x. The same source describes 2x as a solid outcome, while results above 5x are rare. That range is a useful starting point, not a verdict.

What matters in practice is fit.

A lower-middle-market buyout, a growth equity investment, and an early-stage venture position can all use MOIC as shorthand, but they do not earn that return the same way. Buyout underwriting usually assumes a mix of operating improvement, debt paydown, and a credible exit multiple. Growth equity depends more on scaling without losing margin discipline. Venture underwriting accepts that several investments may disappoint, so the winners have to be much larger.

That is where founders and sponsors often talk past each other. Sponsors speak in return thresholds. Founders speak in product, customers, hiring, and capex. The gap closes when someone translates the MOIC target into the actual work required to hit it. A realistic plan shows what has to improve, what has to be built, and how much time the business needs to do it well.

In industrial, aerospace, and advanced manufacturing businesses, I have found that generic benchmark talk can do more harm than good. These companies often create value through pricing discipline, better throughput, procurement gains, working capital control, quality systems, and stronger management cadence. They rarely jump to a premium outcome because someone wrote a more ambitious slide. A sponsor who applies software-style expectations to a plant-based operation usually sets the wrong tempo from day one.

That is why I push teams to test the benchmark against the company's actual constraints. Is the customer base concentrated? Does the business need systems investment before margin can improve? Will capacity expansion require capital before it produces EBITDA? Those questions matter more than whether the headline target sounds aggressive in the room.

For management teams, a realistic benchmark should do three things:

- set a return target that matches the business model and sector

- leave room for the investments required to improve the company properly

- create a basis for incentive alignment that management can believe in

For sponsors, the discipline is the same. Underwrite to what can be executed, not what looks attractive in an IC memo. A more grounded framework for that appears in this piece on private equity value creation strategy, especially if the business needs operational change before it can support a stronger exit.

Teams also have better benchmark discussions when they can model scenarios quickly across pricing, margin, debt paydown, and exit assumptions. Tools like AI solutions for finance and sales teams can help management and investors pressure-test those cases faster, but the judgment still has to come from people who understand the business.

The practical standard is simple. Use market MOIC ranges as orientation, then adjust for sector, company maturity, capital intensity, and how value will be created. That is how founders avoid overpromising, and how PE partners avoid backing into targets the business was never built to deliver.

Key Levers for Driving MOIC Performance

A target MOIC is only as credible as the operating plan behind it. In boardrooms, I look for one thing first: which lever is expected to do the heavy lifting, and what management will have to change to make that happen. That question sounds simple, but it usually exposes the gap between an attractive model and an executable one.

A practical framework for that comes from treating value creation as an operating agenda, not a spreadsheet exercise. The approach in this piece on private equity investment strategy is useful because it connects return expectations to the decisions a CEO and PE sponsor control.

EBITDA growth starts with execution

EBITDA growth is usually the lever management can influence most directly. It comes from better pricing discipline, tighter procurement, stronger plant utilization, cleaner SKU rationalization, more reliable forecasting, and sharper sales execution. None of that is glamorous. All of it matters.

From the founder side, this is often where frustration begins. A sponsor may underwrite growth as if the commercial engine is already built. The CEO knows the team may still need better data, stronger frontline managers, or a different go-to-market structure before that growth is repeatable. Good deals account for that reality early.

The best operating plans break EBITDA growth into named initiatives with owners, timing, investment needs, and measurable milestones. If margin improvement depends on procurement savings, the team should know which categories, which suppliers, and how long the changes will take. If the growth case depends on cross-sell or pricing, management should be able to explain what has already been tested versus what still sits in the model as an assumption.

When teams need to pressure-test those cases quickly, better tooling helps. For finance leaders and commercial teams building scenarios, reporting packs, and sensitivity analysis, AI solutions for finance and sales teams can save time. The judgment still has to come from people who know the business well.

Multiple expansion is earned through quality

Multiple expansion can improve returns fast, but it is the least controllable lever in most deals. Buyers pay higher multiples for companies that are easier to underwrite, easier to scale, and lower risk to own.

That means management quality, customer concentration, systems maturity, reporting accuracy, margin consistency, and strategic clarity all affect the exit. In industrial and operationally complex businesses, a buyer often cares as much about process reliability and quality of earnings as about headline growth.

Founders sometimes hear "we will sell this business for a better multiple" and treat that as confidence. I treat it as a test. What has to be true for the next buyer to see the asset as better than it is today? If the answer is vague, the model is carrying more optimism than discipline.

The best way to defend an exit multiple is to build a company that a buyer can underwrite quickly and trust.

Here's a useful discussion of these ideas in practice:

Debt paydown improves returns, but it competes with growth

Debt paydown is straightforward in theory. If the company generates cash and lowers its debt, more equity value remains at exit. In practice, the trade-off is harder because every dollar used to pay down debt is a dollar not spent on capex, hiring, acquisitions, or commercial expansion.

Convergence of founder and sponsor perspectives is essential. PE firms want disciplined cash generation. CEOs need enough room to invest in changes that improve the business. Both are right. The hard part is deciding where reinvestment will produce durable EBITDA growth and where balance sheet caution should win.

Strong MOIC performance usually comes from balance across the three levers, not dependence on one. If the case relies mainly on multiple expansion, the plan is fragile. If the return comes from operational improvement, sensible reinvestment, and steady cash generation, both management and the sponsor have a stronger hand from entry to exit.

Negotiating MOIC Targets for Mutual Success

A good MOIC negotiation doesn't feel like a tug of war over a spreadsheet. It feels like both sides are trying to answer the same question: what outcome is ambitious, financeable, and operationally achievable?

Too many founder conversations break down because the target gets treated as a sponsor requirement rather than a shared design constraint. That creates defensiveness fast. The founder worries the bar is artificial. The investor worries management is resisting accountability. Both can be wrong at the same time.

A more grounded perspective comes from understanding how private equity thinks in sector context, especially in complex operating environments such as industrials. That's where private equity industrials insights are useful.

Questions founders should ask early

Founders should not negotiate MOIC in isolation. They should negotiate the assumptions that make it plausible.

Ask questions like these:

- What is carrying the return case. Is the model leaning on EBITDA growth, multiple expansion, deleveraging, or add-on acquisitions?

- What has to be true operationally. Which systems, hires, commercial moves, or plant changes are assumed?

- Where is the margin for error. If pricing softens or integration takes longer, what gives in the model?

- How does management participate. Is the incentive structure tied to outcomes management can influence?

Those questions improve the conversation because they move it away from abstract finance and into controllable decisions.

A founder should never agree to a target without understanding the operating burden hidden inside it.

What PE firms should make explicit

Sponsors also have work to do. If they want alignment, they need to show the path, not just the endpoint.

That means making a few things explicit in plain language:

The value creation plan

Not a dense slide. A clear explanation of what will change in the first year, what comes later, and what management support the fund will provide.The pace of change

Some businesses can absorb rapid transformation. Others need sequencing. Funds that ignore this usually create noise, not value.The definition of success

Is success only one exit scenario, or are there several credible ways to win?The founder's role

Founders need to know whether they are being asked to remain chief architect, transition to strategic operator, or prepare for succession over time.

The best negotiations I've seen don't eliminate tension. They use it productively. Founders push on realism. Investors push on ambition. The target MOIC becomes useful when both sides can say, with a straight face, “Yes, this is hard, and yes, this can be done for reasons we can explain.”

That is the beginning of trust. Without it, every board meeting later becomes a debate over expectations that should have been settled before closing.

Conclusion Your Path to a Successful PE Partnership

A target MOIC looks clean on paper. The hard part starts after signing, when that number turns into hiring plans, pricing decisions, board pressure, debt discipline, and a clock that does not stop.

That is why founders and PE partners should treat MOIC as a working agreement, not just a return target. The multiple matters because it frames what the sponsor needs from the investment. What matters more in practice is whether both sides share the same view of how the business gets there. If the plan depends on margin expansion, the team needs a credible path to pricing, procurement, or operating efficiency. If it depends on growth, everyone should be clear on the cost, pace, and execution risk behind that growth.

I have seen this from both sides. As a founder exiting to private equity, and later as a CEO working with PE funds, the gap is rarely about intelligence. It is about translation. Investors often speak in returns, entry multiples, and exit cases. Founders speak in product cycles, sales capacity, customer retention, and leadership bandwidth. Good deals close that gap early.

That is the practical takeaway.

Before agreeing to a target MOIC in PE deals, founders should ask one question: what will this require from the business over the next few years, in concrete terms? PE partners should ask the matching question: what support, sequencing, and flexibility will management need to deliver that outcome without breaking the organization?

For entrepreneurs preparing for a fundraising process or sale, clear communication still matters. This guide to pitching investors effectively can help sharpen how you present the operating case behind the numbers.

The best partnerships are not built on perfect alignment from day one. They are built on honest assumptions, direct communication, and a value creation plan both sides can defend in diligence and execute in the boardroom. When that happens, MOIC becomes a useful discipline. It stops being shorthand for pressure and starts serving as a shared standard for building a better business.

If you're evaluating a PE transaction, preparing for an exit, or trying to build a value creation plan that stands up in diligence and in execution, connect with Hasit Vibhakar. His experience as a founder, CEO, and investor offers a practical perspective for business owners and executives who want alignment, scale, and durable shareholder value.

Leave a Reply